{kind=link}

Current environment muddies ECB normalization plans

The ECB meeting on Thursday was meant to be quite straightforward but in the current world of populism, trade wars and Brexit, this may be too much to ask.

A few months back when the ECB took the surprising step of not only laying down plans for the end of its quantitative easing program but also offering guidance on the timing of its first rate hike – which could be the only increase of Mario Draghi’s tenure if it comes before October 2019.

After a decade of monetary policy experimentation – which was necessary to save the block initially from the worst financial crisis of our lifetime and then its possible collapse – the ECB was acting like a central bank that had its act together and was headed for a brighter – and easier – future. Unfortunately, the world had other ideas.

Financial markets have been rather temperamental this year – to put it gently – and that has gradually spread as it has progressed from emerging markets, including China, to Europe in the summer and now the US.

The market has been ticking along while underlying threats have been building – many, self-inflicted – be they trade conflicts, rising US interest rates, emerging markets, Brexit and Italy’s budget, to name but a few. While I’m by no means proclaiming we’re heading into a crisis, unstable markets and slowing global growth are a concern and certainly make the job of central banks a little tricky.

What can we expect from the meeting?

I don’t expect the ECB to change course on Thursday and suddenly decide to extend QE, especially not as a means of shielding Italy which has seen the yield on its debt surge over the last six months on the expectations of a budget showdown with Brussels. In fact, I believe this would encourage it to maintain its course and pressure the coalition government into falling in line with euro area rules.

But that doesn’t mean it won’t be aware of the risks which is why investors will be paying extremely close attention to the statements that accompany the decision and the Q&A session that follows with Draghi.

Draghi has a tendency to err on the dovish side and may do so once again tomorrow, given the increasing headwinds. But with Rome set to go head to head with Brussels, following the latter’s unprecedented move to reject the former’s draft budget, perhaps he’ll refrain from such action on this occasion and adopt a more neutral position.

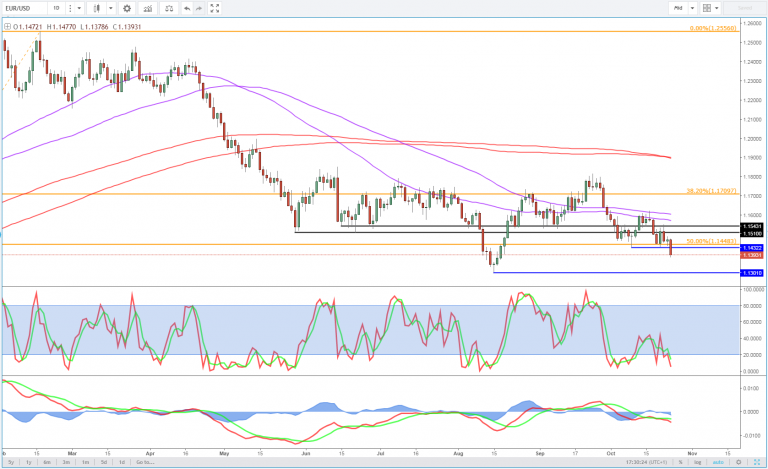

GBPUSD Daily Chart

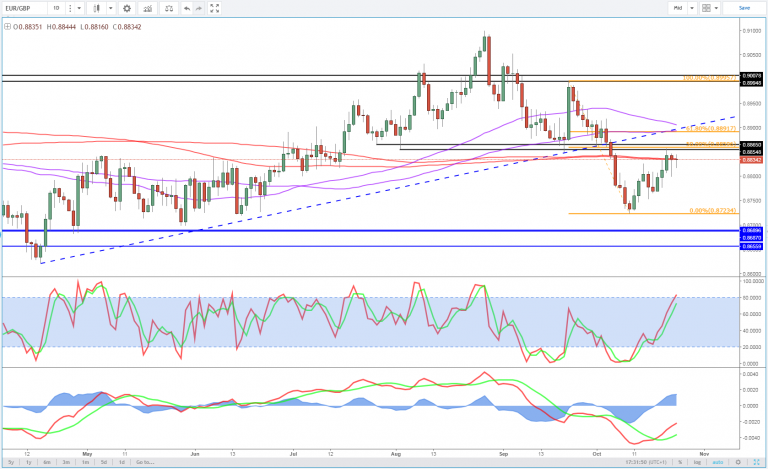

EURGBP Daily Chart

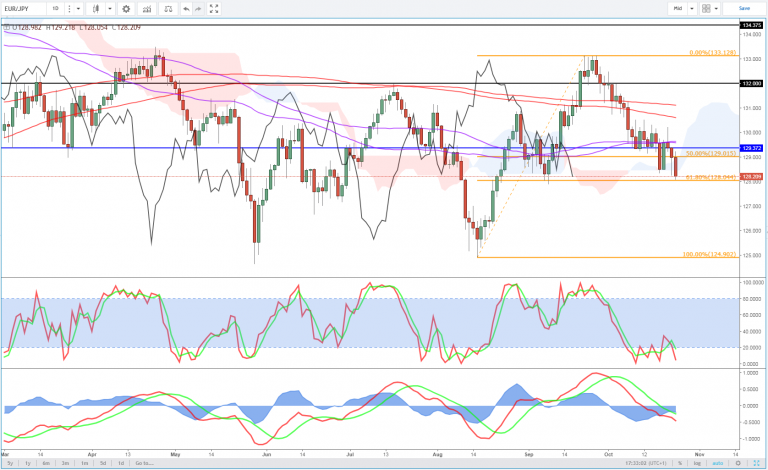

EURJPY Daily Chart