{kind=link}

Here are the latest developments in global markets:

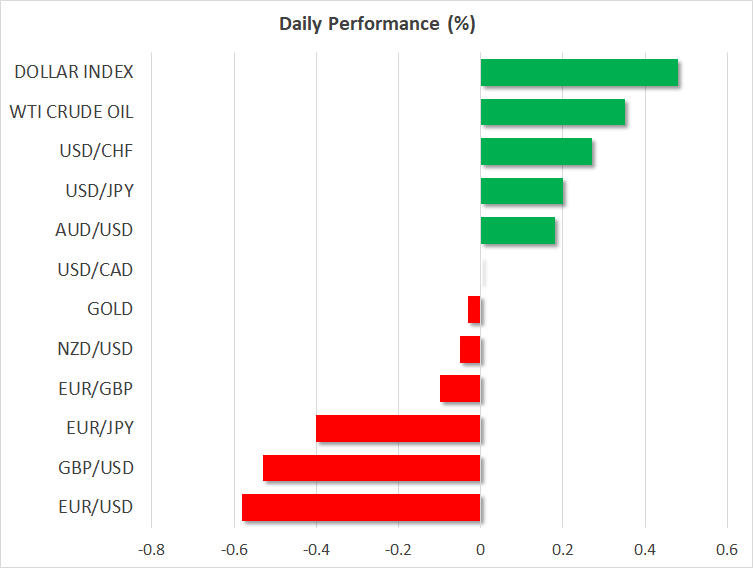

- FOREX: The British pound and the euro were among the worst performing major currencies in early European session on Wednesday, losing around 0.60% against the greenback. Pound/dollar hit a fresh 1 ½-week low at 1.2898 before the UK Prime Minister Theresa May meets with her Conservative Party lawmakers later today (see below). The European Council President, Donald Tusk, said he would call for a November summit, which was previously cancelled by EU leaders, if Brexit negotiators achieve decisive progress toward a deal. Still, the pound was not able to gain on the comments. Disappointing flash Markit PMIs in Germany and in the overall eurozone brought a deep sell-off in the euro, pushing euro/dollar to a two-month low of 1.1394 as investors feared that a weaker business environment could pressure GDP growth even lower before the year ends. Turning to the US, the dollar index jumped by 0.44% to 96.35, to its highest level over the last two months as the euro and the pound tumbled, while dollar/yen advanced by 0.17%. The antipodean currencies were mixed today with aussie/dollar adding 0.10% to its performance and kiwi/dollar falling by 0.08%. Meanwhile, dollar/loonie held steady, rising only by 0.05% ahead of the BOC rate statement later in the day.

- STOCKS: European equities recovered on Wednesday after discouraging third-quarter earnings results particularly in the tech sector shifted funds away from equities on Tuesday. The Italian FTSE MIB, however, remained in the red, falling by 0.24% at 1100 GMT. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were trading higher by 0.57% and 0.85% respectively. The German DAX 30 was up by 0.31%, the French CAC 40 rose by 0.72%, while UK’s FTSE 100 climbed by 0.76%. In the US, stocks were ready to open in negative territory. In corporate news, Deutsche Bank’s third quarter profits declined steeply under the new chief executive Christian Sewing offsetting hopes that the bank could return to profit in 2018, for the first time since 2014.

- COMMODITIES: WTI crude oil edged up to $66.5/barrel (+0.10%) but remained around two-month lows registered yesterday at $65.74/barrel. The London-based Brent, however, decreased by 0.43% to $75.11/barrel, to its lowest level since late August pressured by concerns over weakening demand and rising supply despite US sanctions harming oil exports in Iran and ongoing U.S.-Saudi tensions. In precious metals, gold prices slipped below Tuesday’s new 3-month high of $1,239.68 but remained marginally positive (+0.07%).

Day Ahead: May to face anxious Tories in Parliament; Bank of Canada to raise rates

Following very disappointing initial IHS Markit PMI figures out of the eurozone, the focus will shift to the US Markit manufacturing PMI due at 1345 GMT. Initial estimates support that manufacturing activities in October weakened in the US mainland too but modestly so, driving the index down to 55.5 from 55.6. While a miss in the data could be dollar-negative, investors might prefer to wait the release of the ISM Manufacturing PMI due next Thursday to confirm any slowdown in case the numbers indeed appear lower. ISM PMIs have a longer history than Markit measures have and have proved to be more market-moving as well.

Separately, the US will issue readings on new home sales at 1400 GMT, while at 1800 GMT, the Beige book delivered by the Federal Reserve will be of more importance given that the FOMC uses the report to decide on interest rates. The book presents theeconomic conditions in 12 Federal districts.

In neighboring Canada, the central bank will be meeting at 1400 GMT to decide on interest rates and investors are widely expecting policymakers to raise rates by 25 bps to 1.75%, marking the fifth rate hike since July 2017. With trade risks having mostly faded after Canada, Mexico and the US finally managed to replace the old NAFTA deal with the new USMCA agreement, policymakers could feel more comfortable to unwind further stimulus as inflation stands marginally above the BoC 2.0% price target and the unemployment rate is currently at the lowest in four decades. Yet the BoC might show some caution about the path of interest rates in the future as wages seem to be weakening in the highly indebted country. In September, permanent workers saw their wages slowing for the fourth consecutive month to reach a growth of 2.17%, a warning sign that consumers might turn more careful on their spending if interest rates continue to rise. Should the Bank raise rates but use a cautious tone on future economic trends and overall downplay the prospects of further near-term tightening, the loonie could lose strength. On the other hand, if policymakers appear positive, probably saying that softness in wage growth is temporary, the loonie may find the opportunity to crawl higher. BoC Governor Stephen Poloz and Deputy Governor Carolyn Wilkins will be holding a press conference at 1515 GMT.

In Brexit news, Theresa May will be privately meeting her Conservative Party at the so-called “1922 Committee” event later today in Parliament, where the British Prime Minister will likely face more criticism instead of appreciation over her Brexit strategy. Recent reports stating that May is willing to drop some of her key Brexit demands including a fixed timeframe for the Irish border and the transition period, angered Eurosceptic conservatives even further, with 46 of them having already sent a letter to demand a no-confidence vote against May according to sources. Note that 48 are required to trigger such a vote. If May faces another showdown today, the pound could come under renewed selling. Otherwise, May’s survival could provide some tailwinds to the currency amid hopes that support for the UK Prime Minister and her Brexit plans could be secured before a potential Brexit agreement is presented to Parliament.

Elsewhere, New Zealand will issue new figures on trade balance at 2145 GMT, while in Norway the central bank is expected to keep rates steady at 0.75%.

In oil markets, the Energy Information Administration is scheduled to publish data on US oil inventories for the week ending October 20 after yesterday’s API oil statement identified the strongest built up in crude stocks since March.

In equities, the earnings season continues, with Microsoft being among companies to deliver results for the third quarter after the US market closes.