{kind=link}

Here are the latest developments in global markets:

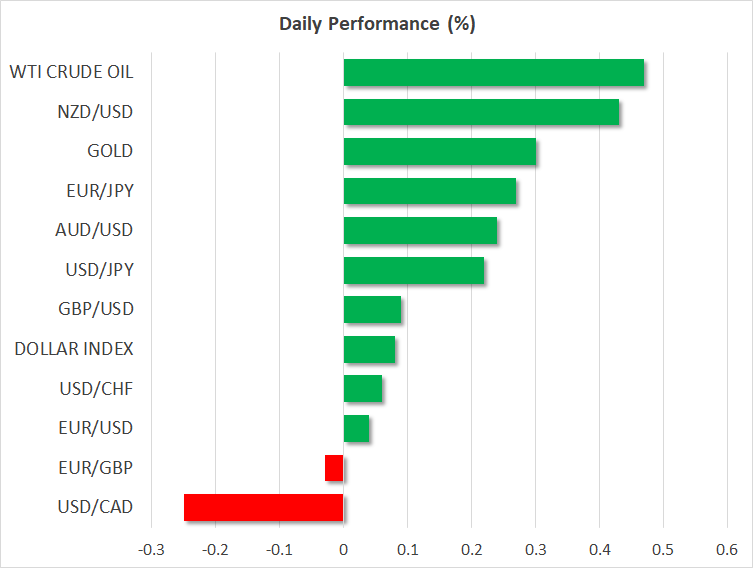

FOREX: The dollar index is a touch higher on Friday (+0.08%), adding to the gains it recorded in the prior session and looking set to end the week meaningfully higher. The pound was the worst performer on Thursday amid a lack of progress on Brexit and downbeat UK data, while the euro also took a hit as Italian budget concerns came back to the forefront. The yen outperformed as risk aversion dominated, but has already surrendered some of those gains today as sentiment appears to have turned around.

STOCKS: Wall Street closed firmly in the red on Thursday, as geopolitical woes and disappointing earnings from industrial firms curbed risk appetite. Lockheed Martin (-1.62%) fell on worries Congress may block arms sales to Saudi Arabia, while Textron (-11.18%) and United Rentals (-14.93%) plunged in the wake of lackluster earnings, citing the impact of tariffs. Accordingly, the S&P 500 (-1.44%) and Dow Jones (-1.27%) tumbled, while the tech sector – where valuations are most stretched – underperformed, with the Nasdaq Composite dropping by 2.06%. Sentiment seems to have reversed though, with futures tracking the Dow, S&P, and Nasdaq 100 pointing to a higher open today. Asia was mixed on Friday, with Japan’s Nikkei 225 (-0.56%) and Topix (-0.69%) declining, but Hong Kong’s Hang Seng (+0.50%) advancing, taking its cue from China’s CSI 300 (+2.97%). Europe was set for a higher open today as well, futures suggest.

COMMODITIES: Oil prices edged lower for a second straight session on Thursday, with both WTI and Brent touching one-month lows, still reeling from a major disappointment in the EIA inventory data earlier in the week. The broader risk aversion in markets likely contributed to the decline. Accordingly, both WTI and Brent rebounded somewhat today, alongside risk sentiment. In precious metals, gold is up by 0.3% on Friday at $1,228 an ounce. The dollar-denominated metal climbed somewhat yesterday too despite another surge in the greenback, as investors turned their sights towards defensive assets.

Major movers: Havens advance as risk appetite sours; Italian worries weigh on euro

Risk aversion was the name of the (trading) game once again on Thursday, with major US stock markets falling considerably, and haven assets – most notably the Japanese yen –advancing across the board. While there was no clear trigger behind this shift, renewed concerns around Italy’s budget, disappointing earnings from industrial firms, still-elevated US bond yields, and the prospect of a fallout in US-Saudi relations may have all contributed. On the Saudi front, US Treasury Secretary Mnuchin withdrew from an investment conference taking place in the Kingdom, amid mounting pressure to hold its leaders accountable for the disappearance of a journalist.

The dollar was the second-best performer among the major currencies, behind the mighty yen, evidently benefiting from the risk-off tones given the absence of tier-one US data. Euro/dollar fell from an intraday high of 1.1525 to settle near 1.1450, not least due to euro weakness as the Italian budget saga came back in focus. The EU Commission sent a letter to Italy outlining its concerns around the budget deficit, and although both sides tried to downplay the significance of the gesture in related comments, Italian bond markets didn’t buy it. Italy’s 10-year bond yield soared above 3.70%, its highest level in 4½ years as investors cut their exposure to Italian assets in anticipation of a potential escalation, thereby sending the euro lower.

The biggest underperformer was the British pound, which suffered at the hands of disappointing UK retail sales data, and the lack of any concrete signs that the Brexit talks are moving forward. Most striking, was the fact that sterling continued to tumble even after EU Commission President Juncker said he is“convinced we will be able to strike a Brexit deal”. The market reaction suggests investors aren’t taking such signals at face value anymore, considering the recent barrage of similarly optimistic, yet void of substance remarks from the various officials. As the adage goes, “talk is cheap”, and actions are seemingly what matters most for markets right now.

Sentiment seems to have turned around on Friday again, as commodity-linked currencies such as the aussie, kiwi, and loonie are all on the front foot, while the safe-haven Japanese yen is surrendering some of the ground it claimed yesterday. Although Chinese GDP data were a touch softer than expected overnight, some extraordinarily optimistic remarks from the nation’s authorities supported sentiment.

Day ahead: Canadian data on inflation and retail sales coming up; politics remain in focus

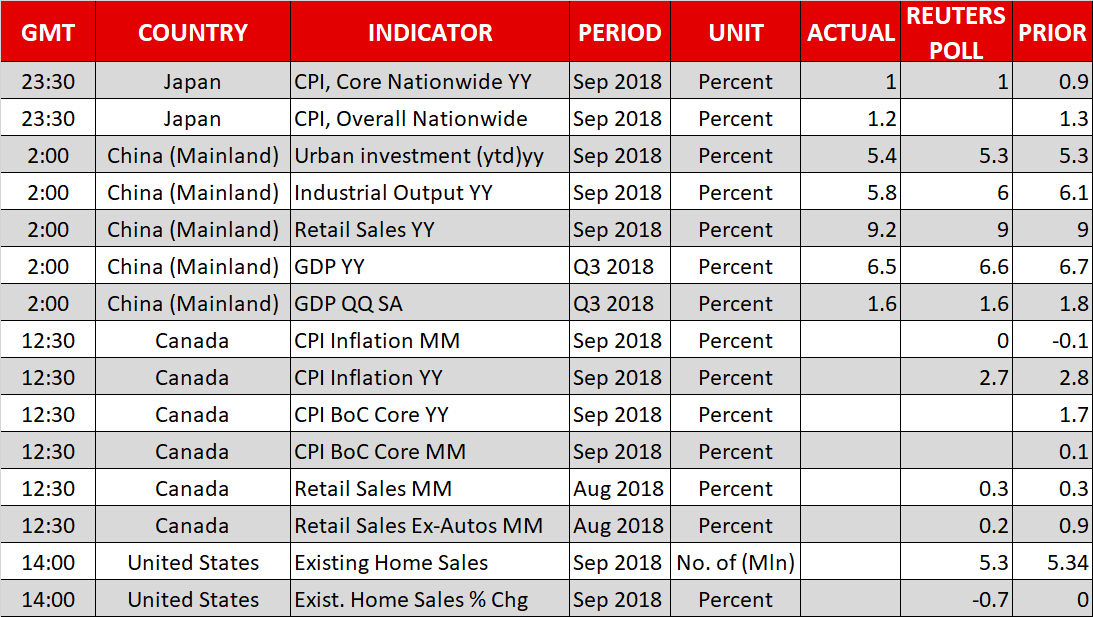

Key Canadian data on inflation and retail sales will be hitting the markets on Friday. Apart from economic releases, political developments will be eyed as they may act as the primary driver of movements during today’s trading.

September’s Canadian inflation as gauged by the consumer price index (CPI) is projected to stand at 2.7% y/y, slightly below August’s 2.8%. This would allow the reading to exceed the Bank of Canada’s (BoC) target for annual inflation of 2.0% for the eighth straight month, and at the same time keep it within the upper bound of the 1-3% target band. Given that higher energy prices largely accounted for the rise in headline CPI, core inflation that excludes energy from its calculations is perhaps attracting additional interest. The same holds true for the measures of core inflation monitored by the Canadian central bank, namely the CPI median, trim and common.

In terms of retail sales out of the nation, they’re anticipated to expand by 0.3% m/m in August, the same pace as in July. Meanwhile, core retail sales that exclude automobiles, are predicted to grow by 0.2% m/m, much lower than July’s 0.9%. Both sets of data (inflation & retail sales) are due at 1230 GMT.

Canadian OIS currently assign a 97% chance for a 25bps rate increase by the BoC when it completes its meeting on monetary policy on October 24; it is practically seen as a done deal. Barring a dramatic weakness in today’s numbers, the figures are unlikely to deter the central bank from proceeding with a rate increase next week.

Out of the US, existing home sales for September are due at 1400 GMT. Generally, these are not market moving for FX markets, though they have their own interest, especially in light of the rising rate environment which is typically negative for the real estate market.

Beyond releases, concerns over an EU-Italy clash over the latter’s budget plans remain firmly on the table, weighing on the common currency. Elsewhere, any Brexit headlines will be closely watched as well. This week’s summit failed to bring the two parties closer to a deal, thus acting as a drag on the pound. In light of the impasse, EU leaders called off the November Brexit summit, with a gathering aiming to complete the deal now expected to take place in December.

Policymakers making public appearances include Bank of England Governor Carney who will be giving a speech at 1530 GMT. Kaplan, a non-voting FOMC member in 2018, is on the agenda at 1445 GMT.

In equities, Procter & Gamble and Honeywell are among companies releasing quarterly results on Friday; both will be reporting before the opening bell on Wall Street.

In energy markets, Baker Hughes data on active oil rigs in the US are scheduled for release at 1700 GMT.

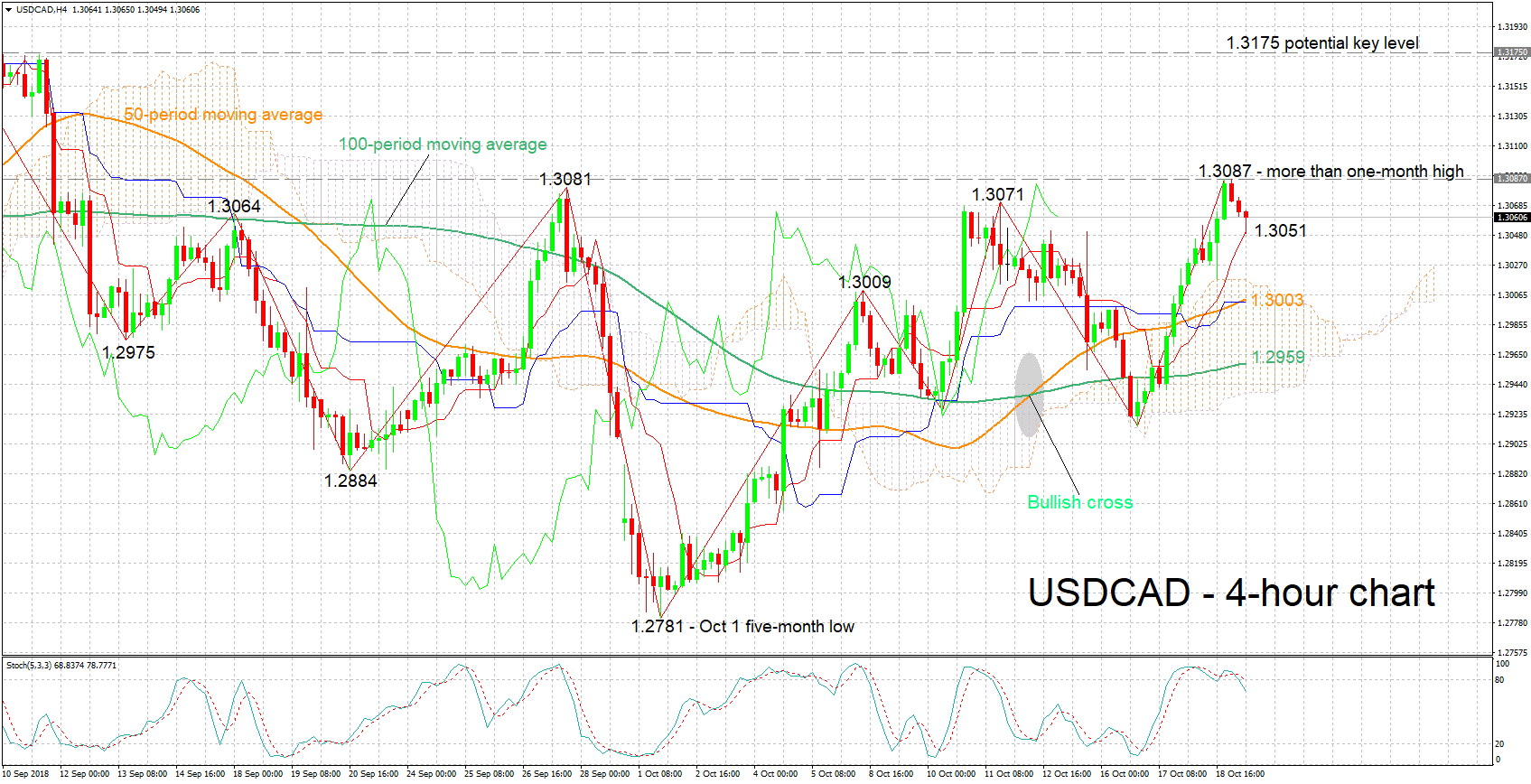

Technical Analysis: USDCAD loses steam after hitting more than one-month high; bearish signal by stochastics in very short-term

USDCAD retreated a bit though it still remains close to Thursday’s more than one-month high of 1.3087. The Tenkan-sen is above the Kijun-sen in support of a bullish short-term bias. Notice though that the latter has flatlined, suggesting that positive momentum may be easing. Moreover, the stochastics are giving a bearish signal in the very short-term: the %K and %D lines have recorded a bearish cross and are both heading lower.

Upbeat Canadian data are expected to boost the loonie, pushing the pair lower. Immediate support seems to be taking place around the Tenkan-sen at 1.3051. A move below would eye the zone around the current level of the 50-period moving average line at 1.3003, which also encapsulates the Ichimoku cloud top (1.3017) and the Kijun-sen (1.3001). Not far below lies the 100-period MA at 1.2959.

Conversely, a miss in the numbers is likely to push USDCAD higher. A barrier to gains could come around yesterday’s high of 1.3087; the region around this captures numerous other tops from the recent past as well as the 1.31 round figure. Higher still, additional resistance may occur around 1.3175, a congested area in early September.

Canada is a major oil exporter and the direction in the previous liquid can also affect the currency’s movement.