{kind=link}

Here are the latest developments in global markets:

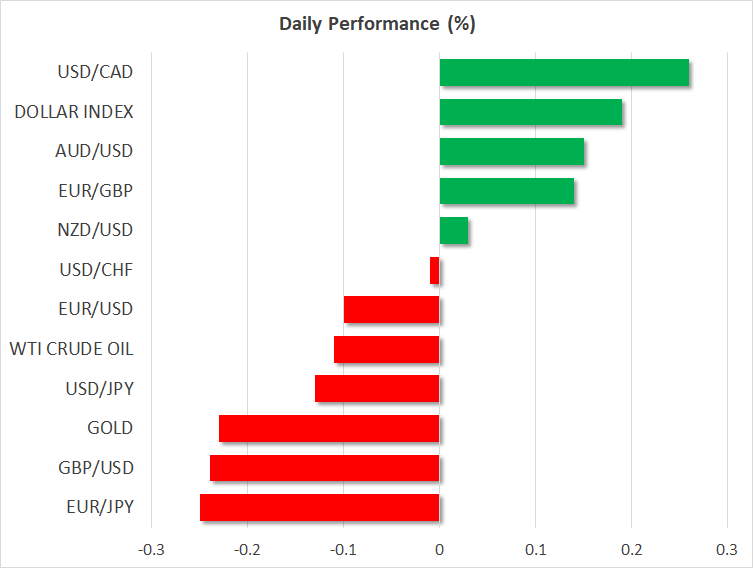

FOREX: The dollar index is up by nearly 0.20% on Thursday, building on the spectacular gains it recorded yesterday, aided by a hawkish tone in the latest Fed minutes. Meanwhile, the worst performers on Wednesday were the euro and loonie, amid Italian budget concerns and a sharp drop in oil prices respectively. The pound traded choppy and lower overall, weighed on by soft UK inflation data and the absence of real progress in the EU summit.

STOCKS: US markets closed lower, albeit only modestly, with a relatively hawkish tone in the FOMC minutes and signals that the US-China trade conflict may escalate further weighing on appetite for risk. The Dow Jones (-0.36%) tumbled the most, dragged lower mainly by Home Depot (-4.34%). Both the S&P 500 and the Nasdaq Composite inched lower by roughly 0.03%. However, sentiment seems to have turned even more sour, as futures tracking the Dow, S&P, and Nasdaq 100 are pointing to a much lower open today. Indeed, the negative mood was also evident in Asia, which was a sea of red. Japan’s Nikkei 225 (-0.80%) and Topix (-0.54%) dropped, alongside the Hang Seng in Hong Kong (-0.54%). Europe was set for a mixed open today, futures suggest.

COMMODITIES: Oil prices plunged on Wednesday, with WTI dropping by more than $2, weighed on by a surprisingly large build in the weekly EIA inventory data. It likely came as a major upset, as the private API figures one day earlier pointed to a drawdown. Poor risk appetite in markets and a stronger dollar may have also contributed to the drop. WTI is also lower today by 0.11% at $69.63 per barrel, while Brent is down by 0.42% at $79.71/barrel. In precious metals, gold is lower by 0.23% on Wednesday at $1221 per ounce. The dollar-denominated metal declined yesterday as well, but only marginally, and certainly much less than one would expect given the surge in the dollar. This resilience reaffirms that demand is slowly picking up, and that gold may have carved out a bottom.

Major movers: Dollar extends gains after “hawkish” FOMC minutes

The greenback was by far the best performer in Wednesday’s session even ahead of the release of the FOMC minutes, extending its gains in the aftermath. The minutes revealed a hawkish tilt, with the Committee appearing increasingly confident that interest rates will eventually need to be pushed above the level which they consider “neutral”. This was hardly surprisingly, considering their latest rate-path projections anticipated rates to move above the longer-run neutral rate 3.0% by the end of 2019. Still, investors took the opportunity to push US bond yields and the dollar a little higher, which likely illustrates that some expected a more cautious commentary.

Overall, officials appeared more optimistic on inflation, and little concerned by trade risks. The key takeaway was the Fed remains committed to raising rates in a gradual manner – perhaps once a quarter – until the “neutral” level of roughly 3.0% is reached, after which a couple of more rate increases may be appropriate, albeit in a slower manner. Yet, market participants don’t appear that confident, having fully priced in only two quarter-point hikes between now and June 2019, which suggests they expect a pause of one quarter in the meantime.

On the Brexit front, the working dinner between EU leaders yesterday yielded little of real substance, though the broader tone was quite upbeat, leaving the impression that both sides are committed to reaching a deal. The pound traded lower for the most part, weighed on by disappointing UK inflation data. Elsewhere, the worst performers on Wednesday were the euro and loonie. The Canadian currency tracked oil prices lower, while the euro remained soft amid reports that the EU will – to the suprise of nobody – reject Italy’s draft budget proposal.

In the broader market, risk appetite remained on shaky legs. Major US equity indices struggled after the Fed minutes amid an uptick in bond yields. Some aggressive moves by President Trump against China didn’t help. The White House announced the US will withdraw from the Universal Postal Union, a 144-year treaty which allegedly enables China to ship goods at unfairly low prices, putting American businesses at a disadvantage. Separately, the US Treasury refrained from labeling China as a currency manipulator in its biannual report, but made it clear it’s watching the yuan closely.

Day Ahead: UK retail sales & Philly Fed Business index awaited; EU summit eyed

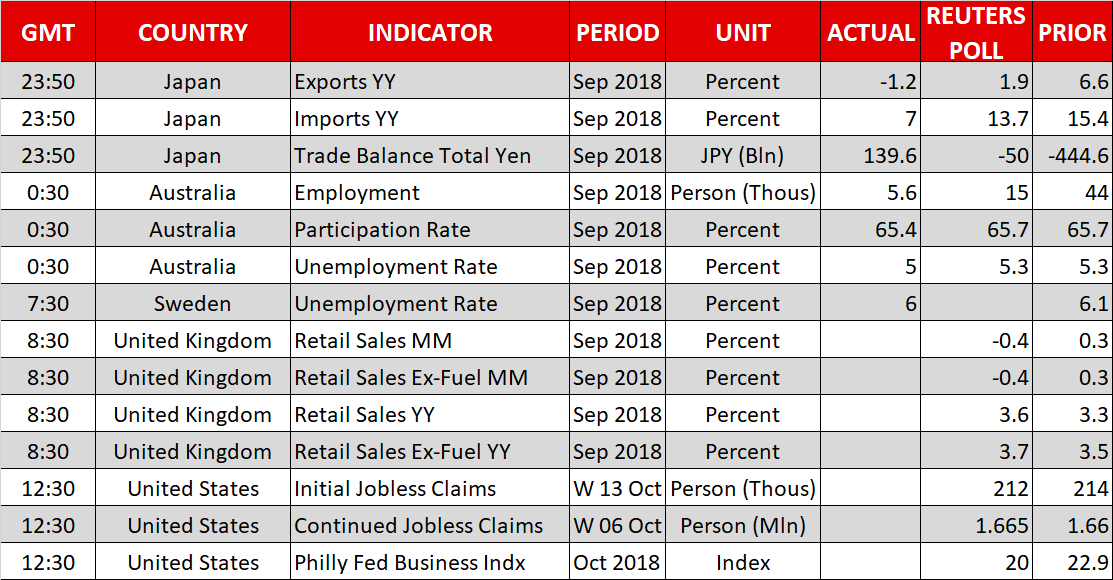

While EU leaders are struggling to find a common ground on the Brexit front in Brussels, with the EU negotiator, Michel Barnier supporting that more time is needed for progress and the UK Prime Minister showing willingness to expand the transition period, investors will turn attention to the calendar during the early European session. At 0830 GMT, retail sales out of the UK are expected to decline by 0.4% on a monthly basis in September after inching up by 0.3% in August, though the annual growth is projected to come higher by 0.3 percentage points at 3.6%. Washing out volatile components such as automobiles and fuels the monthly core measure is said to fall by 0.4% as well, while the yearly gauge is projected to rise by 3.7% compared to 3.5% before. Should the data beat forecasts, indicating that British consumers feel more comfortable to shop as wage growth picks up steam and inflation slides towards Bank of England’s 2.0% price target, the pound could rebound.

In the US, Federal Reserve of Philadelphia will update its Business index for the month of October at 1230 GMT, where any upside surprise could boost investors optimism about the health of the US economy and thus raise stakes for additional rate hikes in coming years. In the aftermath, better than expected readings could spark a stronger rally for the greenback. Looking at forecasts, analysts anticipate the index to ease from 22.9 to 20.

At the same time initial jobless claims for the week ending October 13 will come public as well.

Meanwhile in the Eurozone, besides Brexit, Italy’s spending plans is another worrying issue for traders as recent comments from EU officials including the President of the European Commission, Jean-Claude Junker were discouraging hopes for a lull in the EU-Italian tensions.

As of public speeches scheduled for today, ECB Governing Council member Ewald Nowotny will be talking on “the future of financing and currencies” at 0800 GMT, while ECB Executive Board Member Benoit Coeure and ECB President Mario Draghi are due to speak in the Euro Summit which concludes today in Brussels. In the US Federal Reserve Bank of St. Louis President James Bullard will be giving a presentation on the U.S. economy and monetary policy before the Economic Club of Memphis. In Nw York Fed Vice Chairman for Supervision Randal Quarles will be commenting before an Economic Club of New York luncheon.

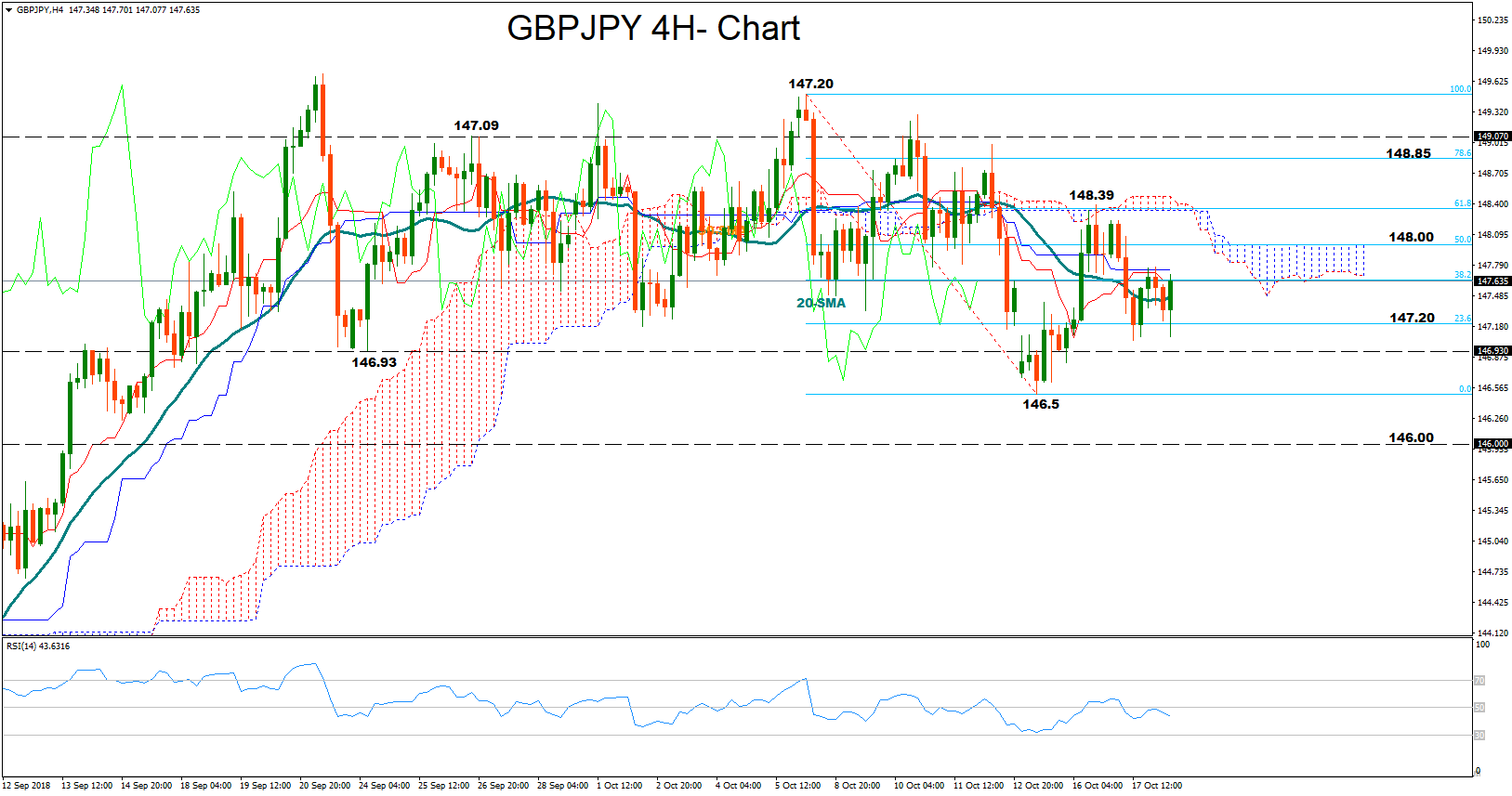

Technical Analysis – GBPJPY in neutral mode; risk tilted to the downside

GBPJPY returned to neutrality after the rebound on the one-month low of 146.5 on October 15, though downside risks remain in the short-term as the RSI heads south below its 50 neutral mark.

Should the market weakens in the wake of disappointing UK retail sales or discouraging Brexit news, the price could slip towards 147.20, the 23.6% Fibonacci of the downleg from 149.50 to 146.5 which has been a main support since the start of the month. Moving lower, bearish actions could retest September 24’s low of 146.93 before hitting the 146.5 bottom. Stepper declines below the latter, could bring the 146 round level into view.

Alternatively a beat in data, would probably drive the price up to 148, where the 50% Fibonacci stands, while if this level fails to hault upside movements, the next stop could be around the previous peak of 148.39 which is slightly above the 50% Fibonacci. Even higher, resistance is expected to come between the 78.6% Fibonacci of 148.85 and September 26’s high of 149.07.