{kind=link}

With optimism around a Brexit deal being wrapped up this week receding, markets could turn their attention back to economic data on Tuesday at 0830 GMT, when the UK will release its latest employment figures. After that, sterling’s fortunes will likely be tied to how the crucial EU summit commencing on Wednesday plays out, and whether investors are left with the impression that a deal may be finalized in November, or not.

Hopes that a Brexit deal would be reached as early as this week came crashing down on Sunday, following news that the negotiations have been “paused” until the EU summit kicks off on Wednesday, amid a lack of progress on the Irish border issue. While it’s not entirely out of the question that an agreement is found at the last minute, developments generally point to the direction of the talks being extended for a few weeks, with a special EU summit to be called in November if enough headway has been made until then.

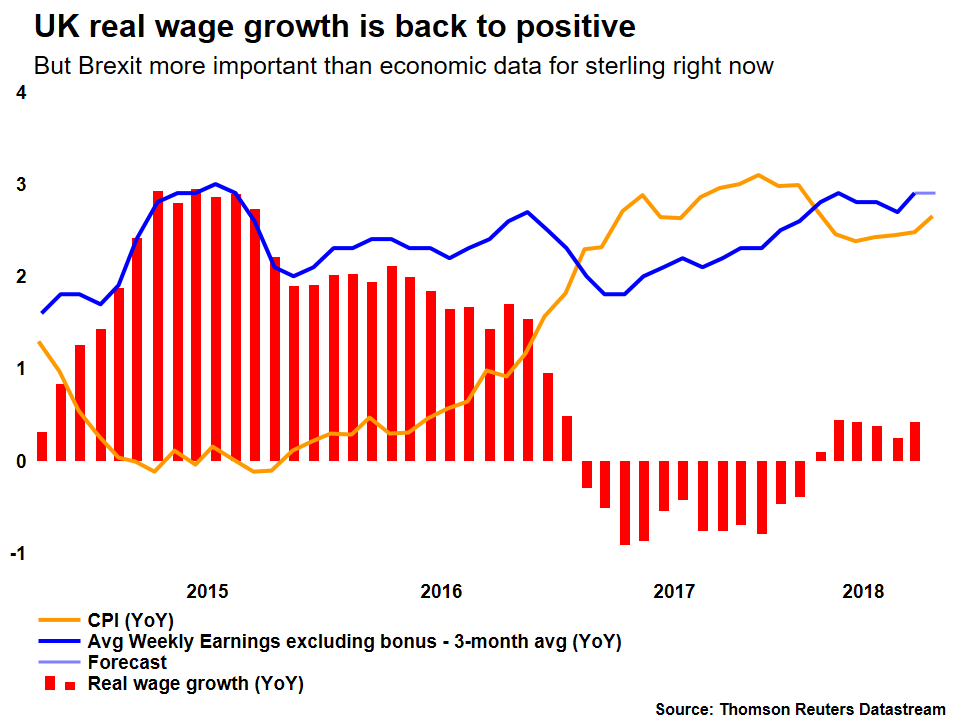

Ahead of this week’s summit, investors could briefly turn their gaze back to economics on Tuesday, when the UK releases its jobs data for the three months to August. Forecasts point to an employment report that would reaffirm the labor market’s strength, with the unemployment rate expected to have held steady at 4.0% – a low last seen in 1975. Meanwhile, average weekly earnings both including and excluding bonus pay are projected to have grown at the same pace as previously, at 2.6% and 2.9% respectively in yearly terms. As for where risks may lie, the UK services PMI for August was very upbeat, noting that employment growth accelerated to its fastest in six months.

While a strong set of data could provide some support to the pound, political developments may eclipse economic ones in driving the currency overall over the coming weeks, considering the critical juncture the Brexit process is currently at. Separately, the fact that the next BoE rate hike is priced in only for August 2019 suggests investors expect policymakers to remain sidelined until the political fog lifts, and that economic data alone may have less of an impact than usual on policy decisions.

With respect to the upcoming EU summit, while nothing concrete (like a deal) may come out of it, markets will still watch the tone of any relevant remarks from EU officials closely as they try to gauge whether reaching an accord in November is a realistic prospect, or not. Indeed, the pound has been sensitive to optimistic rhetoric in recent weeks, gaining ground on comments suggesting a deal is possible, even when they lacked real substance.

Although it’s a close call, the most likely outcome still appears that of a deal being ultimately reached, given the strong desire on both sides for one. Even if that is the case, however, it’s not going to be a smooth trip higher for sterling. The amount of work that remains to be done on the Irish border implies the pound will likely stay volatile, and hostage to incoming headlines for a while. That said, once an accord does appear to be imminent, then the rally in the currency may be quite explosive. The heavy net-short speculative positioning on the pound (CFTC data) allows room for a sudden and violent surge in case numerous investors simultaneously rush to cover or unwind their bearish bets.

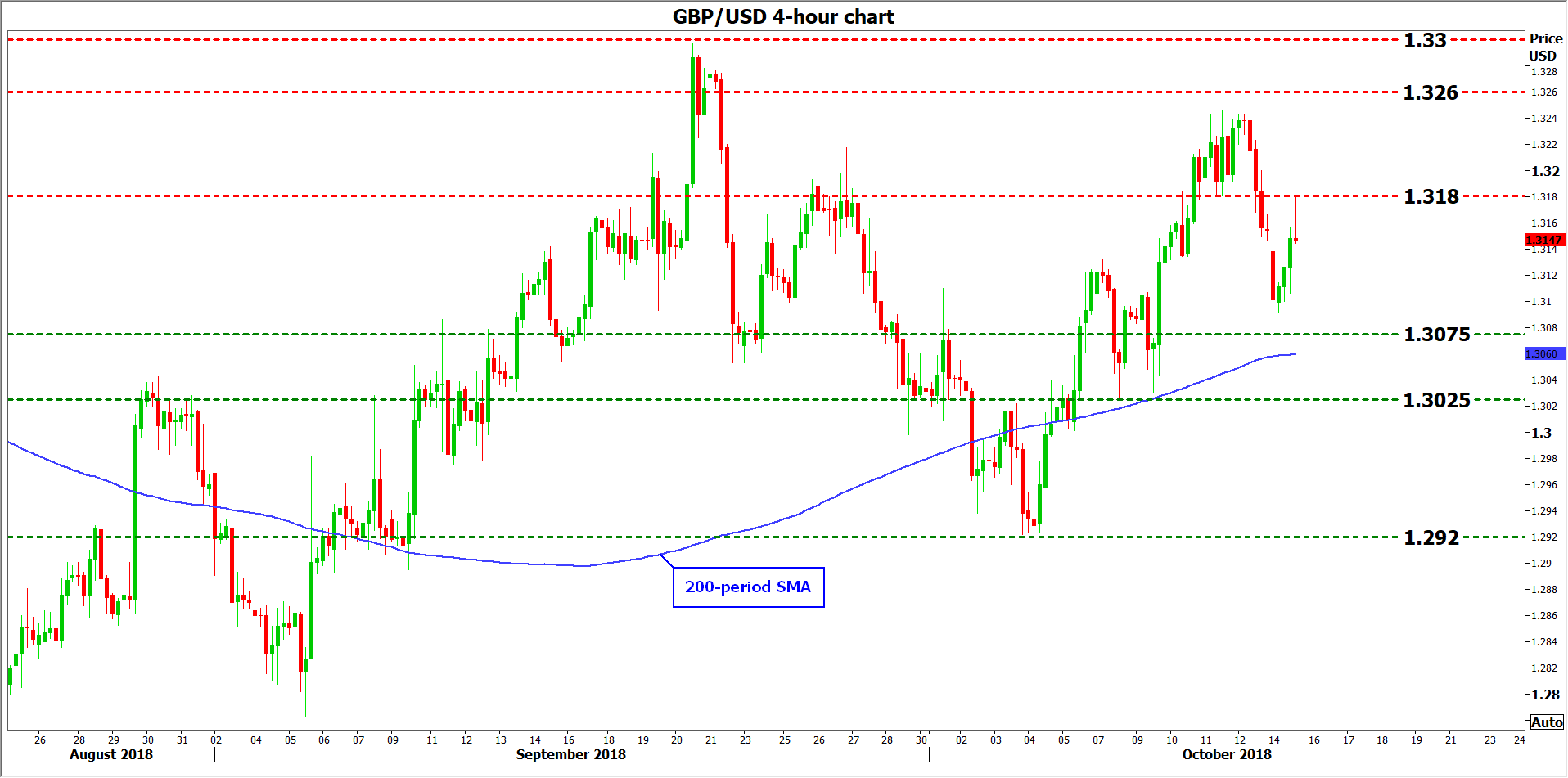

Technically, advances in sterling/dollar may meet initial resistance around 1.3180, an area marked by the inside swing low on October 11. An upside break could open the way for a test of the October 12 high of 1.3260, before the 1.3300 zone comes into view – this being the September 20 peak.

On the flipside, declines in the pair could stall around the 1.3075 territory, defined by the October 15 low. If the bears pierce below it, then the October 8 trough of 1.3025 could provide some support, with even steeper downside extensions seeing scope for a test of the 1.2920 area – the October 4 low.