{kind=link}

Here are the latest developments in global markets:

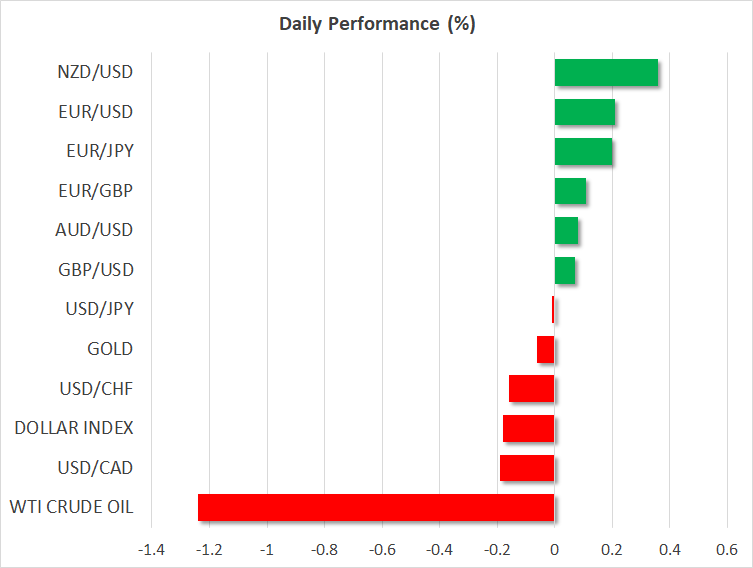

FOREX: The dollar index was down by almost 0.2% against a basket of six major currencies on Thursday, extending losses from the previous session. The yen was the best performer, advancing against all its major peers as risk aversion took hold, amid sustained worries around the trade outlook and elevated bond yields. Meanwhile, commodity currencies were hammered lower in this environment, with the loonie being caught in the eye of the storm as oil prices tumbled as well.

STOCKS: US markets fell off the cliff on Wednesday, with the benchmark S&P 500 (-3.29%) posting its biggest daily drop since February, and the Dow Jones (-3.15%) falling more than 800 points. Weakness was most evident in the technology sector though, where valuations were the most stretched. The tech-heavy Nasdaq Composite (-4.08%) underperformed amid declines in names like Google-parent Alphabet (-4.63%), Netflix (-8.38%), and Amazon (-6.15%). Futures tracking the Dow, S&P, and Nasdaq 100 are all flashing red, pointing to a negative open today as well. Asia was also a sea of red on Thursday, with Japan’s Nikkei 225 (-3.89%) and Topix (-3.52%) plunging amid a stronger yen, while the Hang Seng in Hong Kong dropped by 3.88%. Likewise, European indices are all set to open significantly lower today, futures suggest.

COMMODITIES: Oil fell on Wednesday alongside energy stocks and the broader market, as risk aversion sapped demand for the precious liquid. WTI fell more than $2 yesterday, and both WTI and Brent are trading lower today as well, at $72.63 and $82.41 per barrel respectively. That said, concerns on the supply side likely limited any greater losses, as Hurricane Michael hit Florida, severely disrupting oil production in the US Gulf of Mexico. In precious metals, gold is down marginally on Thursday (-0.08%) at $1,196 per ounce, continuing to trade sideways and remaining uncharacteristically immune to the broader turbulence in financial markets.

Major movers: Stock selloff turns into bloodbath as risk-off tones dominate

US stock markets came under severe selling pressure on Wednesday, with the benchmark S&P 500 plunging by 3.29%, wiping out several months’ worth of gains in a single session. There was no clear fundamental catalyst to trigger the selloff. It was instead attributed to the ‘usual suspects’, namely the elevated US bond yields and growing concerns around the impact of a trade war between the world’s two largest superpowers.

In the FX market, currencies moved largely as one would expect amid the risk-averse environment. The Japanese yen, which tends to benefit at times of uncertainty, advanced across the board as investors turned towards defensive assets. Meanwhile, commodity currencies such as the loonie and aussie, both of which are typically correlated with risk sentiment, plunged – with the loonie’s suffering being amplified by a drop in oil prices. As for the dollar, it generally lost some ground as US bond yields pulled back, though the decline was far from dramatic.

President Trump was on the wires following the market selloff, blaming the turbulence entirely on the Fed raising rates too much, saying ‘I think the Fed has gone crazy’. He added he ‘really disagrees’ with hiking rates further, and that they are ‘so tight’ already. While the Fed and most notably Chair Powell have clearly shown they won’t be swayed by such remarks, it is most interesting that the White House pays this much attention to daily moves in markets. It leads one to question whether a sustained selloff would elicit a policy response directly from Trump aimed at propping up markets, or at least supporting sentiment. In other words, does the US administration measure its success by stock market performance, and if so, is a ‘Trump put’ on the cards if the picture truly deteriorates?

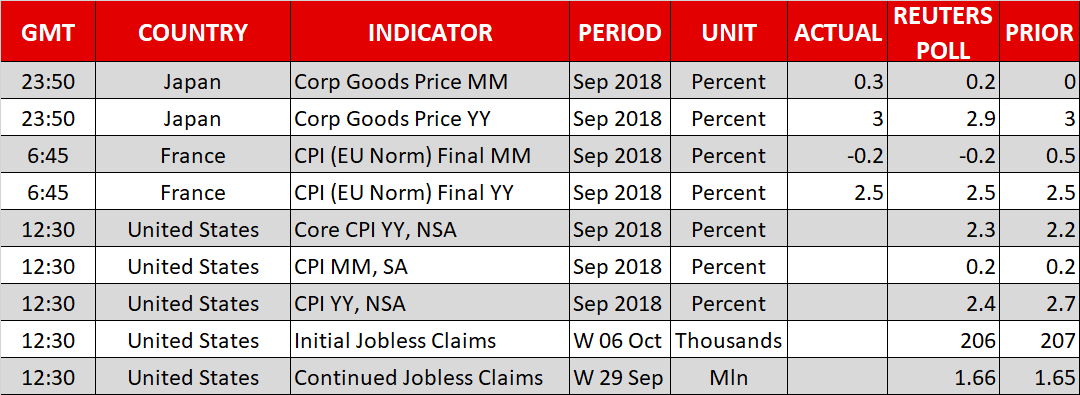

Turning back to the FX market, today’s moves could largely hinge on the US inflation data. A potential acceleration in inflation could drive US bond yields even higher, enhancing risk aversion and weighing on stocks. Hence, the risks surrounding dollar/yen specifically, may be tilted to the downside today. A weak CPI print would push the pair lower on dollar-weakness, and although a strong figure would drive it higher, that strength may well fade once stocks sell off and the yen starts attracting demand.

Day ahead: US inflation data in the spotlight; ECB minutes also out

The highlight out of Thursday’s calendar will be US inflation data as gauged by the consumer price index (CPI) due at 1230 GMT, while ECB minutes pertaining to its September meeting will also be made public today. Other themes remaining in the background are Brexit, Italian politics, as well as trade and yield angst that acted as a major drag on US equities during Wednesday’s session.

US headline CPI for September is anticipated to grow by 0.2% on a monthly basis, the same as in August, which would put the annual rate of growth in the measure at 2.4%, matching its lowest since March. Still, this would keep the print at relatively elevated levels. Overall and adding to this the projected rise in core CPI to 2.3% y/y from 2.2%, the annual slowdown in headline CPI is unlikely to be seen as threatening the Federal Reserve’s rate outlook. Core inflation is the reading that excludes volatile food and energy items from its calculations.

Despite the Fed’s preferred indicator of price pressures being the core PCE price index, still consumer price inflation is also closely watched. A beat in the figures is likely to be met with rising odds for a fourth 25bps rate rise in 2018 (73% priced in according to Fed fund futures), which is dollar-supportive in theory. In light of yesterday’s stock rout, it bears mention that stronger-than-projected CPI readings resulting in elevated Treasury yields may trigger another selloff in equities, which could divert funds into the safe-haven yen, thus proving greenback-negative in this particular pair. Lastly, US weekly jobless claims data are also out at 1230 GMT.

On Brexit, the EU’s chief negotiator Barnier saying 80-85% of the withdrawal deal was agreed was sterling-positive. More evidence that the UK and the EU are getting closer to sealing an actual deal is expected to be met with additional long sterling positions by market participants.

Despite the euro recovering somewhat from its lowest in around two months of 1.1429 hit on Tuesday, worries over Italy and a possible clash with EU officials over its spending plans may soon haunt the currency again. Possibly providing some short-term direction to the currency today will be ECB minutes pertaining to the Bank’s latest meeting due at 1130 GMT. ECB chief Draghi recently describing the pick-up in underlying inflation as ‘relatively vigorous’ led to a jump in the common currency. Any signs of policymakers overall becoming more confident about the euro area’s inflation outlook are expected to support the euro.

Bank of England policymaker Vlieghe will be talking on ‘Global and domestic challenges for UK monetary policy’ at 1045 GMT. Elsewhere, ECB President Draghi and Board Member Coeure will be among those attending the IMF and World Bank’s annual meetings.

In equities, Delta Airlines will be among companies releasing quarterly earnings today; the corporation will be reporting its results before the opening bell on Wall Street. Beyond earnings, fears over worsening Sino-US trade relationships and rising yields are still in place, though yesterday’s selloff may also provide a ‘buy-the-dip’ opportunity.

In energy markets, EIA data on US crude stocks are due at 1500 GMT. An inventory buildup of around 2.6 million barrels is forecast for the week ending October 5, following a rise by around 8.0m during the previously tracked week.

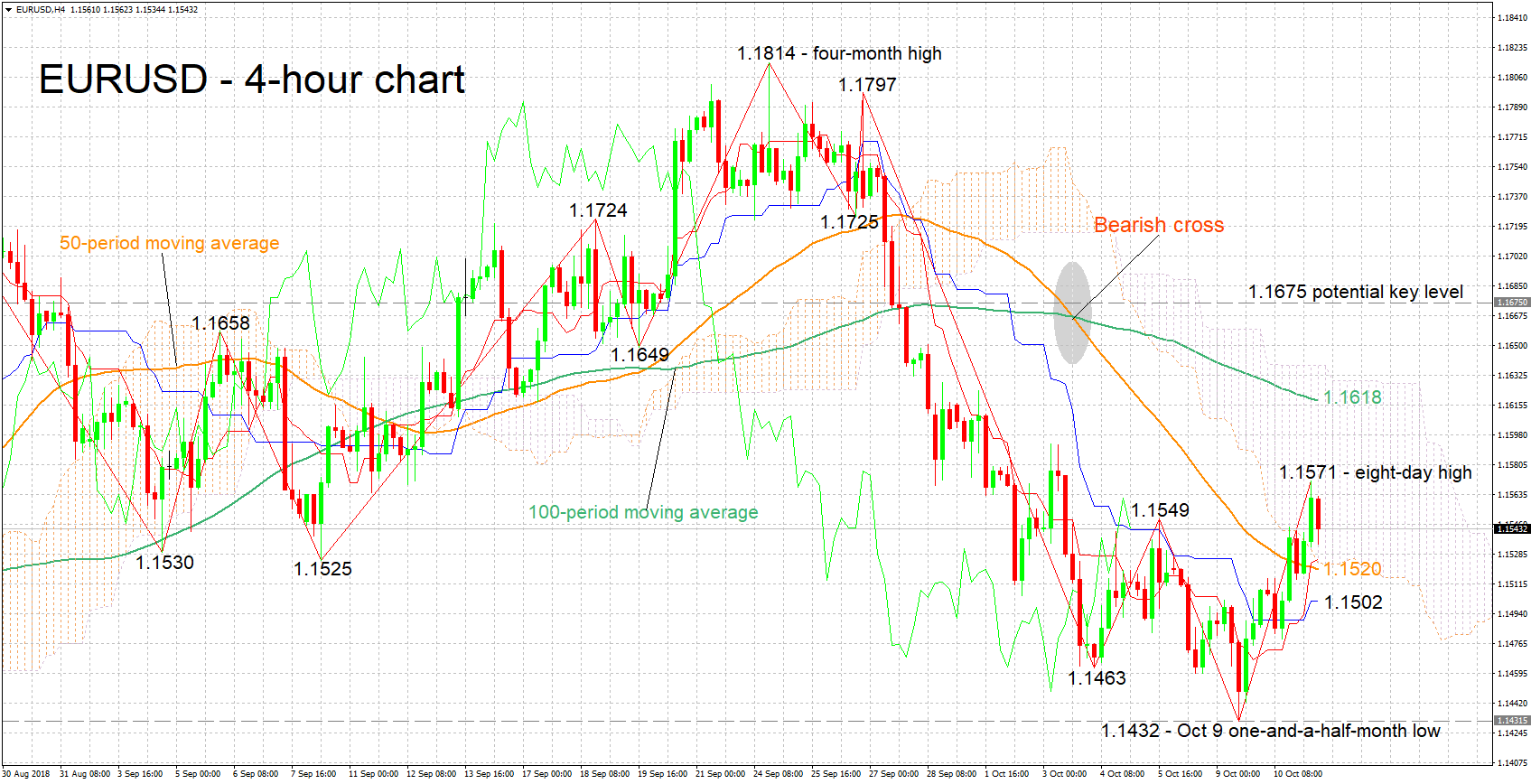

Technical Analysis: EURUSD hit 8-day high in sign momentum turned positive

EURUSD touched an eight-day high of 1.1571 earlier on Thursday, extending its recovery from Tuesday’s one-and-a-half-month low of 1.1432. The Tenkan-sen climbed above the Kijun-sen, suggesting that the bias in the short-term has turned positive.

A relatively hawkish ECB as evidenced by today’s meeting minutes or disappointing US CPI numbers are likely to boost the pair. Immediate resistance may occur around the earlier hit high of 1.1571. The area around the current level of the 100-period moving average at 1.1618 that also includes the Ichimoku cloud top at 1.1639 would be eyed in case of stronger bullish movement. Higher, the previously congested region around 1.1675 would come into focus.

On the downside and in case of a dovish ECB or stronger-than-projected inflation numbers out of the US, support may come around the 50-period MA at 1.1520; the Tenkan-sen and Ichimoku cloud bottom roughly coincide with this point, while the Kijun-sen lies not far below at 1.1502. Lower still, October 9’s one-and-a-half-month low of 1.1432 would increasingly come into scope.

Developments in Italy can also move the pair.