{kind=link}

Here are the latest developments in global markets:

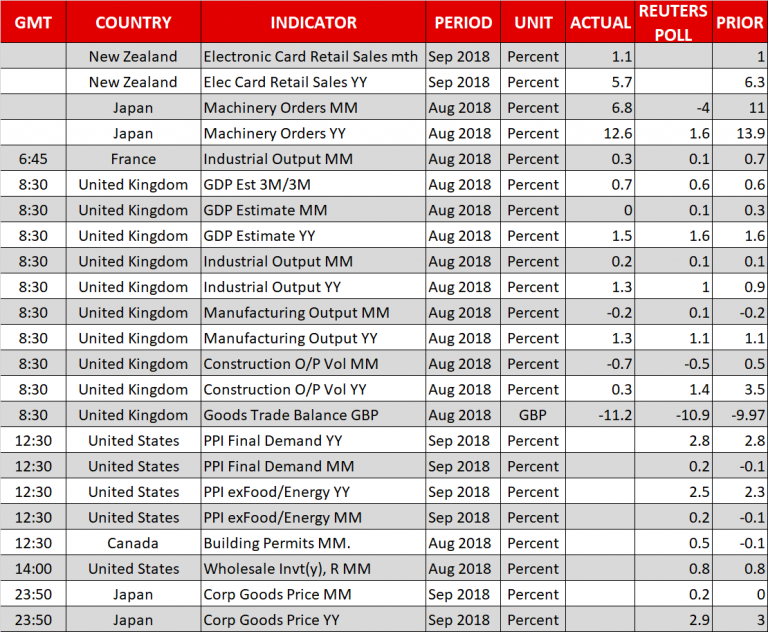

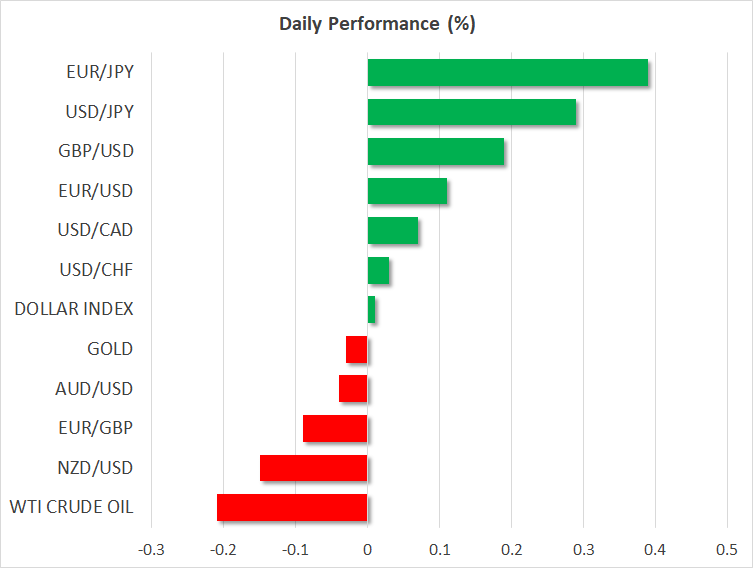

- FOREX: The British pound unlocked fresh two-week highs against the US dollar at 1.3184 but it soon fell to 1.3136 after GDP growth readings out of the UK missed a forecast of 1.6% y/y, showing instead an expansion of 1.5%. July’s mark, though, was revised upwards, from 1.6% to 1.7%. Separately, manufacturing and construction outputs in August disappointed as well, driving industrial production back to the negative territory. The British trade balance in the same month was unexpectedly discouraging too, displaying a wider deficit than projected. News that the EU and the UK are making progress on the UK-Irish border, a sticking point in Brexit negotiations, refreshed hopes that a deal could be near, helping pound/dollar to recover to 1.3156 (+0.10%). Euro/dollar was moving sideways around 1.1500 as the EU-Italian budget conflict maintained some caution in the market. Meanwhile, Reuters stated that the German government is considering cutting growth forecasts for 2019 from 2.3% to 1.8%. In monetary-related news, ECB member Yves Merch expressed confidence that wage growth should help core inflation to pick up steam ahead of ECB meeting minutes due on Thursday. Euro/pound was a little lower at 0.8736 despite the US President criticizing the Fed’s rate hike plans and trade uncertainties still hanging in the background. As of note, US 10-year Treasury yields were recovering after Tuesday’s pullback from 7-year highs. Dollar/loonie was marginally up at 1.2958 (+0.11%). In antipodean currencies, aussie/dollar and kiwi/dollar reversed earlier gains to slide to 0.7097 (-0.06%) and 0.6460 (-0.19%).

- STOCKS: The majority of European shares reversed lower on Wednesday after posting soft gains on Tuesday, as investors traded cautiously on fears that US tariffs may have serious consequences on global trade and world economic welfare. The pan-European STOXX 600 retreated by 0.21%, whereas the blue-chip Euro STOXX 50 was up by an equivalent percentage led by gains in telecommunications and utilities. The German DAX 30 declined by 0.46%, UK’s FTSE 100 was steady, while Italy’s FTSE MIB improved by 0.14%. The French CAC 40 dropped by 0.55% as shares in fashion companies such as the Gucci-owner Kering and the Paris-based Louis Vuitton tumbled amid concerns the US-Sino trade war could push away luxury-buyers in China. In Asia, equities closed mixed. In the US, futures tracking the S&P 500, Nasdaq 100 and Dow Jones held moderate losses, pointing to a soft negative open.

- COMMODITIES: WTI crude oil and Brent were weaker by 0.10% at $74.91/barrel and $84.93/barrel correspondingly after the IMF downgraded its global growth forecasts for 2018 and 2019 on Tuesday, mirroring a slowdown in demand for energy. Yet, platform evacuations and shut-ins in the Gulf of Mexico on the face of Hurricane Michael which was moving towards Florida, limited steeper declines in the market. In precious metals, gold went down to $1186.5/ounce (-0.21%).

Day Ahead: US delivers PPI ahead of CPI figures tomorrow; Canadian building permits on today’s calendar

President Donald Trump noted overnight that he is not happy with the Fed’s policy, saying that rates don’t have to rise this fast as inflation is under control. The disagreement between Trump and the Fed is not something new and the dollar’s positive performance today is a testament to that.

Looking at the calendar, at 1230 GMT, US producer prices for September are scheduled to be released. Predictions are for the headline PPI to remain steady at 2.8% y/y, while on monthly basis it is expected to accelerate to 0.2% from -0.1% in the previous month. Excluding food and energy items, core producer prices are anticipated to rise to 2.5% y/y from 2.3% y/y before. These prints may raise some speculation that US CPIs – due out tomorrow – could move in a similar direction, driving the US dollar higher in case the numbers pop up better than expected.

Readings on US wholesale inventories will be available at 1400 GMT.

In Canada, building permits for the month of August will be delivered at 1230 GMT, with analysts predicting the gauge to inch up to 0.5% m/m versus a decline of 0.1% in the prior month.

Later in the day, at 2350 GMT, Japan will publish PPI stats, though as usual the yen is not expected to react much on the data.

In energy markets, investors will be waiting for the API weekly report to indicate the change in US crude oil stocks for the week ending October 1, at 2030 GMT.

Six months before Britain leaves the EU, markets are positive that a deal related to divorce terms could be secured before the EU summit kicks off on October 17-18. Today people familiar with Brexit negotiations in Brussels reported that the EU is not expecting any new proposals on the Irish border from Britain and that both sides are working to narrow existing differences. Still, they remained optimistic that intense talks between the sides in the next five days could find a solution to the Irish backstop by Monday.

Elsewhere, numerous speeches are on the agenda. At 1400 GMT, the EU’s Brexit negotiator Michel Barnier will be speaking at the European Parliament, while regional Fed Presidents Charles Evans (non-voting member in FOMC in 2018) and Raphael Bostic (voting member) will be making remarks at 1615 GMT and 2100 GMT respectively. The day ends with a speech by Luci Ellis, RBA Assistant Governor at 2230 GMT.