{kind=link}

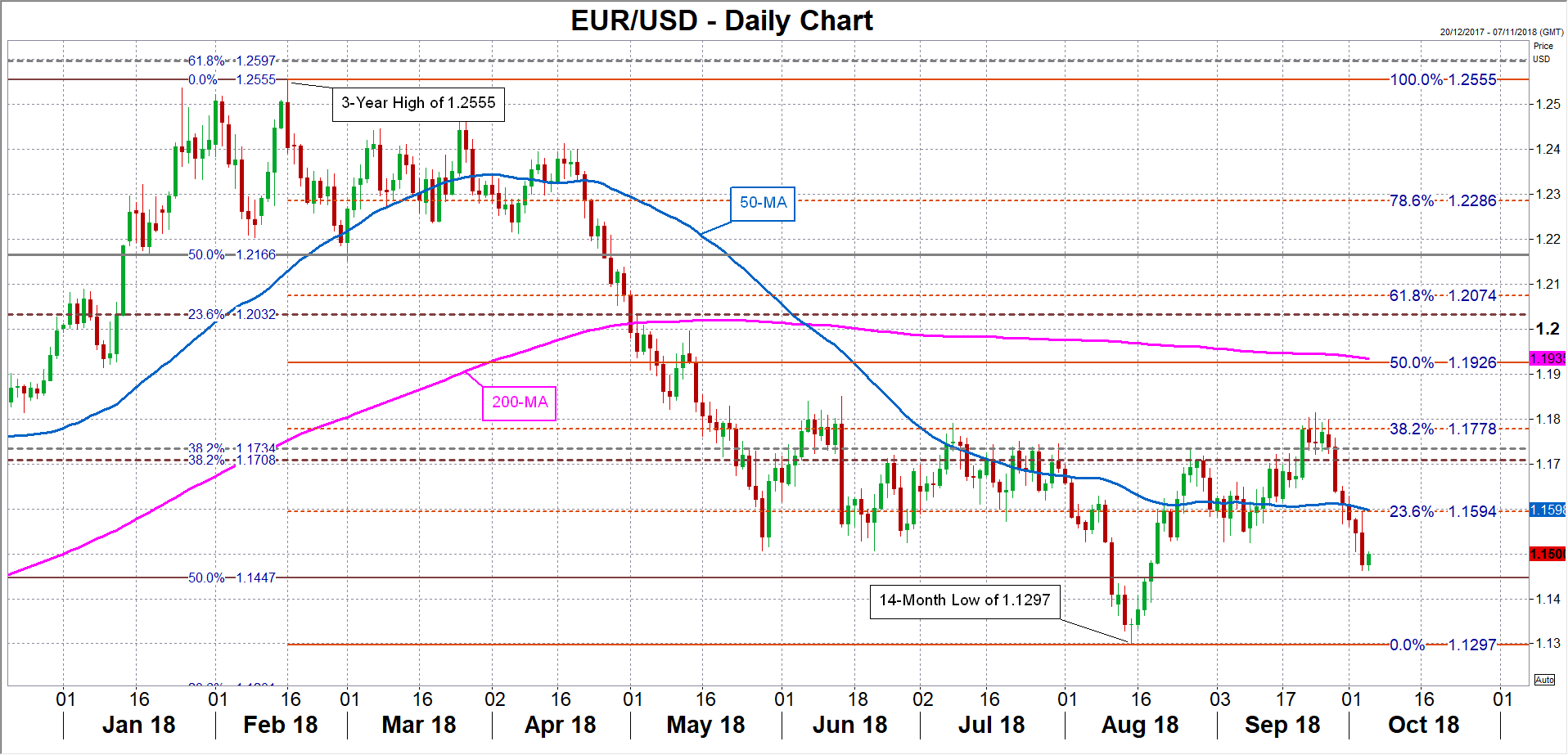

The euro has retreated by about 8% from its three-year peak scaled back in February when it briefly touched $1.2555. At the time, the outlook for the Eurozone economy was looking increasingly positive and political uncertainty appeared to be receding. However, since the spring, economic indicators out of the Eurozone have consistently fallen short of expectations, whereas in the US, they’ve gone from strength to strength. With Eurozone growth struggling to regain momentum and the added risks from global trade tensions and political troubles in Italy, the euro’s recovery is becoming worryingly elusive.

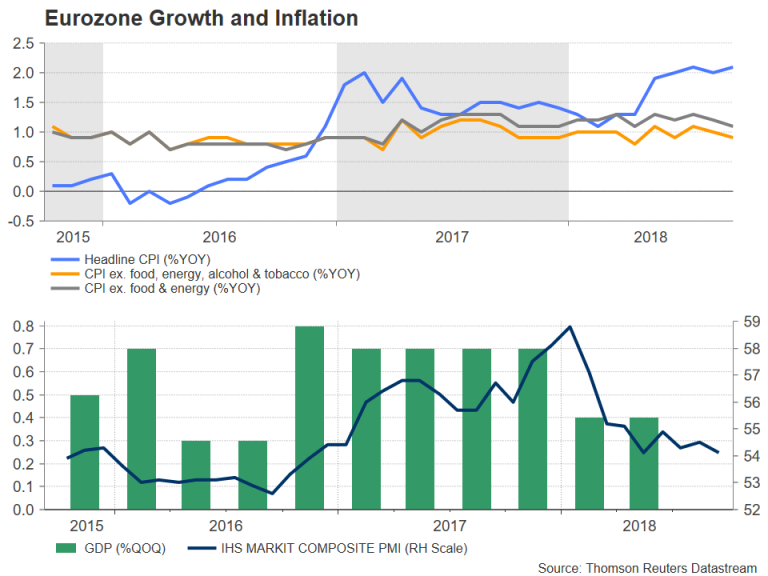

After churning out growth of 0.7% quarter-on-quarter throughout 2017, the pace of economic expansion has almost halved in the first half of 2018 to 0.4%. The slowdown was initially thought to be temporary, but the region’s PMI indicators, which accurately track GDP growth, suggest a rebound is no nearer. Progress on the inflation front has been more evident, at least in the headline rate, which has returned to around 2%, slightly above the ECB’s target of close but below 2%. However, despite some recent hawkish remarks by ECB President Mario Draghi on the underlying price trend, core measures of inflation have been mostly flat over the past year around 1%.

Nevertheless, the European Central Bank is moving ahead with its plans to unwind its asset purchase program be the year-end, with the first rate rise expected to be delivered in the autumn of 2019. The ECB’s long-awaited decision to end its bond buying program was itself negative on the euro as Draghi set out a much more dovish path to normalize policy than the markets had been anticipating.

More recently, the threat of US tariffs on European car imports – which has not completely dissipated as the United States and the European Union have only held preparatory talks on trade so far – and concerns about the effects on global growth from the US-China trade dispute have dampened business confidence in the euro area, particularly in export-dependent Germany.

Adding to the somewhat gloomier outlook for Eurozone businesses is fresh political turmoil in Italy. There was relief at the beginning of May when two of Italy’s populist parties reached a deal to form a coalition government, averting a snap election and further uncertainty. It followed a similar breakthrough in March for Germany’s Angela Merkel when she secured a grand coalition deal to keep her in power and ended months of deadlock.

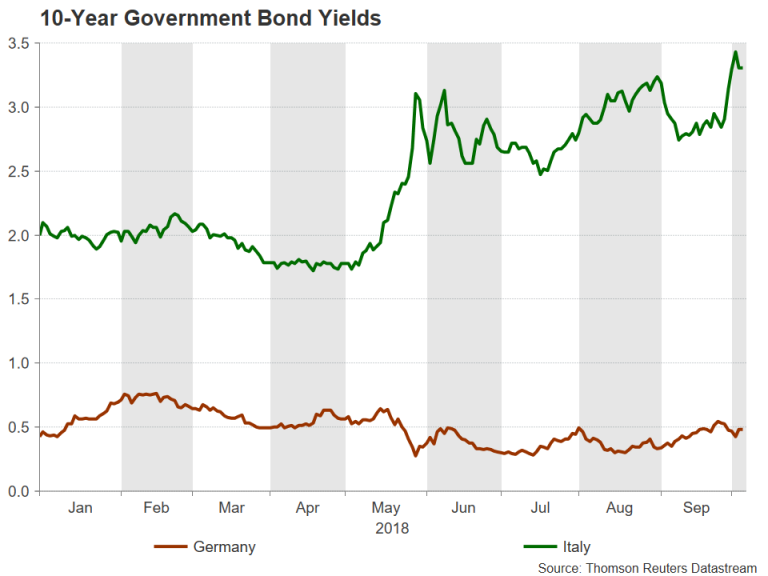

But as is common in Europe, there’s always a new political or economic headache waiting around the corner and there is a threat that the latest stand-off between Italy and the EU could escalate into a much bigger crisis. While few think that Italy would quit the euro bloc should the European Commission not approve the coalition’s budget deficit plans for 2019-2021, prolonged wrangling between Italy’s outspoken leaders and EU officials could upset the markets further and drive Italian government bond yields even higher.

The euro tends to fall whenever periphery bond yields rise sharply above German bund yields and the latest episode with Italy has been no different for the single currency. With the Italian government not looking likely to back down easily over its plans to boost spending in 2019, the euro’s near-term outlook remains tied to the outcome of how the budget saga is resolved.

Should the EU reject Italy’s latest budget proposals, it’s difficult to see the government making further concessions. It’s unclear how the EU would respond to Italy refusing to follow fiscal discipline rules, but such a scenario has the capacity to pull the euro below the yearly low of $1.1297 touched on August 15, which was the weakest in almost 14 months. Before arriving at that bottom though, euro/dollar might seek a more nearby support at around $1.1450, which is the 50% Fibonacci retracement of the January 2017-February 2018 uptrend. Should the pair breach the 2018 trough of $1.1297, attention will fall on the $1.12 handle, as it’s just above the 61.8% Fibonacci retracement and a drop below would signal a deeper bearish phase.

Looking at the more medium- to longer-term prospects for the euro, this would depend not only on whether or not growth in the Eurozone picks up a couple of gears, but also on how the US economy fares in 2019. Assuming the situation in Italy doesn’t develop into a new debt crisis and the tariff war remains confined to US-China, the euro area should continue expanding at a satisfactory pace. Even if growth doesn’t accelerate significantly, inflationary pressures should gradually heat up, as there is already evidence that rising employment levels across the Eurozone are starting to push up wages, and this would enable the ECB to proceed with its rate hike cycle in late 2019.

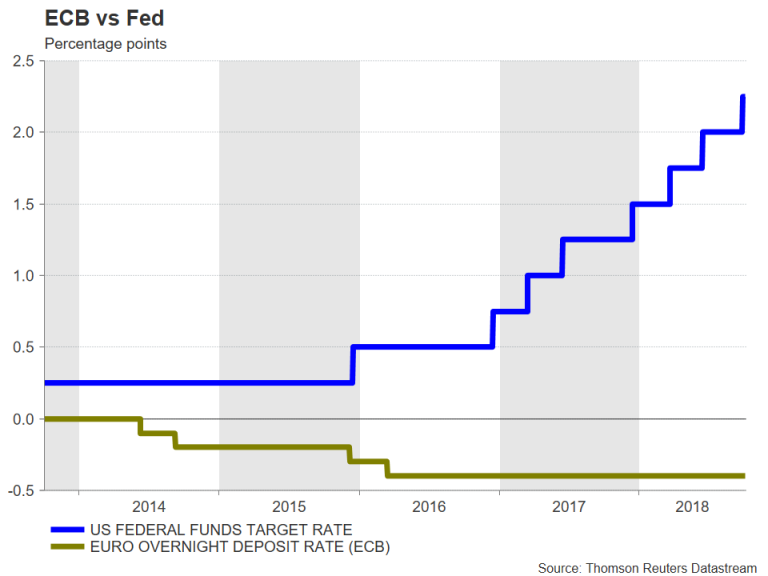

Until then though, the euro could struggle to make significant headway as the interest rate differential between the US and the Eurozone continues to widen. There is a possibility the Federal Reserve would slow down or pause the pace of rate increases in 2019, with several factors that could potentially cause the US economy to lose steam. These range from the tax cut effects fading out, Trump’s trade war hurting the many US companies closely tied to China, to the cumulative rate hikes since 2015 starting to bite the economy.

But a US slowdown doesn’t necessarily have to materialise before the ECB begins lifting rates for the euro to advance higher, as any early indication by the Fed that interest rates are nearing the peak of their current cycle would place the dollar on a downward path.

The single currency’s immediate focus on the upside is the $1.17 level, as it’s yet to make a sustained break above it after losing the handle back in May. Higher up, the next major barrier to beat is the $1.1780 area, which is the 38.2% Fibonacci retracement of the February-August down move. This region has been a strong resistance point to overcome and the euro has been unable to close above the $1.18 level since May despite several attempts. A convincing break above $1.18 would open the way to the 50% Fibonacci at $1.1925, which if cleared, would set a more bullish tone in the short term.

However, in the longer run, euro/dollar would need to challenge the three-year top of $1.2555 and make a move for the $1.26 level to confirm a resumption of the 2017 uptrend. It’s worth pointing that the $1.26 handle is just above the 61.8% Fibonacci retracement of the 2014-2016 downtrend, so the pair would need to surpass this level to return to a long-term bullish structure. Such a shift can only occur though, if the monetary policy divergence between the Fed and the ECB comes to an end and the yield differential starts to narrow in favour of the euro.