{kind=link}

Here are the latest developments in global markets:

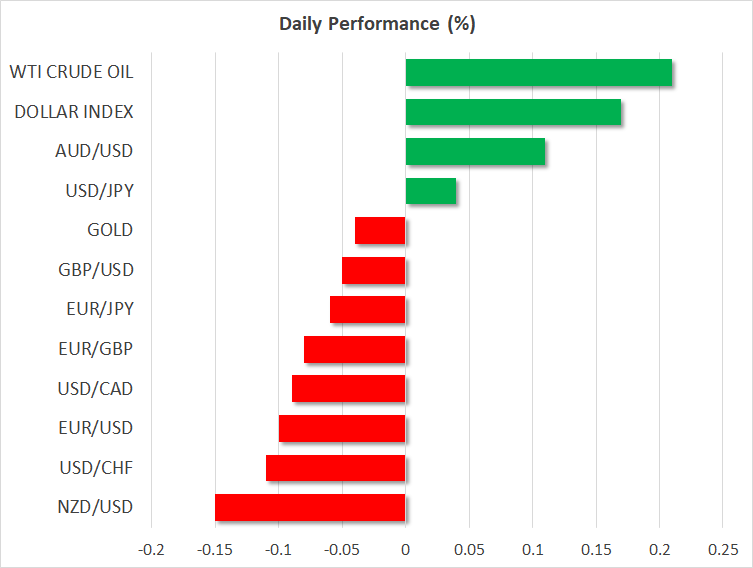

FOREX: The dollar is higher by 0.17% against a basket of six major currencies on Friday, extending the significant gains it recorded in the previous session. The euro, which holds the largest weight by far among those six currencies, edged lower as concerns around the Italian budget intensified.

STOCKS: Wall Street roared back on Thursday, with all the major indices closing in the green, aided by gains in tech giants like Apple (+2.06%), Google-parent Alphabet (+1.11%), and Facebook (+1.13%). Accordingly, the tech-heavy Nasdaq Composite outperformed (+0.65%) the benchmark S&P 500 (+0.28%) and the Dow Jones (+0.21%). In company-specific news, US regulators (SEC) announced after markets closed they are suing Tesla CEO Musk for fraud due to his “misleading” tweet a few weeks ago, sending the electric car-maker’s share price sharply lower in after-hours trading. In Asia, most indices were flashing green on Friday, with Japan’s Nikkei 225 (+1.36%) and Topix (+0.95%) recovering, the former touching a 27-year high. In Hong Kong, the Hang Seng was down by a marginal 0.07%. Europe was a different story, with all benchmarks expected to open much lower today according to futures, amidst worries around Italy (see below).

COMMODITIES: Oil traded higher, albeit only modestly, with some media reports that Saudi Arabia may increase its production by up to 600k barrels per day in the final quarter of the year having little effect on prices. WTI is higher by 0.21% at $72.27 per barrel, while Brent gained 0.12% on Friday, trading at $81.82 a barrel. In precious metals, gold is little changed on Friday, licking its wounds following a notable tumble in the previous session that caused it to exit to the downside the narrow range it had been trading in for a month. The losses came as the greenback surged, rendering the dollar-denominated yellow metal more “expensive” for investors using foreign currencies.

Major movers: Dollar firms on upbeat data; Italian worries drag euro lower

“King dollar” made a return on Thursday. The world’s reserve currency soared across the board, propelled higher by another round of robust US economic data, with broad-based weakness in the euro amidst Italian budget angst also lending a hand. Euro/dollar plunged to find a bottom around 1.1640, from an earlier intraday high of 1.1755. Meanwhile, dollar/yen raced as high as 113.63 – recording a fresh 9-month high – before pulling back a little, also buoyed by strong risk appetite.

As for catalysts, the greenback got a push higher after US durable goods orders for August surprised to the upside, painting a brighter picture for GDP growth in Q3. Adding further credence to this, were the details of the final GDP release for Q2, which showed that inventory-rebalancing by firms shaved more than 1 percentage point away from Q2 GDP. Hence, assuming firms restocked their inventories in Q3, the next GDP print may well show inventories adding to growth.

Even more important for the dollar’s ascend, was the softness in the euro, which was hammered lower by renewed concerns around the Italian budget. The Italian government stated yesterday the budget deficit will be 2.4% for the upcoming year, higher than the 1.9% – 2.0% that had been rumored. While this is still safely below the 3.0% deficit limit set by the EU’s Maastricht Treaty, and admittedly not a gigantic difference relative to expectations, markets still interpreted this as a sign of “fiscal indiscipline” – sending Italian bond yields across all maturities higher and dragging the euro lower. Market chatter even suggests the wider deficit may lead to major ratings agencies downgrading Italian debt. Uncertainty on this front will likely keep a risk-premium on the euro for the time being, perhaps until the official budget is submitted on October 15.

Elsewhere, there was little of note in the FX market, with most pairs simply following the dollar-strength trend. Sterling/dollar fell back below 1.3100, with the next source of volatility for sterling likely to be the Conservative Party conference that commences on Sunday. Two key areas of focus may be any Brexit remarks, especially following the recently-leaked EU papers hinting at “free trade areas”, and any hints that hardline Brexiteers could seek to challenge Theresa May’s leadership in case they are dissatisfied with any “soft” deal she negotiates.

Day ahead: Eurozone flash inflation, US core PCE, UK & Canadian GDP on the agenda

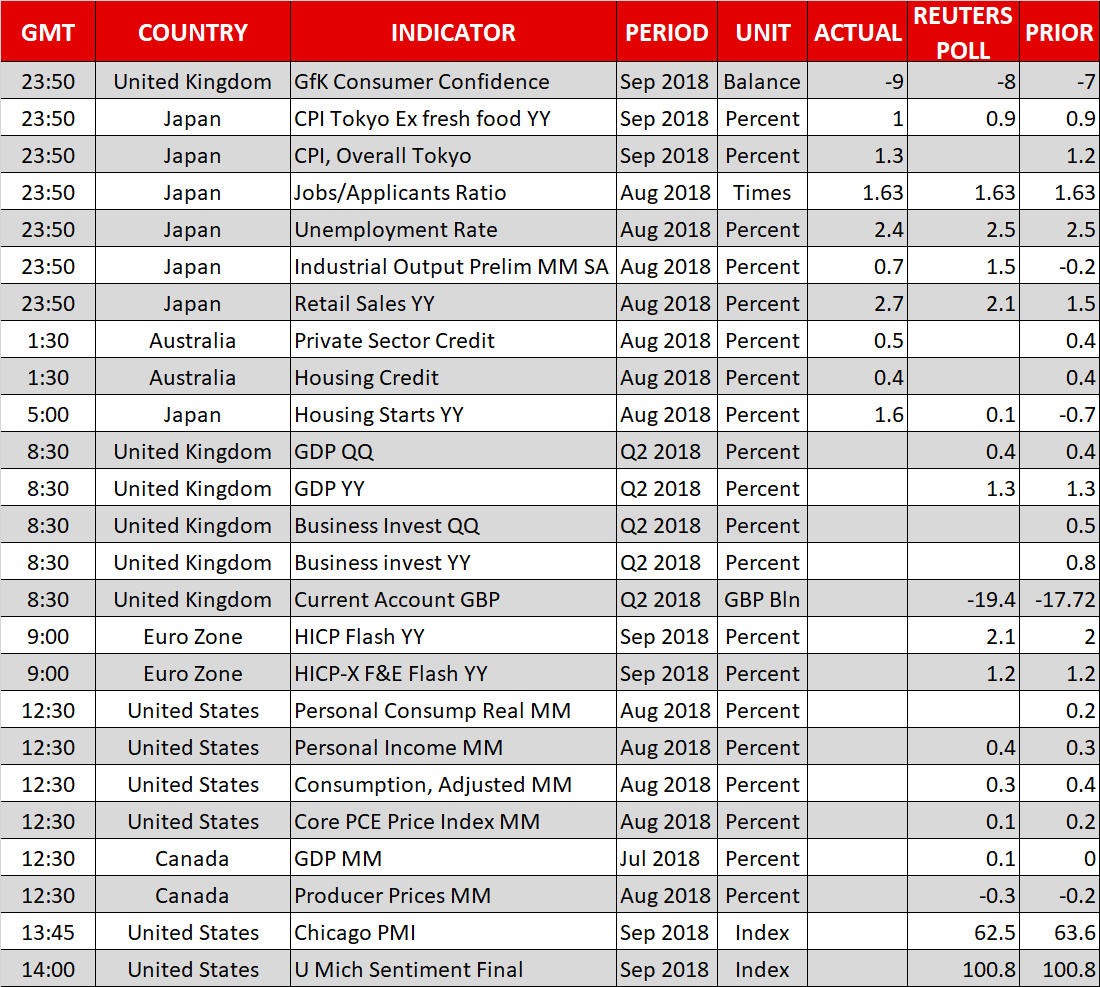

Eurozone preliminary inflation figures for September and US core PCE data are among the releases generating attention in Friday’s calendar.

At 0830 GMT, revised Q2 GDP estimates out of the UK are anticipated to confirm the quarterly and annual pace of growth at 0.4% and 1.3% respectively, above Q1’s equivalent figures of 0.2% and 1.2%. Data on Q2’s business investment and the current account will be made public at the same time. A risk event for sterling will be the Conservative Party conference commencing on Sunday.

The eurozone will be on the receiving end of flash inflation numbers for September. Annually, headline inflation is expected to rise by 2.1%, which compares to August’s 2.0% and the ECB’s target of “close to but below 2%”. The core rate of inflation that excludes volatile food and energy items is projected to stand at 1.2% y/y, the same as in August. Earlier in the week, ECB chief Draghi said he sees a vigorous pickup in inflation, something which led to a jump in the euro. It remains to be seen whether today’s prints will start confirming his views.

Also euro-related, Germany will see the release of unemployment data for September earlier in the day (0755 GMT). The unemployment rate in Europe’s largest economy is forecast to remain at 5.2%, the lowest since the country’s reunification back in 1990.

The attention will next turn to the US, where the Fed’s preferred inflation gauge, the core PCE price index, is due at 1230 GMT. The measure is predicted to rise by 0.1% m/m in August (vs 0.2% in July), something which would allow the annual rate to remain at the 2.0% mark that coincides with the US central bank’s target for inflation. The readings on August’s personal income and consumption are also due at 1230 GMT. The two are anticipated to expand by 0.4% and 0.3% m/m, after rising by 0.3% and 0.4% correspondingly in July.

Other US releases on Friday are September’s Chicago PMI (1345 GMT) and the University of Michigan’s final survey on consumer sentiment (1400 GMT), both for the month of September.

Numbers on Canadian economic activity for July will be hitting the markets at 1230 GMT, with the growth rate expected at 0.1% m/m, after June’s stagnation. Canadian OIS project a 77% chance for a late October hike by the Bank of Canada and upbeat data today and in the coming weeks can push that closer to a done-deal; the opposite holds true as well. August producer prices out of the nation are due at the same time.

Elsewhere, Turkish President Erdogan and German Chancellor Merkel will be speaking to reporters at 1030 GMT following their meetings aiming to restore ties and improve relations between the two nations. Irish Central Bank Governor and ECB policymaker Lane and Bank of England member Ramsden will be talking at 1130 GMT; the latter will be returning to the rostrum at 1320 GMT. Other policymakers on the agenda are ECB’s Praet (1235 GMT), and regional Fed Presidents Barkin (1230 GMT) and Williams (2045 GMT) – they both hold voting rights within the FOMC in 2018, with Williams having permanent voting rights given that he chairs the NY Fed.

In energy markets, the weekly Baker Hughes report on active oil rigs in the US is scheduled for release at 1700 GMT.

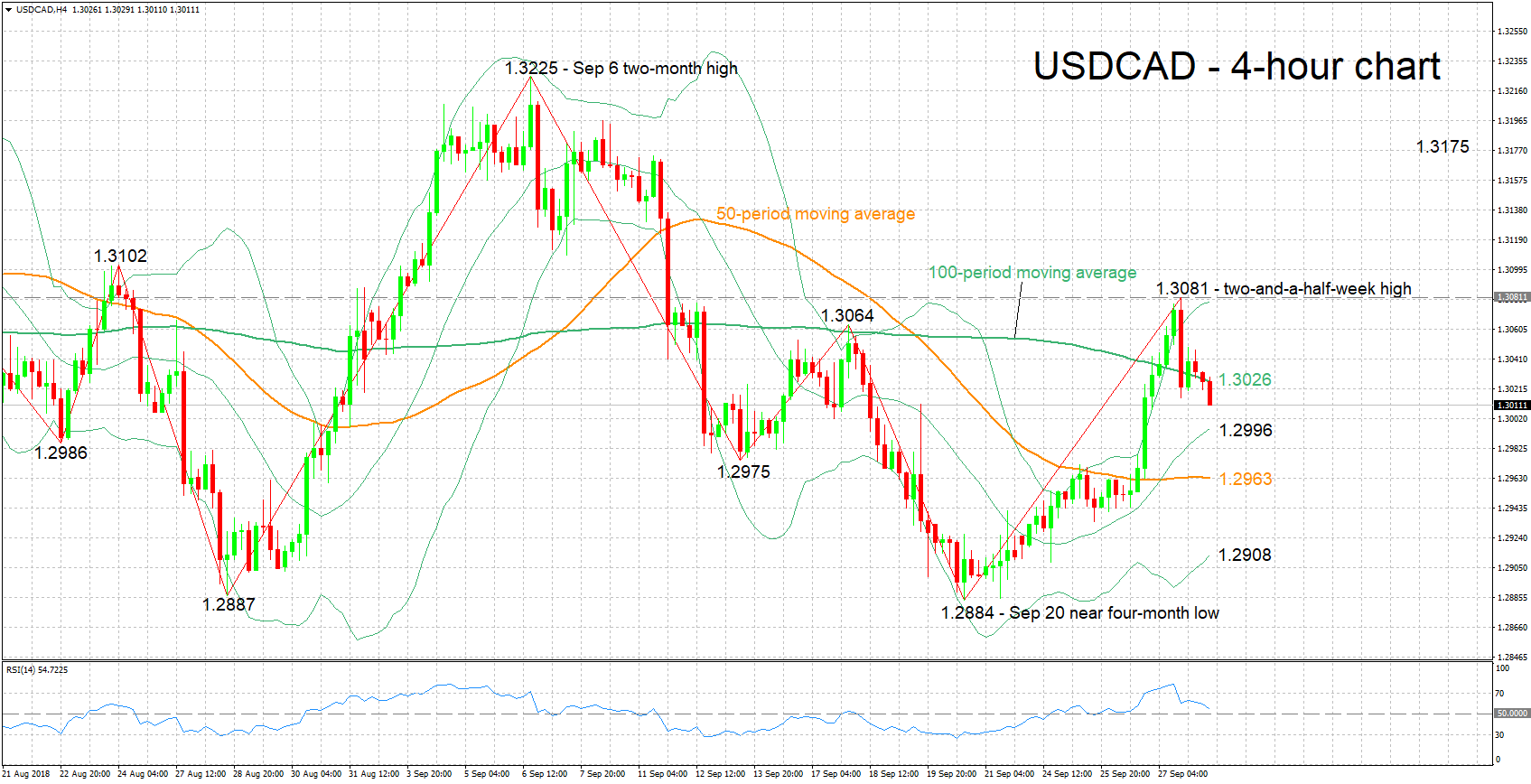

Technical Analysis: USDCAD near-term momentum could be shifting to the downside

USDCAD lost ground after touching a two-and-a-half-week high of 1.3081 during Thursday’s trading. The RSI entered a path of declines after previously rising into overbought territory. Its fall is signaling a change in short-term momentum to the downside.

Upbeat Canadian GDP numbers can push the pair further down. Immediate support to losses may come around the middle Bollinger line – a 20 period moving average line – at 1.2996 and the 50-period MA at 1.2963. Further below, the attention would turn to the zone around the lower Bollinger band at 1.2908 and the near four-month low of 1.2884 from September 20.

Conversely, disappointing Canadian figures are expected to lift USDCAD. Given a move above the 100-period MA at 1.3026, resistance could occur around yesterday’s high of 1.3081, while further above, the region around 1.3175 was congested earlier in September and may hold significance, acting as a barrier to gains.

US data out on Friday can also move the pair.