{kind=link}

Here are the latest developments in global markets:

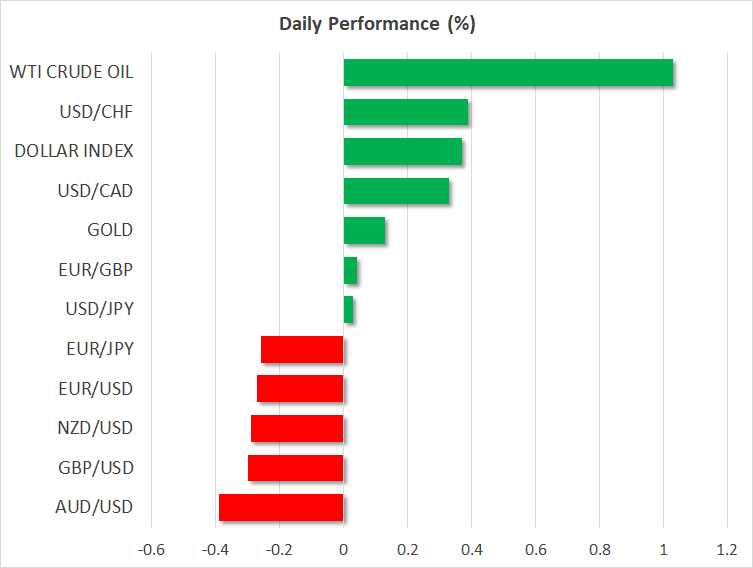

FOREX: The dollar flattened around 112.72 versus the yen early in the European session, while relative to six major currencies the greenback was in a better position, gaining 0.36% on the back of a weaker euro and pound. Euro/dollar was struggling to recoup earlier losses triggered by news that the Italian budget meeting may be postponed. Following the worrying news, however, the Prime Minister’s office confirmed that discussions will be held today (see below). As for data releases out of the Eurozone, the economic sentiment index came in worse than expected, while final readings on consumer confidence appeared in line with initial forecasts, showing that consumers’ pessimism deteriorated to 1 ½-year lows in September. The August mark, though, was revised up to -1.9. Euro/dollar was down on the day at 1.1713 (-0.22%). Pound/dollar was on the back foot as well, changing hands at 1.3128 (-0.33%) as anxiety about Brexit and the Fed’s optimism on the US economy continued to pressure buying interest in the market. In antipodean currencies, aussie/dollar and kiwi/dollar were in bearish mode, fluctuating at 0.7230 (-0.36%) and at 0.6635 (-0.30%) correspondingly. Note that the Reserve Bank of New Zealand kept interest rates steady on Wednesday as expected and maintained cautious economic outlook, reiterating that the next move in rates could be up or down. In contrast, on the same day, the Fed raised borrowing costs and signaled further monetary tightening in the coming years as anticipated. Surprisingly, though, it dropped the description that monetary policy is accommodative in the rate statement. Dollar/loonie was enjoying gains around two-week highs (+0.30%).

STOCKS: The majority of European equities were trading lower on Thursday at 1120 GMT as investors got stressed about the Italian 2019 budget, pushing the Italian FTSE MIB down by 1.20%. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 declined by 0.14% and 0.08% respectively. The German DAX 30 dropped by 0.15% led by losses in utilities and industrials. The French CAC 40 retreated by 0.05% and the Spanish IBEX 35 fell by 0.54%. The British FTSE 100, however, managed to hold in the positive territory, trading higher by 0.22% after Deutsche Bank said that British shares would outperform European ones if the UK leaves the Union without an agreement on the divorce terms. In Asia, stocks closed weaker, with Japanese shares losing the most. In the US futures, tracking the S&P 500, Nasdaq 100 and Dow Jones were mixed.

COMMODITIES: Crude oil prices managed to fully recover yesterday’s downside on prospects that prices could go even higher in the wake of US sanctions against Iranian oil exports due in November. In the meantime, sources with knowledge of the matter reported that Saudi Arabia will increase output in the next few months to replace supply shortages in Iran, though it fears that next year it might have to cut output if the US pumps more oil. WTI crude and Brent rallied to $72.27/barrel (+0.98%) and $81.99/barrel respectively (+0.79%). In precious metals, gold was last seen at 1,196.68 (+0.22%).

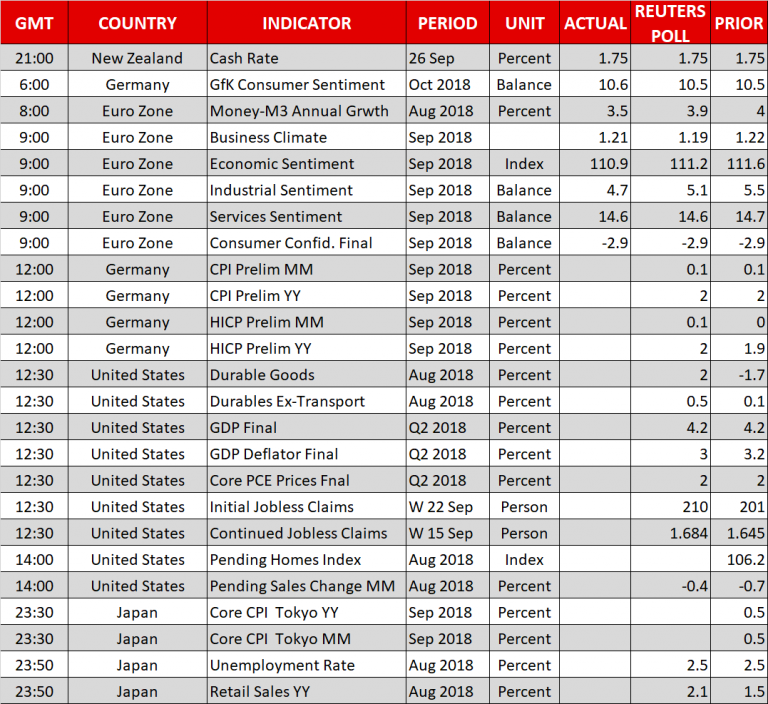

Day Ahead: US durable goods & Q2 GDP final figures awaited; German CPI & Japan unemployment rate pending

Looking ahead to the rest of the day, the US, Germany and Japan are scheduled to report economic figures, while there are plenty of public appearances for traders to have in mind.

German preliminary inflation figures for the month of September will be available for review at 1200 GMT. Expectations are for the nation’s EU-harmonized inflation rate to rise by 2.0% in yearly terms, the same pace as before, while on a monthly basis the figure is forecast to remain steady as well at 0.1%.

Out of the US, weekly jobless claims – initial and continued – due at 1230 GMT will be gathering attention. The number of initial benefits claimants for the week ending September 22 is anticipated to be 210k, little changed from the preceding week’s 201k. The world’s largest economy will also see the release of August durable goods. Headline orders are expected to rise by 1.9% m/m from -1.7% m/m in the preceding month, whilst the core durable orders (excluding transportations equipment) is forecast to inch up by 0.5% m/m from 0.1% m/m before. In addition, the final GDP growth estimate due at 1230 GMT is predicted to remain unchanged at 4.2% q/q in the second quarter. Also, the core PCE prices will come into view at the same time, while at 1400 GMT the focus will shift to pending home sales. The US dollar is still trading higher versus major currencies and stronger-than-expected data prints could help the greenback to extend gains later in the day.

Overnight at 2350 GMT, Japan’s unemployment rate for August will get published. The unemployment rate is predicted to remain the same at 2.5%, while the preliminary figures on industrial production are anticipated to rebound by 1.5% m/m from a decline of 0.2% previously. Retail sales for the month are forecast to tick higher by 2.1% y/y from 1.5% the prior month. The BoJ’s summary of opinions from its latest policy gathering is due to be released as well. A bit earlier, the Tokyo CPIs for September will also come out.

Meanwhile in the Eurozone, the focus will stay on Italy where the 2019 budget meeting is scheduled at 1800 GMT according to the Prime Minister’s office, while pre-meeting talks are also said to take place at 1400 GMT. News of delays in the budget meeting and echoes of resignation for the Italian Finance Minister announced earlier hint that discussions could be surrounded by conflicts.

Numerous speeches are on the agenda today with the BoE policymaker Haldane speaking at 1145 GMT, ECB President Mario Draghi at 1330 GMT and Bank of England Governor Mark Carney at 1400 GMT. ECB chief economist Praet will be making remarks too at 1700 GMT. In the US, Dallas Fed President Robert Kaplan will be talking at 1800 GMT, while later at 2030 GMT remarks on the US economy by the Fed Chair Jerome Powell will attract greater attention. At 2145 GMT, comments by the BoC Governor Steven Poloz could be of interest too.

Today, a two-day meeting is starting between the Turkish President Tayyip Erdogan, German Chancellor Angela Merkel and President Frank-Walter Steinmeier in Germany with scope to improve relations between the two countries.