{kind=link}

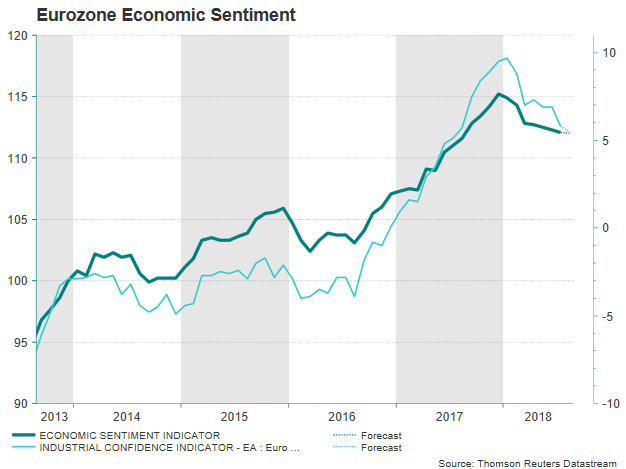

The European Commission is delivering its monthly consumer and business survey results on Thursday at 0900 GMT and forecasts signal that economic sentiment in the 19 countries sharing the euro currency has deteriorated even further in August. While an upside surprise could move the euro higher, traders may stay cautious on their positioning until Eurozone’s August preliminary inflation numbers come out on Friday at 0900 GMT, as those could generate larger volatility to the market given their direct impact on the European Central Bank’s appetite for future rate hikes. Note that price stability is the primary objective of the ECB.

In July, the Eurozone Economic Sentiment index (ESI) pulled back by 0.2 points to 112.1, touching a one-year low, and extending its downtrend from December’s peak of 115.3. The weakness in the index appeared to worsen as managers expectations on future production levels, current order books and stocks of finished goods turned more pessimistic on the back of US steel and aluminum import tariffs as well as on Washington’s warnings of more tariffs on EU cars, pushing the industrial sentiment index lower to 5.8.

New ESI data on Thursday though are not expected to show any improvement yet as analysts believe that in August the measure inched down to 112.0. Meanwhile, its industrial component is anticipated to drop to 5.5, probably reflecting the additional pressure businesses felt on the face of the ongoing US-Chinese tit-for-tat trade game and the inability of these trading powers to find a common ground.

However, Trump’s agreement with the President of the European Commission, Jean Claude Junker, to refrain from imposing tariffs on EU automobiles and continue negotiations could have calmed worries. As much is evident from the latest German Ifo business sentiment data, which surprisingly indicated a stronger recovery than analysts had forecasted, posting the first increase since November. First estimates on the Eurozone’s composite Markit PMI for the month of August also indicated an improvement but disappointingly only a marginal one, while the manufacturing PMI retreated further to the lowest since November 2016. As regards the sentiment in the services sector, the corresponding index is projected to come at 15.1, losing part of last month’s positive momentum which drove the measure to 15.3, the highest since March.

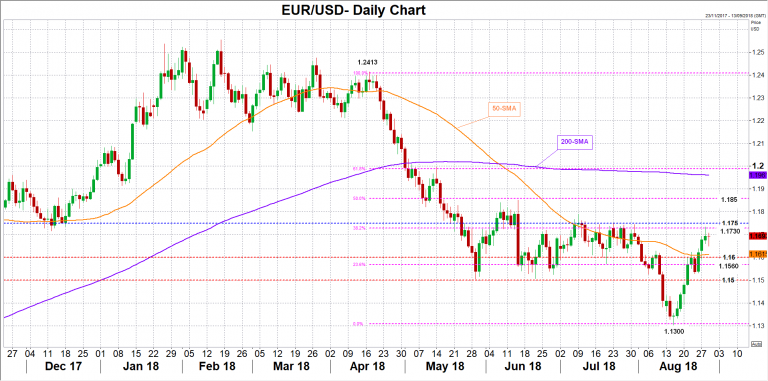

In FX markets, euro/dollar has fully recovered losses made earlier this month, spiking slightly above the 1.1700 key level on Tuesday after touching the more-than-a-year low of 1.1300. Upbeat ESI numbers on Thursday may add hopes that GDP growth in the eurozone could do better in the third quarter, helping the pair to surpass the 1.1700 round level again to hit 1.1750, which the market found difficult to pierce in July. Beforehand, however, bulls would need to overcome 1.1730, which is the 38.2% Fibonacci of the downleg from 1.2413 to 1.1300. A bigger positive surprise in the data could also bring the 50% Fibonacci of 1.1850 on the radar.

On the other hand, a data miss could send the price down to the 1.1600 round level, near the 50-day simple moving average, while slightly lower, the area between the 23.6% Fibonacci of 1.1560 and the 1.1500 mark may attract attention as well ahead of the 1.1300 low.

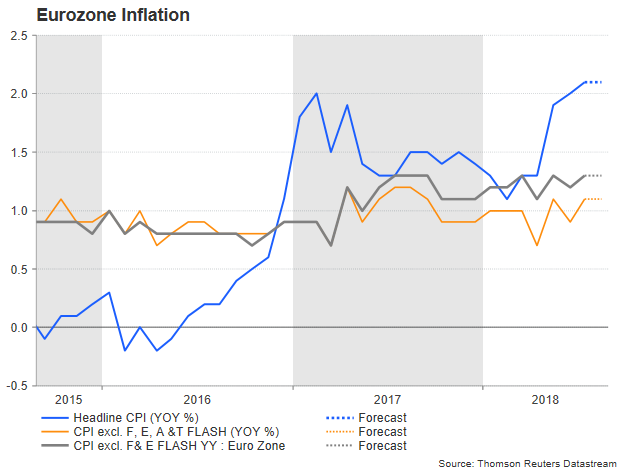

It should be pointed out, however, that investors might react less than usual in the wake of the data, showing patience ahead of the flash harmonized CPI figures out of the bloc on Friday. Initial estimates are anticipated to message that consumer prices overall have grown at a pace of 2.1% y/y in August, the same as in July, expanding at the highest pace since January 2013 and marginally above the ECB’s 2.0% inflation target. Excluding food and energy products, the core measure is also expected to show no change, holding at 1.3% y/y, while the gauge deducting alcohol and tobacco too is seen steady, at 1.1% y/y.

As the termination of the quantitative easing program (QE) by the end of this year is already a well-known story, the focus has switched back into interest rates. Minutes of the latest ECB meeting in July clarified that the central bank won’t do anything about rates until the end of summer 2019, with markets estimating the first hike to come only in October or December next year.

The unpredictable and risky US trade policy, as well as the recent slowdown in the Eurozone’s GDP growth, are among factors that refrain policymakers from raising borrowing costs and should inflation numbers unexpectedly pull back on Friday, the odds for an after-summer rate hike next year could weaken, driving the euro to the aforementioned support levels. Alternatively, if consumer prices advance by more than analysts predicted, taking another step above the ECB’s price target, that could boost the common currency towards resistance levels underlined above as investors would probably turn more confident that a rate hike is on the way.