{kind=link}

Euro climbs ahead of ECB meeting

While we may not look back at the ECB meeting on Thursday as one of the defining moments in the eurozone’s long recovery from the global financial and debt crises, or even remember it much at all for that matter, that doesn’t mean there won’t be anything to take away from it, or that markets won’t react.

- ECB left little to the imagination in June

- Never a good idea to assume an uneventful meeting

- Will Draghi succeed in talking down the euro again?

At its meeting last month, the ECB laid out plans for its bond buying program (quantitative easing) beyond the current expiry date of September, opting to extend it until the end of the year at half the pace – €15 billion – and warned that interest rates will remain at present levels “at least through the summer of 2019”.

In providing such a clear path for asset purchases and interest rates for the next year, the central bank effectively covered all bases and barring a significant shift in the data or a change in the global landscape, left few questions if any to be answered, making this meeting a potential non-event.

Should we ever anticipate a “non-event”?

One thing we’ve learned in the past though is not to become complacent when the central banks are involved and in the current environment of trade conflicts and Brexit, things can change very quickly. We have to remember that while the recovery is gathering momentum and making encouraging progress, it is still fragile and could be derailed by a number of events which would require the ECB to step back in and offer its support.

Only this week it has been reported that US President Donald Trump intends to slap 25% tariffs on European auto imports and significantly escalate the trade conflict between the US and EU. Jean-Claude Juncker is currently in Washington looking to calm the growing tensions between the two but it seems that unless he is offering concessions, he may not get very far.

What’s more, the UK and EU don’t appear to be getting much closer to agreeing on the divorce and with eight months to go until exit day, this is a notable downside risk for both economies, with the IMF recently warning that a no-deal Brexit that sees the two revert to WTO rules could wipe 1.5% and 4% off EU and UK output, respectively, by 2030.

In terms of the data, the ECB will likely be relatively content, with unemployment continuing to drop – now at 8.4%, the lowest since December 2008 – the economy growing well despite the dip in the first quarter and inflation gradually increasing, albeit less so on from a core perspective. Nothing has really changed on this front since the last meeting that will concern policy makers.

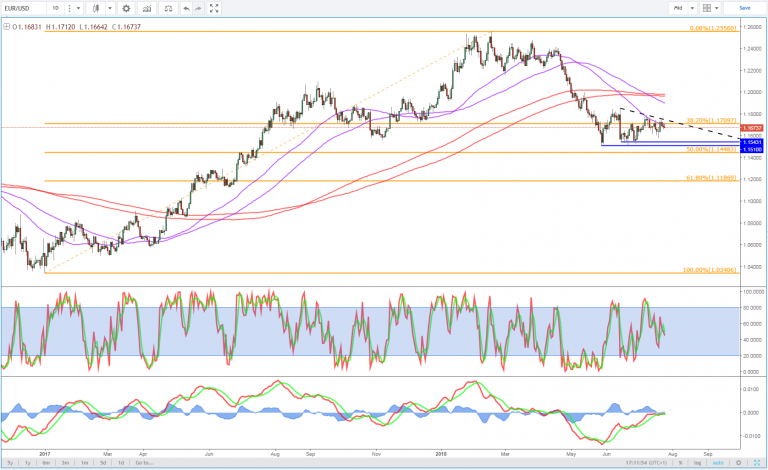

While the euro has been climbing over the course of the last month, after falling following the ECB announcement and very dovish accompanying statements, it’s now only trading back where it was before the meeting which will be a relief to policy makers. It will be interesting to see if anything they say changes this or if Draghi focuses on talking it lower once again.