{kind=link}

Thursday April 20: Five things the markets are talking about

Current price action suggests that investors continue to pare back ‘risk-on’ market positions ahead of this weekend’s first round of the French Presidential election.

Geopolitical worry over North Korea, a faltering U.S economy and a snap U.K election are also consuming investor’s mindsets.

A race too close to call – every French poll for the past month has shown the independent Macron and the National Front’s Le Pen taking the top two-spots. Macron is then expected to easily win the May 7 runoff by a +25% margin.

However, both front-runners have been steadily slipping over the past fortnight, and Republican Francois Fillon and Communist-backed Jean-Luc Melenchon are now within striking distance.

Nevertheless, Millions of French voters remain undecided, making this the least predictable vote in France in decades.

1. Stocks stick to tight ranges

Global stocks eked out small gains overnight as investors resisted risky bets ahead of the first round of the French presidential election.

In Japan, the broader Topix index added +0.1%, bringing its weekly gain to +0.9%, while the Nikkei 225 share average ended -0.01% lower.

In Hong Kong, the Hang Seng advanced +0.7%, while down-under the Aussie S&P/ASX 200 Index climbed +0.3%, while South Korea’s Kospi index was up +0.5%.

In China, the Shanghai Composite was little changed, after four days of losses brought it to the lowest level since early February.

In Europe, equity indices are trading generally higher as market participants continue to focus on the upcoming French presidential elections. Banking stocks are supporting the Eurostoxx, while energy, commodity and mining stocks are trading lower on the FTSE 100.

U.S stocks are set to open in the black (+0.3%).

Indices: Stoxx50 +0.5% at 3,440, FTSE -0.1% at 7,105, DAX +0.2% at 12,034, CAC-40 +0.9% at 5,048, IBEX-35 +0.9% at 10,461, FTSE MIB +0.4% at 19,907, SMI +0.4% at 8,564, S&P 500 Futures +0.3%

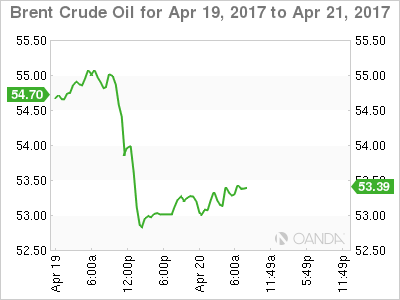

2. Oil prices claw back losses, but oversupply still weighs, gold higher

Oil prices have regained some ground overnight after yesterday’s steep losses, as Kuwait said it expected an OPEC-led effort to cut supplies would be extended into H2.

Brent crude futures are at +$53.34 per barrel, up +41c, or +0.77% from last nights close. U.S. West Texas Intermediate (WTI) crude futures are up +32c, or +0.63%, to +$50.76 a barrel.

Also supporting prices was yesterday’s data from the EIA, which showed a reduction in commercial U.S crude stocks, which fell by -1m barrels last week to +532.34m barrels.

Note: Crude prices fell -3.5% Wednesday after the EIA reported surging gasoline inventories as well as another rise in U.S crude oil production to +9.25m bpd, up almost +10% in 12-months.

Compliance between OPEC and Non-OPEC members on agreed upon production cuts was over +90% in March.

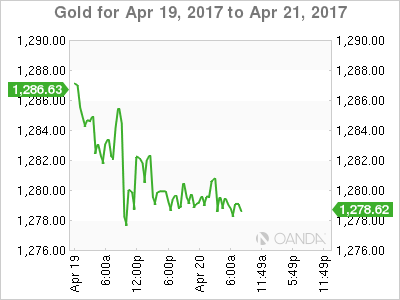

Gold prices are holding firm (unchanged at +$1,278.74 per ounce) ahead of the U.S open after falling as much as -1% yesterday, with tensions surrounding North Korea and the upcoming French presidential election driving safe-haven demand.

Yesterday, the yellow metals drop was its worst one-day fall in four-weeks.

3. Global yield curves remain flatter

The U.S 10-year Treasury yield has tumbled about -40 bps from its 2017 peak in March. Despite the plunge in yields, bond bears still expect U.S yields to back up towards that +3% handle by Q4. They don’t believe that the current patch of ‘softer’ U.S data is weak enough to throw the Fed off its game plan to normalize rates.

However, one risk for that higher yield call is for both far right and far left candidates in the French Presidential election to enter into the second round.

If the market gets its baseline scenario – Le Pen vs. Macron – in the second round on May 7, Le Pen is unlikely to significantly increase her support beyond her base, and voters of the moderate left and right are expected to merge around Macron. This scenario should be a plus for the EUR (€1.1000’ish) and have Bund yields unwinding the past months risk premium rather quickly.

The yield on U.S 10’s has slid -1 bps to +2.20% after a +5 bps advance Wednesday. Most other eurozone bond yields are little changed on the day.

4.’Big’ dollar remains under pressure

The USD remains soft against the G10 FX pairs that started with last Friday’s soft retail sales and CPI data from the U.S.

The EUR has rallied +0.5% to a three-week high atop of €1.0777, shrugging off political uncertainty before this weekend’s first-round French presidential elections. Election risk seems to be more evident in Scandinavian and central European currencies. The EUR is also being supported by the markets doubts about the global reflation trade.

GBP (£1.2836) remains supported by the view that early elections in the U.K diminishes prospects of a messy exit from the E.U – however, someone needs to tell that to the European side!

Elsewhere, the NZD (NZ$0.7036) is firmer after data overnight showed that New Zealand Q1 CPI annual reading remained within the target range for the second consecutive month and the highest level since Q3 2011.

5. German March PPI unchanged on month, +3.1% on year

Data this morning showed that German producer prices remained unchanged last month, while the annual rate stabilized at February’s level.

As expected, factory gate prices rose +3.1% in March y/y., while the annual rate matched the strongest annual rise in over five-years.

Note: Following the pattern of previous months, energy prices (+4.5% y/y) continue to have the biggest impact on the overall index.

Ex-energy prices, producer prices rose +0.3% on the month and increased by +2.6% on the year.