. This level prompted FX interventions to the tune of almost JPY 10tn by the Japanese Ministry of Finance at the end of April and alarm bells are ringing this time around as well. Vice Finance minister Kanda confirmed preparedness to take appropriate action in the event of excessive FX moves based on speculation.){kind=link}

Markets

The Japanese yen grabs most attention this morning. Dollar strength pushed USD/JPY last Friday above 159.50 following stronger-than-expected June PMI’s and the pair is still flirting with the 160 mark this morning (34-yr JPY low). This level prompted FX interventions to the tune of almost JPY 10tn by the Japanese Ministry of Finance at the end of April and alarm bells are ringing this time around as well. Vice Finance minister Kanda confirmed preparedness to take appropriate action in the event of excessive FX moves based on speculation. Excessive currency fluctuation negatively impact the national economy, he added. Finance Minister Suzuki later added weight by stressing that the government is watching FX moves closely. Minutes from the June Bank of Japan meeting fail to help the currency even as they bolster the case for a July rate hike: “if deemed appropriate, the central bank should raise the policy rate before it’s too late”. A small Japanese interest rate adjustment obviously doesn’t suffice against a hawkish leaning Fed keeping policy rates at their peak levels for longer.

Most recent French election polls continue pointing to a win for Marine Le Pen’s Rassemblement National in the first round of legislative elections next Sunday. They are forecast to get 35.5% of the vote, ahead of alliance of left-wing parties (Nouveau Front Populaire, 29%) and President Macron’s alliance (Ensemble, 21%). In the projected seat tally, they fail to get an outright majority though (210-250 guestimate in 577-seat parliament). Such hung parliament risks putting France in a political deadlock with RN (Bardella) so far ruling out delivering a PM for a minority government. Political uncertainty could thus remain high after elections with little momentum to put French ailing public finances back on track. The French 10-yr OAT-swapspread continues trading near recent multiyear highs (+45 bps) with French bonds unlikely to pull any comeback soon. The German/French 10-yr yield spread hit 80 bps for the first time since 2012. Euro weakness holds EUR/USD (just) below 1.07 this morning. The YTD low at 1.0601 remains the travel direction. Today’s eco calendar is thin with only German Ifo business climate which will normally reflect Friday’s weakness in PMI’s (political uncertainty). Speeches by ECB and Fed governors are a wildcard. This week’s eco agenda is back-loaded with the Fed’s preferred (May) PCE deflators and first national EMU (June) CPI data on Friday.

News & Views

The IMF in its annual review said that Hungary has come a long way reducing double digit inflation and bringing the current account deficit under control. It expects average annual inflation of 4.2% this year to ease to the 3% central bank target by 2026. But significant challenges remain with the fiscal deficit and debt ratio still well above the pre-pandemic levels. It also said that the windfall taxes introduced in 2022 are increasing market uncertainty and expressed criticism on the country’s “excessively high” and competition-hindering state ownership in key sectors. The IMF lashed out at the government’s interest rate freeze as well, as it distorts market conditions. The Hungarian government recently extended an interest rate cap on retail loans (introduced in Jan 2022) until the end of 2024. The IMF urged Hungary to pursue a credible and growth-friendly fiscal consolidation plan and said the government should help the central bank’s efforts to reduce inflation. The IMF lastly stressed that structural and governance reforms are necessary or risk losing access to the remaining locked up European funds, in turn leading to a higher risk premium, a weaker forint and tighter monetary policy weighing on growth.

China’s fiscal revenue fell 2.8% in the first five months of 2024 compared to the same period last year. It’s also an acceleration from the 2.7% drop in the January-April period and a sign of sluggish demand and the fragile property sector continuing to weigh on the economy. Expenditures rose 3.4% in the five months to May. The government pledged more fiscal stimulus to support the ailing economy and to reach the (ambitious) 5% growth target for this year. Part of the efforts include the recently kicked-off sale of CNY 1tn long-dated special treasury bonds to help fund mega projects in key sectors.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. For the time being, though, the political narrative (France) dominates. After hitting a new YtD top at 2.7%, the German 10-yr yield corrected lower on safe haven bids.

US 10y yield

The Fed is seeking more evidence than just one slower-than-expected (May) CPI is providing. Upgraded inflation forecasts and a higher neutral rate complicate the exact timing of a first cut further. June dots suggest one move in 2024 followed by four more next year. Markets are positioned more aggressively, turning the recent low in yields into a technical support zone. The US 10-y yield is testing the downside of the 4.2/4.7% trading range.

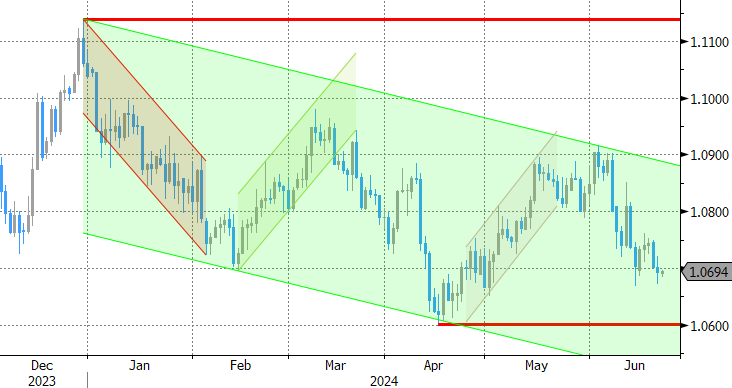

EUR/USD

EUR/USD is stuck in the 1.06-1.09 range. The desynchronized rate cut cycle with the ECB exceptionally taking the lead, strong US May payrolls and a swing to the right in European elections pulled the pair away from 1.09 resistance. The Fed meeting balanced the weaker than expected US CPI outcome. Euro fragility makes a return to the 1.06 downside more likely than not.

EUR/GBP

Debate at the BOE is focused at the timing of rate cuts. May headline inflation returned to 2%, but core measures weren’t in line with inflation sustainably returning to target any time soon. Still some BoE members at the June meeting appeared moving closer to a rate cut. This might cap further sterling gains. At the same time, the euro remains vulnerable to political event risk going into the French elections. EUR/GBP 0.84 is becoming solid support.