{kind=link}

- Core PCE inflation to test bets of two Fed rate cuts in 2024

- Yen awaits BoJ Summary of Opinions, Tokyo CPI

- Canadian CPI data also enters the spotlight

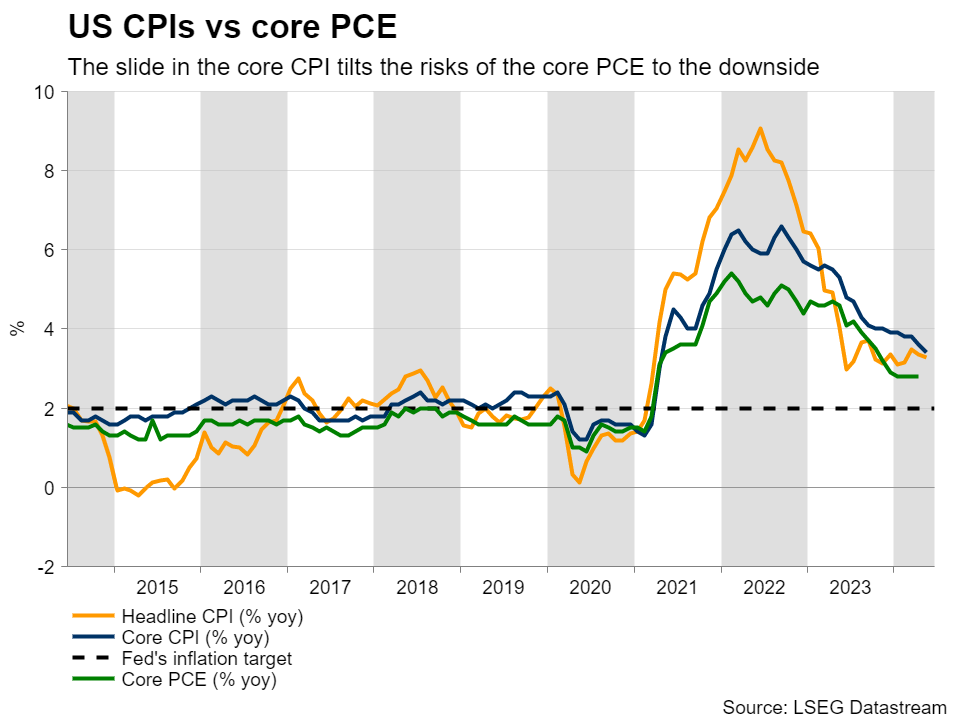

Will PCE data confirm Fed rate cut bets?

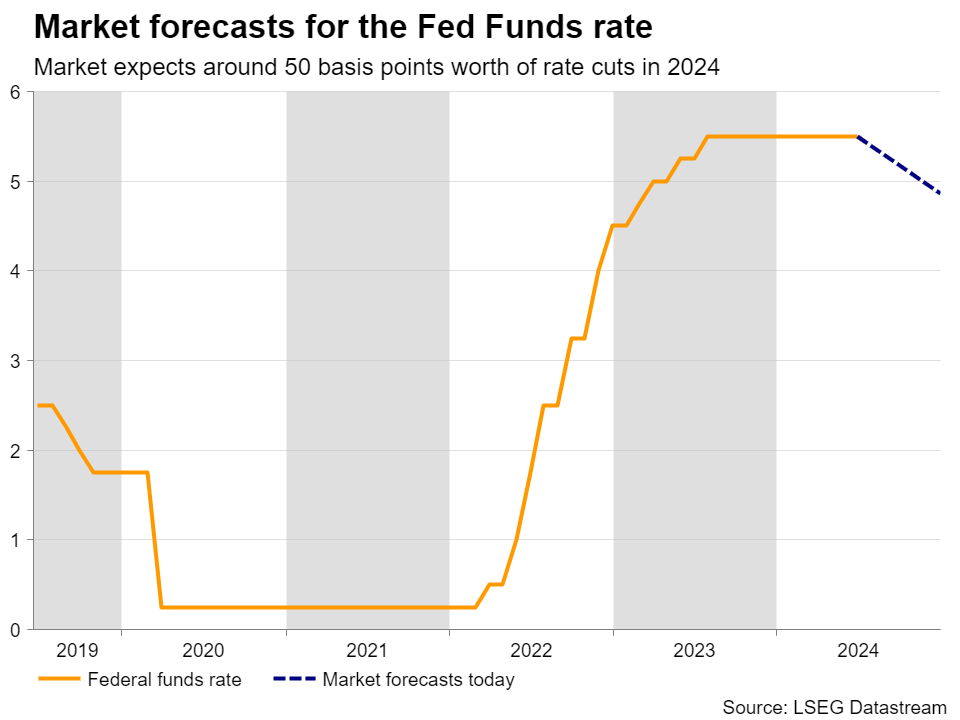

Although the Fed’s updated dot plot pointed to only one quarter-point reduction by the end of the year, the softer-than-expected CPI numbers a few hours ahead of last week’s decision did not convince market participants about officials’ intentions. The weaker-than-expected retail sales numbers this week corroborated that view.

Indeed, according to Fed funds futures, investors are penciling in around 50bps worth of reductions by the end of the year, assigning around a 70% probability for the first cut to be delivered in September.

With all that in mind, the main item on dollar traders’ agenda next week may be the core PCE price index for May due out on Friday, which is accompanied by the personal income and spending data for the same month. The final GDP print for Q1 is also set to be released the day before, but given that Q2 is almost over, any minor deviations from the 2nd estimate are likely to pass unnoticed.

As for the core PCE index, the slide in the core CPI for the month poses some downside risks. There may be downside risks to spending as well, derived by the weakness in retail sales, although income may be poised to improve, something suggested by the better-than-expected average hourly earnings.

Overall, another set of economic data pointing to cooling consumer demand may further solidify expectations of two quarter-point cuts by the Fed, and perhaps increase the probability for initiating the process in September. This could prove negative for the US dollar, especially against its Australian counterpart. Remember that this week, the RBA maintained its neutral stance, while Governor Bullock revealed that they discussed the option of raising rates.

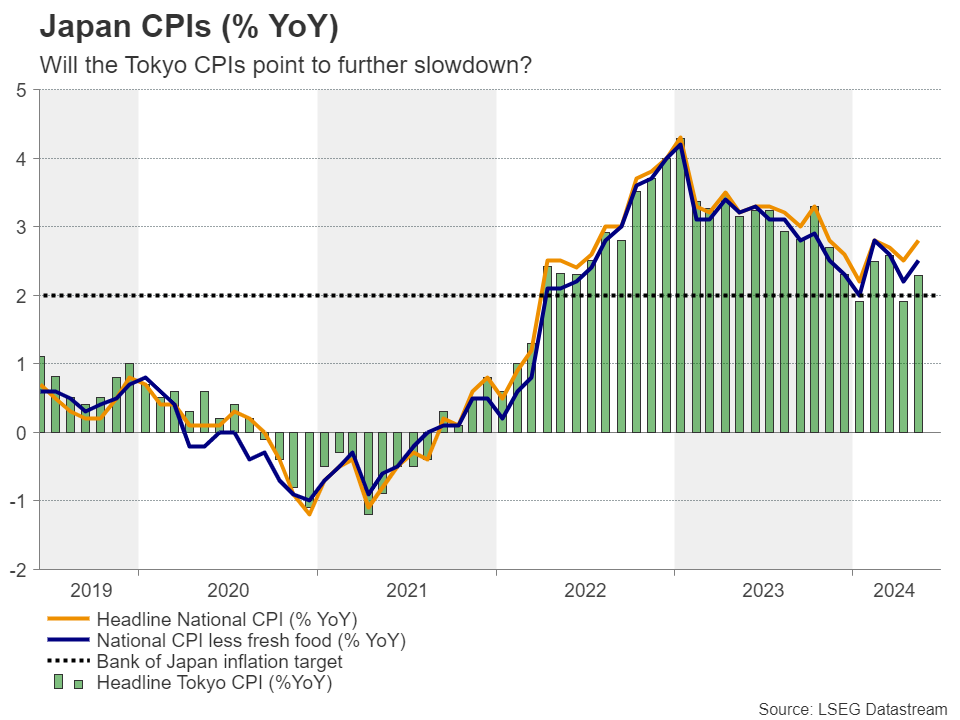

How likely is a July hike by the BoJ?

In Japan, the Summary of Opinions from last week’s BoJ decision will be released on Monday during the Asian session, while on Friday, the Tokyo CPIs for June are coming out.

At last week’s meeting, BoJ officials decided to keep interest rates unchanged and said that they would start trimming their bond purchases, but that they will announce a detailed plan next month. What’s more, Governor Ueda said that he is not ruling out interest rates rising in July.

Still, the yen fell, perhaps as some market participants were expecting more concrete signals about a July hike and a potential slowdown in bond purchases. This is also evident by market pricing, where the probability of a 10bps hike in July has dropped significantly, to around 27%. Ahead of the decision that chance was more than 65%.

All this suggests that yen traders will dig into the summary for clearer hints on how likely a July hike is. If they are left once again disappointed, the yen is likely to extend its slide and perhaps take another hit if the Tokyo CPIs pull back below the Bank’s 2% objective again. Having said all that though, with dollar/yen already trading near the 159.00 zone, further advances, closer to the round number of 160.00, may significantly increase the risk for another intervention episode by Japanese authorities, although officials have been silent until now.

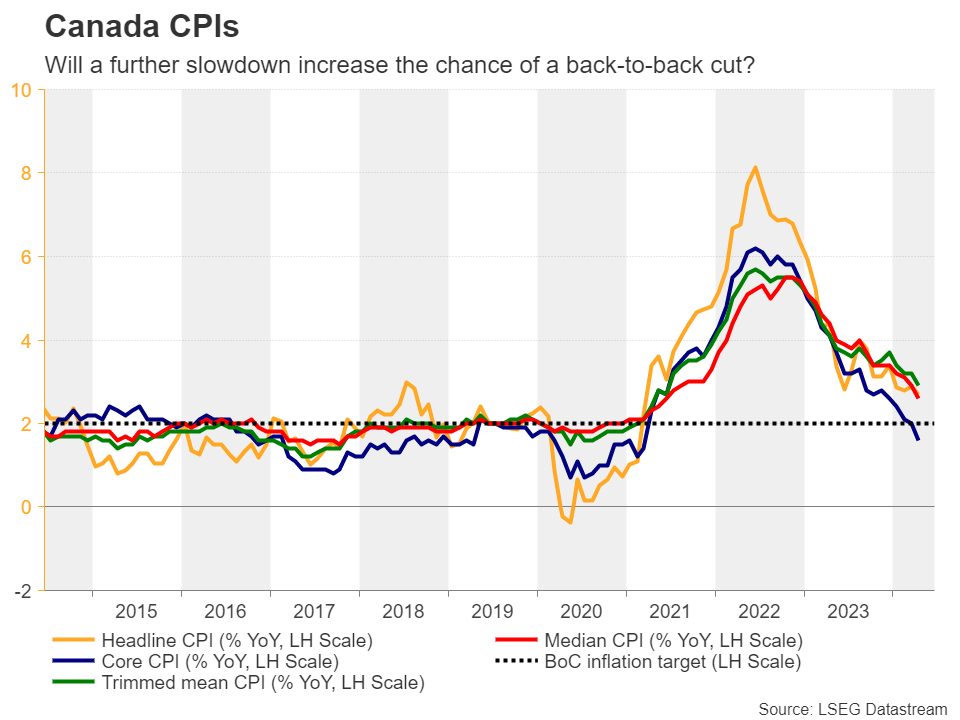

Back-to-back rate cuts for the BoC?

Canada’s CPI numbers are also on next week’s agenda. They are due out on Tuesday. Earlier this month, the BoC became the second central bank in the G10 group to cut interest rates by 25bps, with Governor Macklem signaling that it would be “reasonable to expect further cuts” if inflation continues to cool.

Since then, the only data set worth mentioning was the employment report for May, which came in slightly better than expected. And that was not enough to deter investors from expecting another rate reduction in July. The probability of such a move currently rests at around 62% and should next week’s data reveal that inflation continued its downward trajectory, it could go higher. This could weigh on the Canadian dollar.

Australia releases its monthly CPI prints for May. Inflation in Australia has been proving stickier than other major economies, with RBA policymakers discussing the possibility of hiking rates at Tuesday’s gathering. Ergo, if the CPI confirms the stickiness in price pressures, traders will continue seeing the RBA as more hawkish than other major central banks, something that may keep the aussie supported.