{kind=link}

Markets

US data on Friday (almost) perfectly fitted the dovish post-Fed market momentum. After several consensus-beating monthly releases, the US economy in April ‘only’ added 175k jobs, the slowest growth in six months. US wage growth also eased with Average Hourly Earnings (AHE) slowing to 0.2% M/M and 3.9% Y/Y (from 0.3% M/M and 4.1% Y/Y). The unemployment rate rose from 3.8% to 3.9%. A bit later in the session, the US services ISM copied the setback seen in the manufacturing measure earlier last week. The headline services ISM unexpectedly dropped in contraction territory (49.4 from 51.4). The new orders component slowed further to 52.2 (from 54.4). Employment also slipped further into contraction territory (from 48.5 to 45.9). Other sub-indices were more mixed but there was one big exception to the overall soft narrative: the prices paid index jumped to 59.2 from 53.4. One set of monthly data for sure isn’t enough to conclude the US economy is heading to stagflation, but it’s something to keep an eye on as it might complicate the Fed’s room of maneuver. In a first reaction, markets clearly saw the data reaffirming the potential for the Fed to cut rate later this year. US yields corrected further off the YTD highs reached end April or earlier last week, declining between 7.4 bps (10-y) and 5.7 bps (2-y). Interestingly, the 2-y yield intraday tested the 4.7% area (level traded just before the release of the higher than expected US CPI early April), but closed well above that. Investors now again see a 90% chance of a first rate cut in September and 80% a second 25 bps step in December. German yields showed similar declines easing between 6.6 bps (2-y) and 2.6 bps (30-y). Despite ongoing high inflation readings, equity markets were happy to further bet on an easing of financial conditions with US indices rebounding up to 2.0% (Nasdaq). The dollar initially lost substantial ground but in the end losses were modest (EUR/USD close 1.0761; DXY 105.03 from 105.30). Japanese authorities also got some further breathing space. USD/JPY closed at 153.05, compared to a brief journey above 160 early last week.

Today’s eco calendar is thin. Japanese and UK markets are closed and there are no important data in the US. Later this week, we keep an eye at the US Treasury refinancing (combined sale of $125 bln of 3-y, 10-y and 30-y Notes) and Fed governors given their view on recent data. For US yields, we expect some consolidation off recent peak levels. Stick inflation probably will limit any sustained further decline in yields especially at the long end of the curve. The short-term technical picture for the dollar also turned more neutral. Still we see room for some bottoming. The EUR/USD 1.08 area probably won’t be that easy to regain in a sustainable way.

News & Views

The OECD in a new biennial economic survey released today zoomed in on New Zealand this time. It said the country has limited scope to cut rates in 2024 amid inflation that’s likely to be persistent. The OECD advised to keep rates constant at 5.5% until “there is clear evidence that inflation will fall to the middle of the RBNZ’s target range”. Prices in the first quarter of the year rose by 4%, above the 1-3% range. A domestic gauge even came in at 5.8% with the OECD noting that high migration has pushed up domestic demand higher than the central bank (RBNZ) had expected. It also pressed the government to get spending under control and reduce the deficit. Finance minister Willis in March said the aim for a surplus was 2028, a year later than previously projected because of weaker economic growth. The OECD forecasts a 0.8% expansion in 2024 before picking up to 1.9% next year.

Chicago Fed president Goolsbee argued the FOMC’s dot plot needs more context than the current form provides. Right now, “the dot plot is just a collection of opinions without economic content.” Goolsbee noted that a policymaker adding or removing cuts for this year does not inform whether the participant believes the economy is overheating or that it simply “has the capacity to grow faster and therefore can tolerate higher rates.” His solution would be a matrix that matches the economic forecasts to the rate path for each FOMC participant. Goolsbee’s comments come amid a general rethink of central bank communication in the wake of the huge forecasting errors made in recent years. Former Fed governor Bernanke recently concluded an exercise for the Bank of England while ECB’s Schnabel floated the idea of publishing an ECB dot plot. The Fed prepares a review of its own policy framework, expected to begin later this year..

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a summer (June) rate cut and has broad backing. EMU disinflation will continue in April and bring headline CPI (temporarily) at/below the 2% target. Together with weak growth momentum, this gives backing to deliver a first 25 bps rate cut. A more bumpy inflation path in H2 2024 and the Fed’s higher for longer strategy make follow-up moves difficult. Markets have come to terms with that.

US 10y yield

The Fed in May acknowledged the lack of progress towards the 2% inflation objective, but Fed’s Powell left the door open for rate cuts later this year. Soft US ISM’s and weaker than expected payrolls supported markets’ hope on a first cut post summer, triggering a correction off YTD peak levels. Sticky inflation suggests any rate cut will be a tough balancing act. 4.37% (38% retracement Dec/April) already might prove strong support for the US 10-y yield.

EUR/USD

Economic divergence, a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead and higher than expected US CPI data pushed EUR/USD to the 1.06 area. From there, better EMU data gave the euro some breathing space. The dollar lost further momentum on softer than expected early May US data. Some further consolidation in the 1.07/1.09 are might be on the cards short-term.

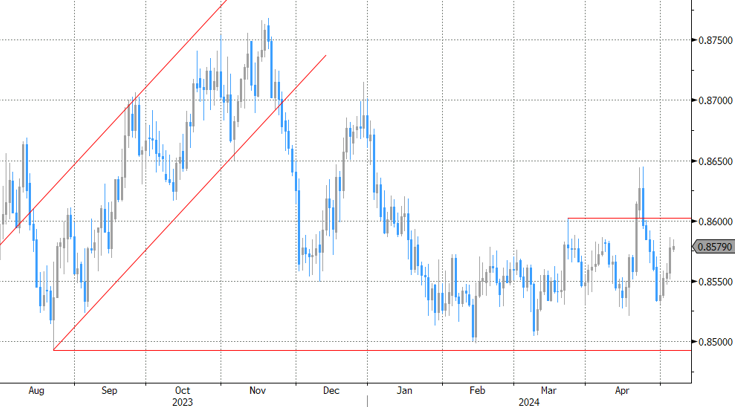

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Most BoE members align with the ECB rather than with Fed view, suggesting that the disinflation process provides a window of opportunity to make policy less restrictive (in the near term). Sterling’s downside turned more vulnerable with the topside of the sideways EUR/GBP 0.8493 – 0.8768 trading range serving as the first real technical reference.