{kind=link}

Markets

Yields this morning cautiously continued the downtrend after Powell’s rather mild assessment at the press conference on Wednesday. The Fed chair indicated that, despite disinflation making little progress of late, keeping the policy rate a while longer at current level will likely still suffice to return inflation to target over time. An unexpected and substantial deterioration of labour market conditions even could cause the Fed to ease policy pre-emptively. Today’s payrolls were a first high profile reality check. Whether it will be enough for Fed governors to already ignore strong activity data and higher than expected inflation over the previous months still has to be seen, but the April payrolls were weaker across the board. The US economy last month ‘only’ added 175k jobs versus 240k expected, the slowest gain in six months. There were no really big negative outliers in the major subcategories, but no or limited job growth in temporary help (-16k), leisure and hospitality (+5 k) or government (8k) did catch to eye. Also the household survey was soft with limited reported job growth and the unemployment rate rising from 3.8% to 3.9% amid an unchanged participation rate (62.7%). Average hourly earnings eased to 0.2% M/M and 3.9% (from 0.3% M/M and 4.1%). Interest rate markets understandably continued on the post-FOMC momentum. US yields decline between 9 bps (5-y) and 6 bps (30-y). Money markets again see a first rate cut as early as the September meeting with a second step almost full discounted again for December. Before Wednesday’s Fed communication, investors only saw a 75% chance of a first rate in November. German yields are essentially following the trend in the US easing between 6.5 bps (2-y) and 3 bps (30-y) as the Fed rate path remains a important variable for almost other central banks, including the ECB. The easing on the interesting rate markets triggers a broad equity rebound. The EuroStoxx 50 gains 0.9%. US indices open up to 1.75% higher (Nasdaq). Oil still struggles to avoid further losses (Brent $ 84 p/b). Golds also fails to profit from lower yields and/or a weaker dollar ($ 2302 p/oz). On FX, the post-Fed USD correction builds with the DXY trade weighted index tumbling below 105 (104.8). EUR/USD briefly tested the 1.0807 level (38% retracement decline end Dec/mid-April) (currently 1.079). The broader USD decline also provides some relief for the BOJ with USD/JPY trading at 152.5, to be compared with ‘intervention levels’ north of 160 touched earlier this week. Sterling slightly underperforms the euro as markets look forward top next week’s BoE policy meeting (EUR/GBP 0.857).

After finishing this report, the US services ISM will still be published. However, we would be surprised that even a strong report would be able to reverse the post-payrolls’ market dynamics.

News & Views

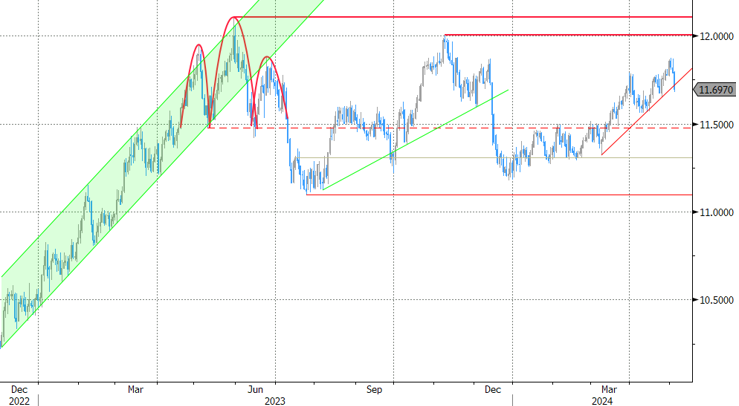

The Norges Bank (NB) today as expected left its policy rate unchanged at 4.50%. The MPC assesses that the policy rate is sufficiently high to return inflation to target within a reasonable time horizon, but it will likely be kept at current level from some time ahead. At 3.9% Y/Y for headline inflation and 4.5% for the core CPI-ATE measure (ex-energy and taxes), inflation holds well above the 2.0% target, but has been slightly lower than projected. At the same time, economic activity is slightly better than expected and wage growth may turn out to be slightly higher than projected, too. The NB also keeps close eye at external developments. Market policy rate expectations have risen internationally as did Norwegian policy rate expectations. The US dollar has appreciated broadly and the krone exchange rate is weaker than assumed. The NB will have more information at its policy meeting in June, when new forecasts will be presented. In March, the NB indicated that the policy rate could stay at current level till autumn before gradually moving down. Data so far suggest that a tight monetary policy stance may be needed for somewhat longer than previously envisaged. The Norwegian krone was captured in a protracted weakening trend since the start of the year, but outperforms today. EUR/NOK eased from the 11.80 area to currently trade at 11.69. Admittedly, the NOK rebound this afternoon also was helped by the broader post-payrolls USD correction.

Graphs

EUR/NOK: Norwegian krone rebounds as weak currency gets bigger weight in the NB’s policy assessment.

Dollar extends correction. EUR/USD tests 38 % retracement of Dec/April decline (1.0807).

US 2-y yield ‘nosedives’ off 5.0% barrier as market again contemplates September rate cut.

Nasdaq tries to escape sell-on-upticks dynamics as global financial conditions ease.