{kind=link}

- Japan allegedly intervened for the first time in six months

- Most recent interventions did not produce concrete results

- A more hawkish BoJ is probably needed for a sustained yen rally

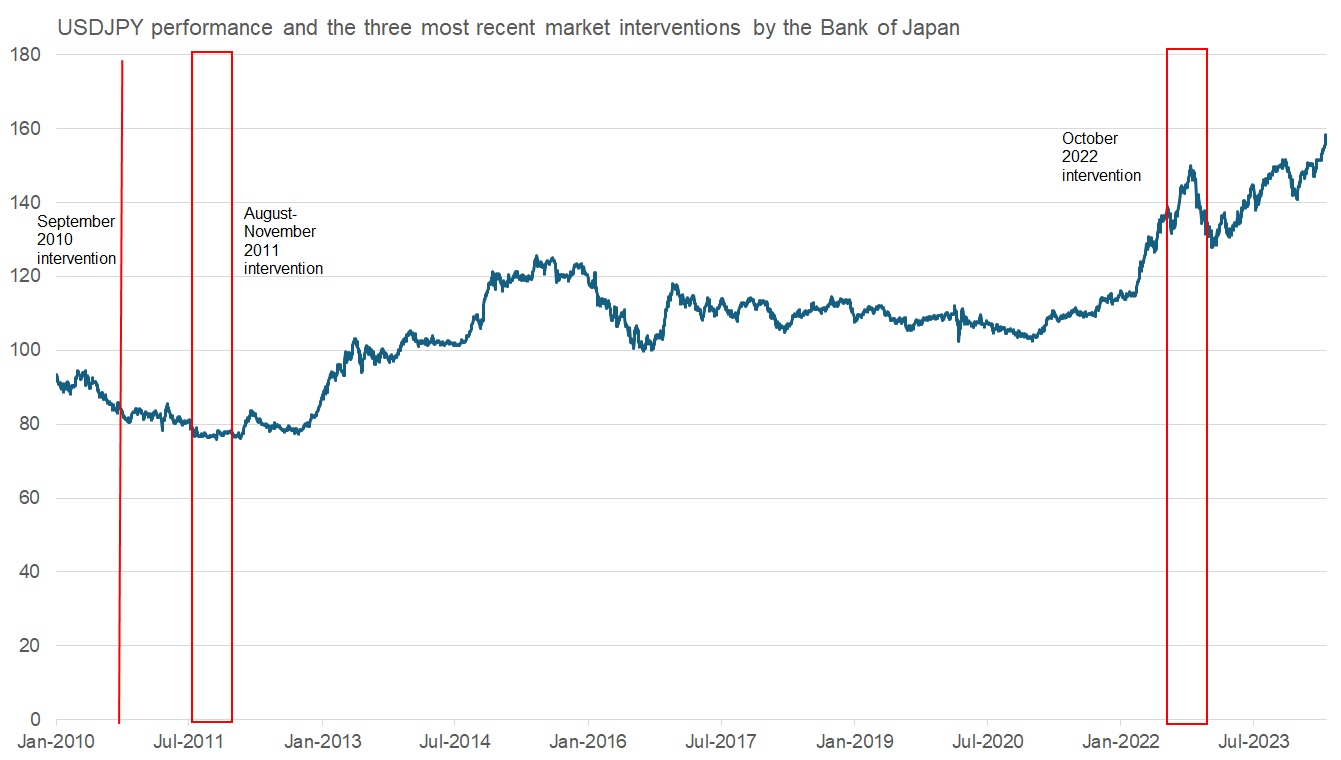

Japan has a long history of market interventions, to weaken or prop up its currency. Several times since the 1990s, Japan, unilaterally or with help from its main trading partners, tried to turn the tide for the yen. A quick look at the most recent market interventions, including yen’s post-intervention performance, could offer valuable insight to what can be expected in the short-term for the yen after Monday’s activity.

Before delving into the analysis, it is important to explain how Japan intervenes. The Japanese finance ministry is responsible for such a move. It then instructs the BoJ, due to its established links with the main banks and investment houses, to buy/sell the yen.

The US dollar/yen pair appears to be the decisive factor in Japan’s reaction function. If the yen is deemed to be very expensive against the dollar and not reflecting the underlying economic disparities, then the BoJ sells yen (buys dollar) in the market aiming to weaken its currency. Alternatively, when the yen is deemed to be too weak against the dollar, the BoJ buys yen (sells dollars) in the market.

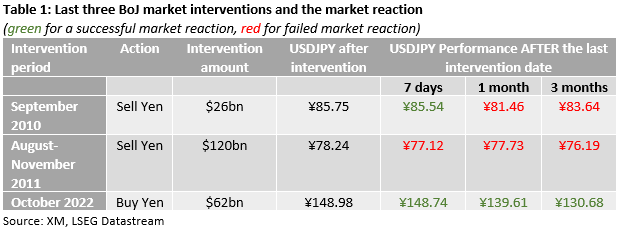

The three most recent market interventions in 2010, 2011 and 2022 respectively were analysed; table 1 below presents some key findings.

September 2010 – first unilateral intervention since the 2003-2004 programme

Almost six years after the massive 2003-2004 program that lasted for more than 15 months, Japan decided that the consistent yen appreciation was a hindrance to its effort to return to solid growth. Since mid-2007 and mostly due to the US subprime crisis and the subsequent quantitative easing programme (QE1) implemented by the Fed, the yen appreciated aggressively against the dollar. From hovering around the ¥120 area, dollar/yen dropped below ¥90 during the first half of 2010.

The BoJ intervened once on September 15, 2010 spending around $26bn to weaken the yen. It stopped short from intervening again as a different approach was chosen. A QE programme was announced by the BoJ in early October 2010 with the visible target being not only to create inflationary pressures but also to cause a sizeable yen weakness.

August-November 2011 – More aggressive approach

With the September/October 2010 effort proving insufficient and a coordinated one-off intervention in March 2011 not producing the expected results, the BoJ was once again forced to return to the market. In the August-November 2011 period, the BoJ sold the yen six times and expanded again its QE program. The intervention notched up a gear in early November 2011 with the total amount spent reaching $120bn.

Similar to the 2010 episode, the yen did not significantly underperform. Dollar/yen continued to hover around the ¥80 mark until 2013 when Abenomics and another massive QE programme in the US (QE3) pushed this pair close to the ¥100 level.

October 2022 – Yen reaches multi-decade low against the dollar

Almost 11 years after the last intervention and the yen was significantly underperforming against the dollar. Despite the revived BoJ under new Governor Ueda, developments elsewhere, and in particularly the aggressive Fed tightening cycle to control runaway inflation, drove the dollar/yen pair to reach a new 32-year high.

Three daily interventions in the period of one month totaling $62bn were implemented with dollar/yen correcting aggressively. However, the main reason for this move was the change in expectations for next Fed rate rises and the associated drop in US Treasury yields. In addition, another stimulus package from the Japanese government and the December BoJ yield curve control tweak also contributed to the renewed yen strength.

Putting everything together and two conclusions could be reached: (1) market interventions as a stand-alone reaction have proven to be an insufficient measure. Only a combination of domestic and foreign developments could sustainably change the direction of the yen. Having said that market intervention has its remits as it could simply be seen as a very short-term move to stop the consistent strengthening/weaknening of the yen until other forces come to play.

And (2) the BoJ tends to intervene multiple times, unless there is another plan in the works like the various QE programmes seen in 2010 and 2011. Such an outcome looks unlikely at the current juncture though.

Moving to the current situation and the yen is not expected to stage a sustainable rally against the dollar, most likely forcing the BoJ to intervene again in the market in low liquidity sessions. Unless the Fed surprises with dovishness in the near future and a rate cut follows at the June meeting, the BoJ will need to adopt a much more hawkish monetary policy stance in order to stabilize the yen.