{kind=link}

Global equity indexes have continued their rally that started the week on renewed confidence in Eurozone stability and strong earnings data expectations. This newfound confidence has global yields backing up and the ‘big’ dollar in demand for a third consecutive day.

President Trump is expected to unveil his tax plan tomorrow that would cut the upper corporate rate to +15%. If he is short on detail and lacks substance, this market will quickly reverse course.

Other risks remain as investors await central bank meetings tomorrow from the BoJ and ECB. Tensions around North Korea continue to simmer, while in China, concerns of a crackdown from regulators have left the world’s second-largest equity market trading atop its 2017 low.

1. Asian stocks near two-year high on U.S optimism, Europe mixed

Asian stocks extended their gains for a fifth consecutive day overnight, as renewed optimism about the U.S economy has brightened the outlook for risky assets.

In Japan, the Nikkei share average closed at a one-month high, lifted by a weaker yen (¥111.17) and a record high for the Nasdaq Composite. The index is up +3.6% for the week, and climbed +2% last month. The broader Topix index rose +1.2%, climbing for a fifth straight session for the longest winning streak this year.

Australia’s S&P/ASX 200 Index added +0.7% and New Zealand’s S&P/NZX 50 Index increased +1.6%, the most in six-months, as both markets reopened after ANZAC day.

In China, the Shanghai Composite Index added +0.2% after climbing a similar amount yesterday.

In Europe, equity indices are trading mixed as market participants await President Trump’s tax reform plans. Banking stocks are generally lower across the board adding to losses on the Eurostoxx, while commodity and mining stocks are trading mixed in the FTSE 100.

U.S stocks are set to open small down (-0.1%).

Indices: Stoxx50 -0.2% at 3,577, FTSE flat at 7,277, DAX flat at 12,465, CAC-40 +0.1% at 5,280, IBEX-35 -0.2% at 10,758, FTSE MIB -0.6% at 20,687, SMI +0.2% at 8,793, S&P 500 Futures -0.1%.

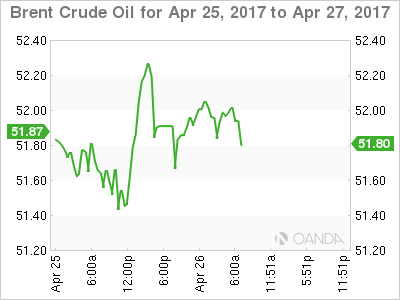

2. Oil price slips on bulging U.S stocks, ample global supplies

Oil prices have weakened further overnight as yesterday’s U.S inventory data showed a rise in crude stocks. Coupled with record supplies in the rest of the world is casting further doubt over OPEC’s ability to control output and tighten the market.

Brent crude futures have eased -3c to +$52.07 per barrel, down around -8.5% below this months peak. U.S West Texas Intermediate (WTI) is trading down -4c at +$49.52 per barrel, after gaining +0.7% in yesterday’s session. The WTI price has fallen for seven of the past eight sessions.

API inventory data, issued late Tuesday, is weighing on prices. Not only did the report show crude oil stocks rising +897k barrels in the week to April 21 (vs. an expected drawdown of -1.71m barrels), but it also showed a large build in gasoline stocks, unusual for this time of the year.

Should these figures be mirrored by today’s EIA report (10:30 am EST), expect the weaker bulls to offload some of their long contract positions.

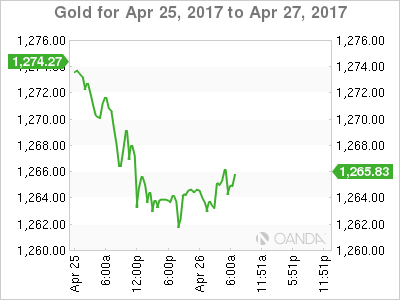

Ahead of the U.S open, gold prices have dipped to a new two-week low (-0.2% to +$1,261.36 per ounce) as increased investor appetite for ‘risk’ has dulled the demand for safe-haven assets. The current rally in ‘real’ interest rates should see the yellow metal come under further short-term pressure.

3. Global yields back up on Trump expectations

Across the curve, gains in U.S interest rates are expected if the Trump’s tax plan includes reductions on repatriated earnings. Investors can expect the short end to harden the quickest, more in anticipation of corporate treasuries’ divestment of short product ahead of any repatriation.

Yesterday’s U.S Treasury bill auction results: +$60B four-week bill auction draw was +0.735%, bid-to-cover was 3.32; +$20B 52-week bills draw was 1.060%, BTC 3.23 – four-week +21.8% allotted at the high – 52-week +7.2% allotted at the high.

The yield on U.S 10’s is little changed at +2.33%, after climbing for five straight sessions.

Elsewhere, Aussie 10-year debt saw yields back up +3 bps to +2.63%, French 10-year yields have fallen -1 bps to +0.90%, after advancing +7 bps yesterday.

Note: The bearish sentiment in 10-year German Bunds is not expected to subside until yields rise above +0.4%. Fears of reduced ECB accommodation are still at play. Bund yields have surged from a low of +0.156% before the French vote last week to +0.385%.

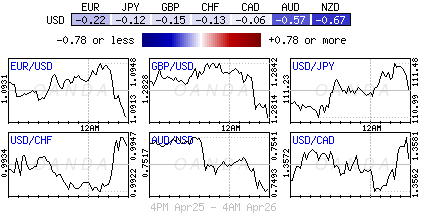

4. Dollar partially in vogue

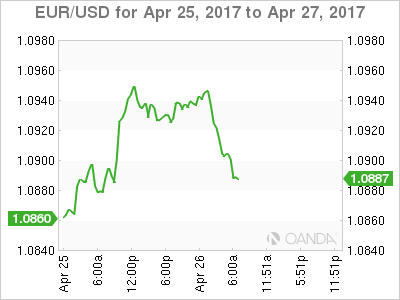

The USD is a tad firmer heading into the U.S open. The markets focus now turns to the details on the Trump administration’s tax reform plan.

The demand for dollars got a boost late yesterday as reports indicated that Trump would provide an incentive to repatriate accumulated foreign profits for U.S companies.

The EUR (€1.0900) outright did manage to print a fresh six-month high overnight at €1.0950, mostly aided by receding concerns about the risks posed by the French presidential election. The ECB sets its monetary policy tomorrow. With officials indicating little chance of a policy change, the focus will be on any signals from President Mario Draghi that the ECB is starting to discuss an exit from its extraordinary stimulus.

USD/JPY has continued its winning streak, as the yen has slipped -0.3% to ¥111.45, after dropping -1.2% yesterday. The currency is down -2.7% from a five-month high reached last week. The BoJ is expected to keep the settings on its monetary easing program unchanged at the end of a two-day policy meeting tonight.

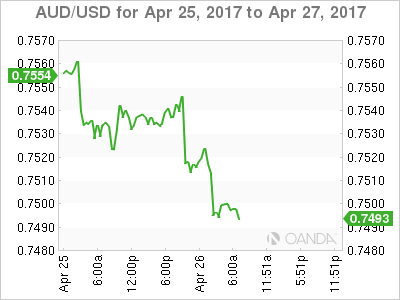

5. Australia CPI returns to RBA target range

The AUD (A$0.7497) was volatile in the overnight session following the mixed Q1 CPI data. The headline year-on-year moved back into the RBA’s +2-3% target range for the first time in two-years, however, it missed expectations.

Q1 CPI – Q/Q: +0.5% vs. +0.6%e; Y/Y: +2.1% (highest since Q2 of 2014) vs. +2.2%e.

Analysts noted that much of the price increase was in auto fuel and housing, which may suggest that living costs are outpacing wage gains. Consensus does not expect an RBA rate cuts after the data, but believe that when CPI is consistently above +2% Aussie policy makers would signal a policy shift.