Live Comments

Oil Surges Toward $110 as Trump-Xi Summit Signals Supply Rerouting, Not Hormuz Resolution

The Trump-Xi summit was supposed to calm oil markets. Instead, it may have convinced traders that the global energy system is adapting to a prolonged Hormuz disruption rather than preparing for its resolution.

Brent crude surged toward $110 today after traders reassessed the implications of comments made by US President Donald Trump following his two-day meeting with Chinese President Xi Jinping in Beijing. Rather than signaling coordinated pressure on Iran to fully reopen the Strait of Hormuz, Trump emphasized plans for significantly expanded Chinese purchases of American oil exports.

“They’ve agreed they want to buy oil from the United States,” Trump said in an interview with Fox News. “We’re going to start sending Chinese ships to Texas and to Louisiana and to Alaska.”

That message appears to have fundamentally altered market psychology.

Before the summit, many investors had hoped Beijing would use its leverage as the largest buyer of Iranian oil to pressure Tehran into ending shipping disruptions and reducing tensions in the Gulf. A credible Hormuz reopening would likely have triggered a sharp collapse in crude prices by removing much of the war premium embedded in energy markets.

But instead of hearing a pathway toward reopening the Strait, markets increasingly heard something very different: a rerouting of global supply chains around a continuing disruption.

That distinction matters enormously.

If China increasingly replaces Iranian barrels with American energy supplies, Beijing may have less strategic incentive to defend Iranian export infrastructure or oppose more aggressive US actions against Tehran. Some traders interpret the summit outcome as raising — not lowering — the probability of future military escalation.

As a result, oil markets are beginning to shift toward pricing a more structural fragmentation of global energy trade flows. The summit did not solve the war. It may simply have reorganized the winners and losers. That helps explain why oil prices are accelerating higher rather than retreating despite two days of high-level diplomacy.

Technically, as Brent crude's rise from 96.03 resumed through 108.45 resistance today, the key focus is on 61.8% projection of 96.03 to 108.45 from 103.88 at 111.56. Firm break there could prompt upside acceleration to 100% projection at 116.30.

More importantly, any upward acceleration through 115.30 resistance the first indication that whole converging triangle pattern from 119.50 high made in March has completed. That could set up long term up trend resumption through the key 120 psychological barrier.

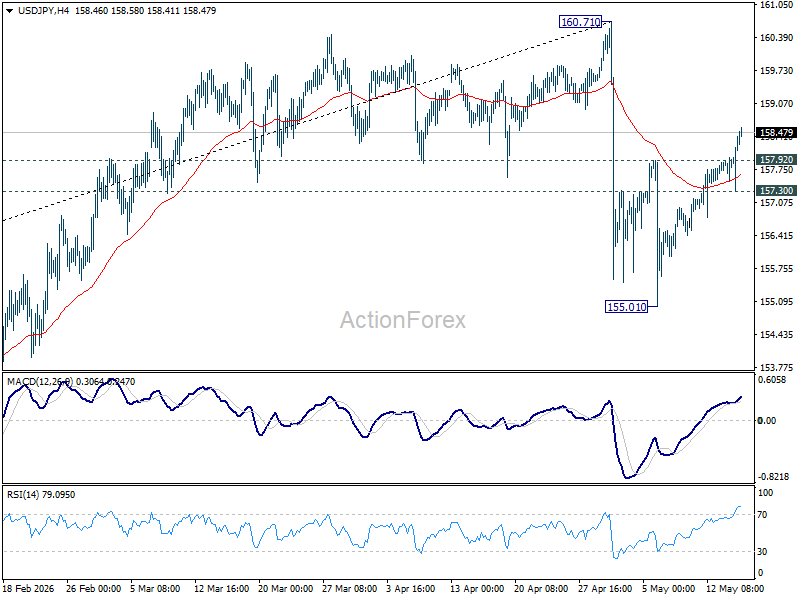

USD/JPY Climbs Toward 160 as Rising US Yields Test Japan’s Intervention Resolve Again

USD/JPY is once again approaching territory that could force Japanese authorities into difficult decisions. The pair surged through 158 on Friday as broad Dollar strength combined with another sharp rise in US Treasury yields. The US 10-year yield pushed above 4.5% in Asian trading, extending a global bond selloff that is currently dominating currency market dynamics. The latest move places USD/JPY back within striking distance of the psychologically and politically sensitive 160 level that previously triggered Japanese intervention.

The immediate driver is the widening yield gap between the US and Japan. Bond investors in U.S appears to be beginning to price a more hawkish policy environment under incoming Fed Chair Kevin Warsh, even while current Fed officials continue advocating a wait-and-see approach. Strong US inflation data this week, combined with resilient retail sales and stable employment conditions, reinforced fears that inflation linked to the Middle East energy shock could become more persistent, pushing Treasury yields sharply higher.

Importantly, however, markets are still only cautiously pricing additional Fed tightening. Current futures pricing implies roughly a 40% chance of one further rate hike by year-end. But in FX markets, even a modest repricing becomes highly significant when combined with Japan’s still-ultra-low interest rate structure and the BoJ’s cautious normalization path.

Meanwhile, Japanese officials are signaling concern about the broader global backdrop rather than simply Yen weakness itself. Finance Minister Satsuki Katayama said on Friday that G7 finance leaders are likely to discuss the recent surge in global bond yields. “These moves appear to be reinforcing each other across the major markets,” she said, referring to simultaneous selloffs in US Treasuries, Japanese government bonds, and UK gilts.

Her comments highlight an increasingly uncomfortable reality for Tokyo: intervention becomes far less effective when global bond markets are simultaneously widening the underlying yield differential supporting Dollar strength. Even if Japanese authorities step into FX markets again, it is uncertain whether intervention alone can sustainably reverse USD/JPY higher while US yields continue climbing faster than Japanese yields.

Technically, USD/JPY's break of 157.92 resistance suggests that pullback from 160.71 has already completed at 155.01. Rebound from there is now seen as the second leg of a corrective pattern from 160.71. Further rise could be seen towards 160.71 but strong resistance should emerge around there to bring reversal. Meanwhile, break of 157.30 minor support will argue that the third leg could have already started back towards 155.01.

Japan PPI Surges 4.9% as Energy Shock Intensifies

Japan’s wholesale inflation accelerated sharply in April, adding to expectations that the Bank of Japan could move toward another rate hike as early as June. The Corporate Goods Price Index rose 4.9% yoy, accelerating from 2.9% yoy in March and far exceeding market expectations of 3.0% yoy. It marked the fastest annual increase since May 2023.

On a monthly basis, producer prices climbed 2.3% mom after rising 1.0% mom previously, highlighting the growing impact of higher energy and import costs on Japan’s heavily import-dependent economy.

Petroleum and coal product prices rose 5.3% yoy, while chemical goods prices surged 9.2% yoy, the fastest pace since September 2022, reflecting broadening cost pressures linked to the Middle East conflict and disruption surrounding the Strait of Hormuz.

The weak Yen is also amplifying imported inflation pressures. Japan’s yen-based import price index surged 17.5% yoy in April, the fastest rise since December 2022.

| Indicator | March 2026 | April 2026 | Notes |

|---|---|---|---|

| Japan CGPI / PPI (YoY) | 2.9% | 4.9% | Fastest since May 2023 |

| Japan CGPI / PPI (MoM) | 1.0% | 2.3% | Sharp acceleration |

| Yen-Based Import Price Index (YoY) | 17.5% | Fastest since Dec 2022 | |

| Petroleum & Coal Goods Prices (YoY) | 5.3% | Reflecting higher crude and jet fuel costs | |

| Chemical Goods Prices (YoY) | 9.2% | Fastest since Sep 2022 |