{kind=link}

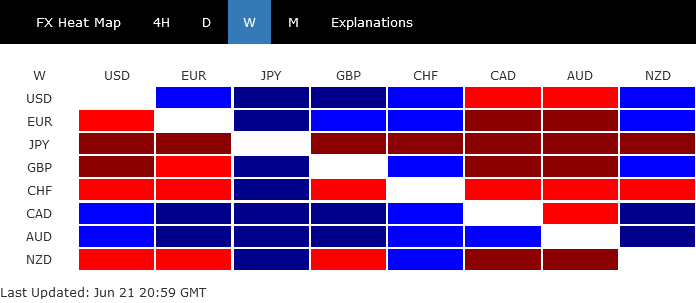

Yen ended as the runaway loser last week as its decline reaccelerated towards the end. With the crucial 160 level against Dollar now within reach, market participants are keenly watching to see if Japan will intervene soon to prop up the Yen, or just let it depreciate further.

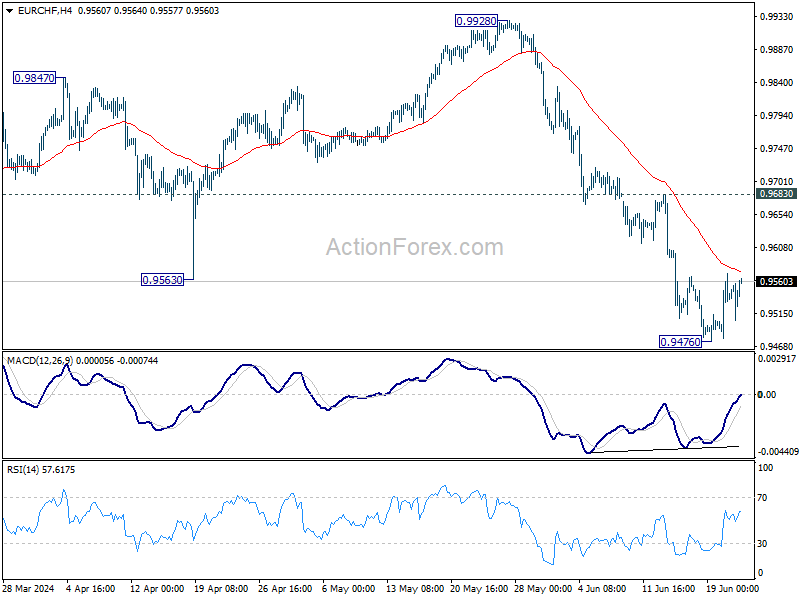

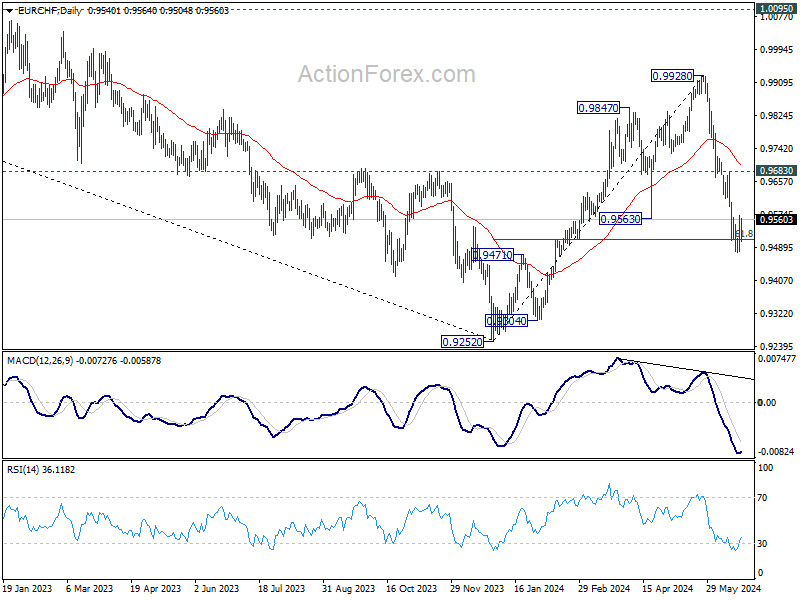

Swiss Franc was the second weakest currency by a mile, declining following SNB’s rate cut. Despite this, the Franc’s decline is at worst seen as consolidation of its strong gains earlier this month, with no indications of a reversal in trend.

While Euro did recover some ground against the Franc, it remains susceptible to further declines due to ongoing political instability in the European Union. British Pound is also facing vulnerabilities after BoE suggested that a rate cut is still on the table for August. Both Euro and the Pound ended the week in the middle of the performance spectrum.

Conversely, Australian Dollar was the standout performer, buoyed by RBA’s stance that keeps the possibility of another rate hike open. Canadian Dollar followed closely as the second strongest currency, while Dollar also saw gains, driven by robust PMI data.

Will Japan Intervene in Monday’s Thin Asian Markets to Defend 160? Or…?

Yen was at the center stage towards the end of a week of central bank bonanza, with its sharp decline. The Japanese currency is now nearing the crucial 160 level against Dollar, a level last breached in late April and prompted Japanese authorities to intervene to halt its rapid depreciation. The immediate question is whether Japan will seize the opportunity of the typically low-liquidity Asian session on Monday to intervene and prop up Yen. If no intervention occurs, speculators may push Yen further towards 165 mark.

Yen’s recent slide gained momentum a week ago after BoJ refrained from outlining a clear plan for tapering bond purchases, a decision that disappointed the market. While it makes sense for BoJ to wait for new economic projections before making a firm stance, traders were evidently unsatisfied with the lack of immediate action. Additionally, data on Friday showed that demand-led inflation in May slowed, evident with declines in core-core CPI and services price growth, providing no urgent impetus for BoJ to raise rates soon. In contrast, robust PMI data from the US revealed the economy growing at its fastest pace in 26 months, suggesting that any easing of Fed policy will be gradual, even if it begins in September.

Japan seems to be shifting its Yen-supportive tone slightly towards the possibility of monetary tightening. BoJ Governor Kazuo Kuroda has repeatedly indicated that a rate hike in July is a viable option, a sentiment echoed by Deputy Governor Shinichi Uchida.

At the same time, Japan’s top currency diplomat Masato Kanda has softened his rhetoric on intervention, stating that interventions are intended to counter speculative and excessive volatility rather than alter market trends. Kanda emphasized that as long as currency rates move stably in line with fundamentals, there is no need to intervene. This could signal that Japan might be prepared to let Yen depreciate further, possibly to 165 level, if the move is orderly.

But then, the actions or inactions of Japanese authorities in the upcoming Asian session will be crucial in determining Japan’s stance and Yen’s direction. If intervention does not occur, Yen’s depreciation would continue.

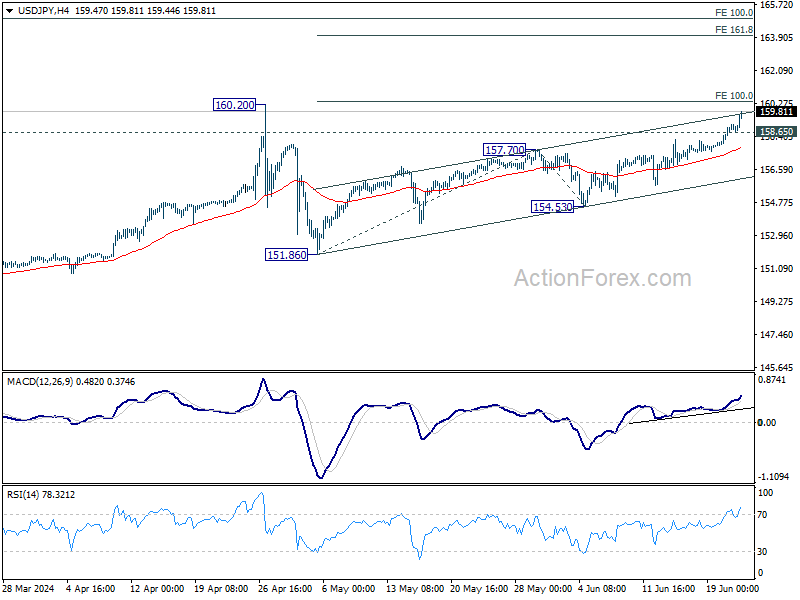

Technically, USD/JPY is also entering a key resistance zone, including near term rising channel, 160.20 top, as well as 100% projection of 151.86 to 157.70 from 154.53 at 160.37. Break of 158.65 minor support will suggest rejection by this resistance zone and bring consolidations first.

However, decisive break of 160 mark and sustained trading above there, could prompt upside accelerations to next near term target at 161.8% projection at 163.97. This would be close to medium term target of 100% projection of 127.20 to 151.89 from 140.25 at 164.94.

Swiss Franc Slips After SNB Rate Cut, Remains Strong Amid French Political Instability

Swiss Franc ended the week as the second weakest currency, impacted by SNB’s rate cut which was a surprise to some market participants. The policy rate was lowered by 25bps 1.25%, marking the second consecutive reduction this year. Alongside the rate cut, SNB adjusted its inflation forecasts downward, predicting a decline from 1.3% this year to 1% by 2026.

While SNB Chair Thomas Jordan offered no definitive clues about future rate cuts, he firmly kept the possibility open. Speaking to Swiss broadcaster SRF, Jordan noted that inflation was falling slightly, which is why SNB has not committed to this being the final rate cut in the cycle.

Economists are divided on whether more rate cuts are forthcoming. Some argued that SNB might align its policy with ECB’s easing cycle to keep Franc stable against Euro, thus avoid significant disinflation. Nevertheless, swap markets are currently only seeing 0.10% of further SNB rate cuts.

Despite its recent pullback, it should be emphasized that Swiss Franc remains the strongest major currency for the month, showing around 2.4% gain against both Yen and Euro.

This strength in Franc is largely due to the political turbulence in France ahead of the snap elections scheduled from June 30 to July 7. Recent polls indicate that Marine Le Pen’s far-right National Rally is leading, followed by the left-wing Popular Front and President Emmanuel Macron’s centrist party. This political uncertainty has already negatively impacted French and Eurozone PMIs.

A victory for the far-right in France could have profound implications for the European Union’s shared identity. Also, as the only EU country with a permanent seat on the UN Security Council, an anti-EU French government could undermine EU’s global influence at a time of increasing geopolitical tensions and protectionism. Moreover, such an outcome could jeopardize Western support for Ukraine in its conflict with Russia.

Technically, a short term bottom could be formed at 0.9476 in EUR/CHF, after hitting 61.8% retracement of 0.9252 to 0.9928 at 0.9510. Some consolidations would be seen first, and last until the results of French elections. But near term outlook will stay bearish as long as 0.9683 resistance holds. Break of 0.9476 and sustained trading below 0.9510 will pave the way back to retest 0.9252 low.

RBA Boosts Aussie While Sterling Slips Post-BoE Announcement

Last week also saw two major central banks, RBA and BoE, hold their interest rates steady at 4.35% and 5.25%, respectively.

RBA maintained a hawkish tone despite the hold. Governor Michele Bullock emphasized that persistent inflation led the board to consider a rate hike, while a rate cut was not even on the table. Consequently, money markets slightly increased the probability of a rate hike in August to 20%. But after all, the deciding factor for RBA’s next move still lies in Q2 inflation report due in July.

Conversely, BoE’s commentary brought the possibility of an August rate cut back into focus, with money markets now seeing 50% chance of a reduction. Before BoE’s announcement, UK CPI data showed inflation slowing to 2% target of in May finally. While services inflation remained high, some Monetary Policy Committee members noted it did not significantly impact the overall disinflation trend.

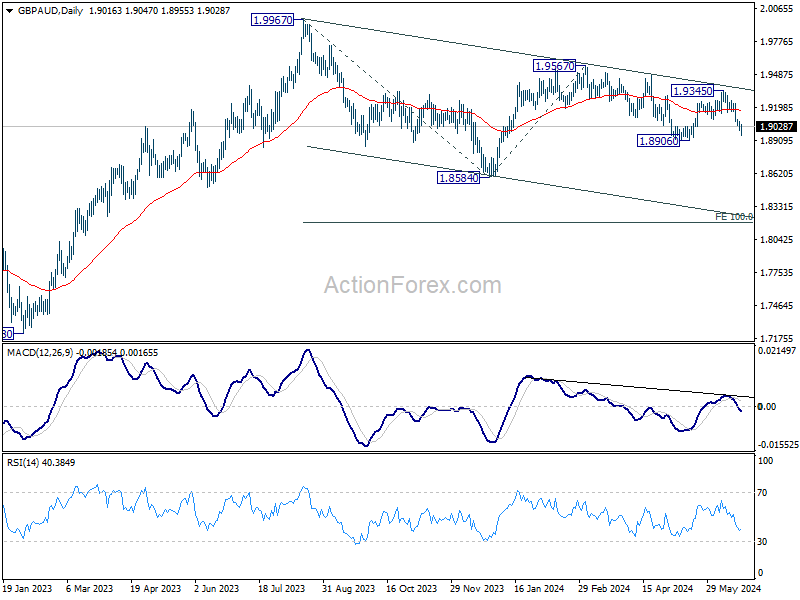

GBP/AUD’s fall from 1.9345 extended lower last week. The development is inline with the view that decline from 1.9567 is in still in progress. Break of 1.8906 support will confirm resumption towards 1.8584 support next. As the fall from 1.9567 is seen as the third leg of the corrective pattern from 1.9967, decisive break of 1.8584 will pave the way to 100% projection of 1.9967 to 1.8584 from 1.9567 at 1.8184 in the medium term.

Dollar Gains on Strong PMI Data, Faces Potential Pullback

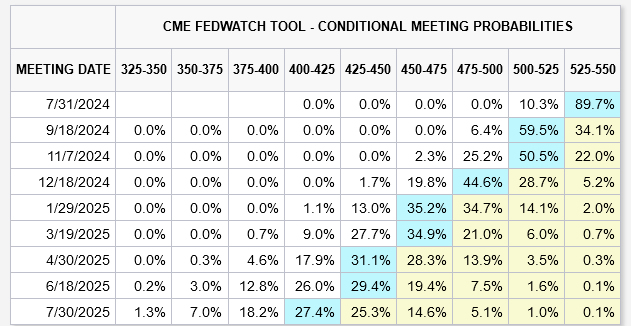

Dollar gained notably on Friday, following solid PMI data indicating strong economic growth and cooling price pressures. However, despite this rally, Dollar was overshadowed by Aussie and Loonie in terms of weekly performance. Currently, Fed fund futures indicate nearly 66% chance of a rate cut by Fed in September, with similar probability for a second cut in December. Nonetheless, as many Fed officials have emphasized, several more months of favorable inflation data are necessary before considering monetary easing.

Dollar Index’s rebound from 103.99 continued last week, albeit just steady momentum. This rally is seen as a leg of the whole rise from 100.61 which should extend through 106.51 resistance to 107.34 and above. However, given that USD/JPY is now close to 160 key resistance while EUR/USD is holding above 1.0667 short term bottom, there is risk of a pull back in Dollar first. Break of 105.12 support in Dollar index will dampen the bullish view and bring more sideway trading first.

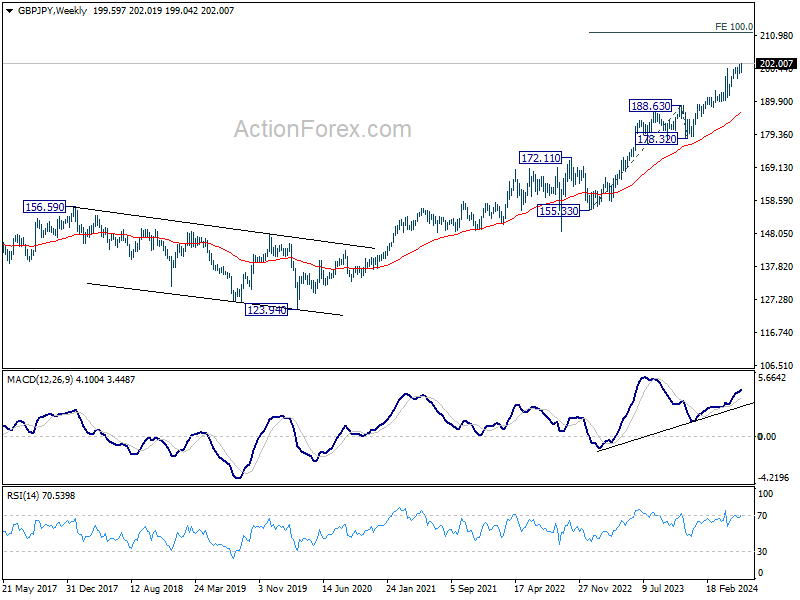

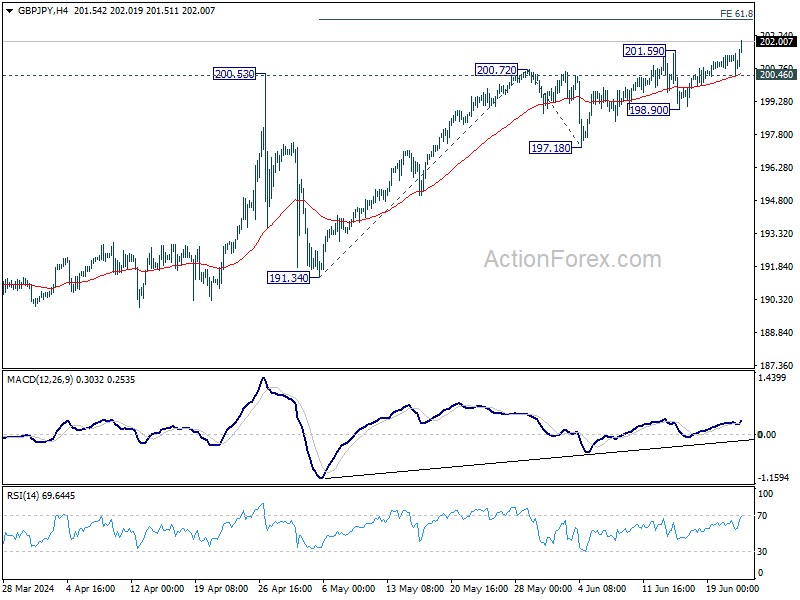

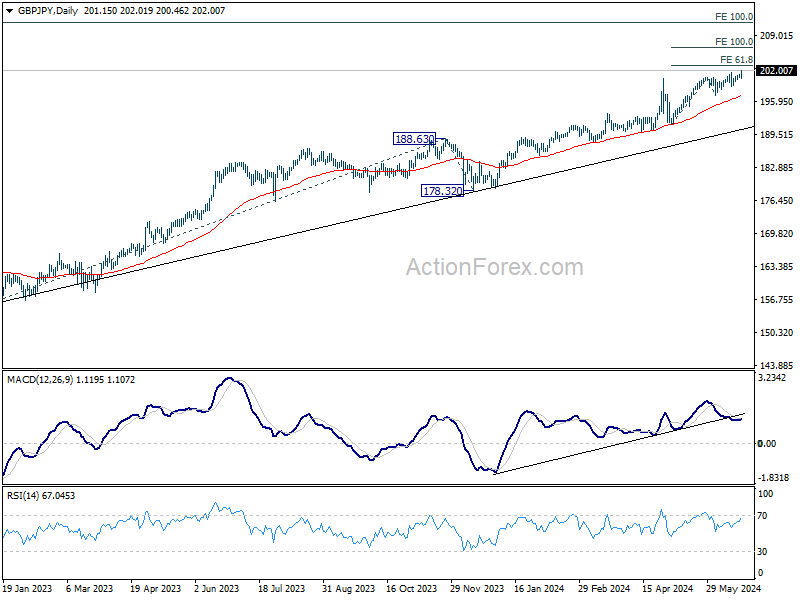

GBP/JPY Weekly Outlook

GBP/JPY’s up trend resumed after brief retreat and hit as high as 202.01. Initial bias is now on the upside this week for 61.8% projection of 191.34 to 200.72 from 197.18 at 202.97. Firm break there will pave the way to 100% projection at 206.56 next. on the downside, below 200.46 minor support will turn intraday bias neutral first. But outlook will remain bullish as long as 198.90 support holds, in case of retreat.

In the bigger picture, long term up trend is still in progress. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62. Outlook will stay bullish as long as 191.34 support holds, even in case of deep pullback.

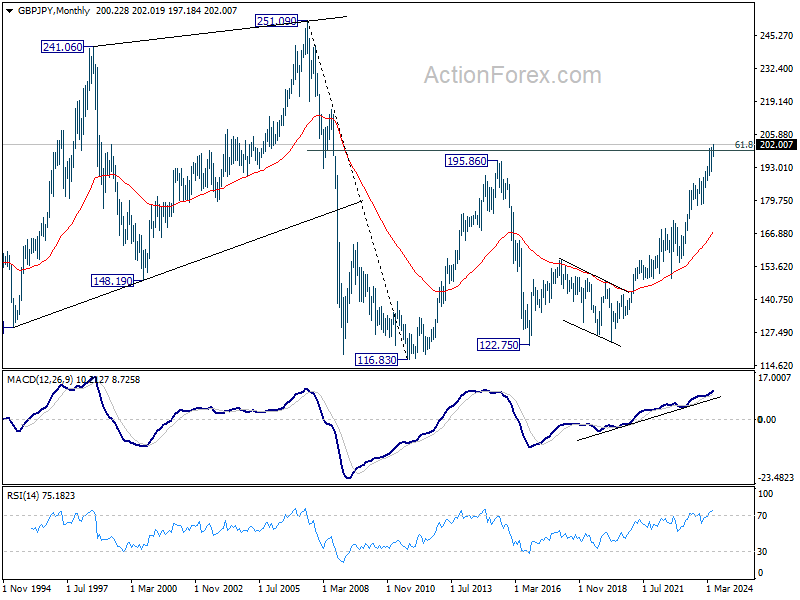

In the longer term picture, rise from 122.75 (2016 low) is seen as the third leg of the pattern from 116.83 (2011 low). Focus is now on 61.8% retracement of 251.09 (2007 high) to 116.83 at 199.80. Decisive break there would pave the way back to 251.09 in the long term.