{kind=link}

Canadian Dollar jumps following after data showing that Canadian inflation unexpectedly accelerated in May. More importantly, the resurgence in price pressures was largely driven by significant increase in services inflation. The data aligns with BoC Governor Tiff Macklem’s cautious stance that the central bank should not ease monetary policy “too quickly.” Given this context, the likelihood of a back-to-back rate cut in July seems minimal. Attention will now shift to whether the Bank of Canada has room to cut interest rates at its September meeting, assuming no drastic economic surprises in the interim.

In broader currency markets, the Euro has turned broadly lower as its near term recovery momentum waned. The common currency remains overshadowed by uncertainties related to the French parliamentary elections, making a sustained bounce unlikely until the political situation clarifies. Australian and New Zealand Dollars, along with Swiss Franc, are among the weakest performers today too. In contrast, Dollar is showing strength, positioning as the second strongest currency after Canadian Dollar. Yen is also seeing some recovery, while British Pound is holding a middle ground.

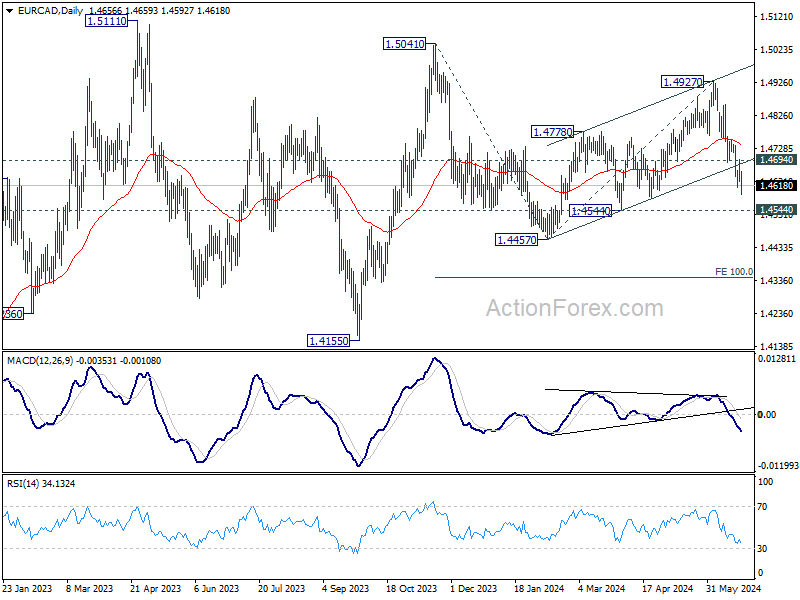

Technically, EUR/CAD’s fall from 1.4927 resumed today after brief recovery. Corrective rise from 1.4457 should have completed with three waves up to 1.4927. Deeper decline is expected as long as 1.4694 resistance holds, to 1.4544 support. Decisive break there will argue that fall from 1.5041 is ready to resume through 1.4457 low.

In Europe, at the time of writing, FTSE is down -0.19%. DAX is down -0.99%. CAC is down -0.82%. UK 10-year yield is down -0.0129 at 4.071. Germany 10-year yield is down -0.017 at 2.405. Earlier in Asia, Nikkei rose 0.95%. Hong Kong HSI rose 0.25%. China Shanghai SSE fell -0.44%. Singapore Strait Times rose 0.37%. Japan 10-year JGB yield rose 0.0092 to 1.000.

Canada’s CPI accelerates to 2.9% yoy, driven by service sector price hikes

Canada’s CPI recorded a notable increase in May, climbing to 2.9% yoy from 2.7% yoy the previous month, surpassing the anticipated rate of 2.6%. This acceleration in headline CPI was primarily fueled by a significant uptick in service prices, which rose by 4.6% yoy in May, following a 4.2% yoy increase in April.

Diving deeper into the components, CPI median—which represents the midpoint of price changes—escalated from 2.6% yoy to 2.8% yoy, again outstripping the forecast of 2.6%. CPI trimmed, another measure that excludes extreme price movements, held steady at 2.9% yoy, also exceeding expectations of 2.8%. In contrast, CPI common, which reflects the common price changes across categories, slowed slightly from 2.6% yoy to 2.4% yoy, falling below the anticipated 2.6%.

On a monthly basis, the CPI rose by 0.6% mom in May, doubling the expected 0.3% mom increase. Similarly, the core CPI also increased by 0.6% mom, well above the forecast of 0.2%. This indicates a broader upward pressure on prices beyond just volatile categories.

Fed’s Bowman: Inflation to remain elevated, rate hold necessary

Fed Governor Michelle Bowman, in a speech today, said her baseline outlook that US inflation will return to the 2% target, provided federal funds rate remains at its current level of 5.25-5.50% “for some time.” She emphasized that Fed is “still not yet at the point” where it would be appropriate to lower the policy rate.

Bowman stressed the need for Fed to “consider a range of possible scenarios” as monetary policy decisions evolve. She remains “willing” to raise interest rates “should progress on inflation stall or even reverse.”

Regarding inflation outlook, Bowman noted that since the beginning of 2024, there has been only “modest” progress on inflation. Core CPI has been running at 3.8% through May, which is significantly above the average inflation rate in the second half of last year. She expects inflation to “remain elevated for some time.”

Bowman also highlighted several upside risks to inflation. She mentioned that it is unlikely that further supply-side improvements will continue to reduce inflation. Geopolitical developments could also pose additional risks. Furthermore, increased immigration and continued labor market tightness could lead to persistently high core services inflation.

Australia’s Westpac consumer sentiment ticks up but still deeply pessimistic

Australia’s Westpac Consumer Sentiment rose 1.7% mom to 83.6 in June. However, the index remains deeply pessimistic, well below neutral level of 100. Although assessments of personal finances and buyer sentiment have become less negative, concerns about inflation, interest rates, and economic growth continue to weigh heavily on consumers.

The sub-index tracking the ‘economic outlook for the next 12 months’ fell -5.7% mom to 78.5, marking its lowest level since last October. In contrast, the ‘economic outlook for the next 5 years’ sub-index saw a slight improvement, rising 2.1% mom to 94.1.

Regarding RBA monetary policy, Westpac noted that the upcoming Q2 CPI data, due on July 31, will be crucial. Westpac expects the update to confirm that weak demand is still exerting disinflationary pressure. This should provide RBA with sufficient confidence that upside risks are not materializing, reducing the likelihood of a rate hike.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0696; (P) 1.0721; (R1) 1.0760; More….

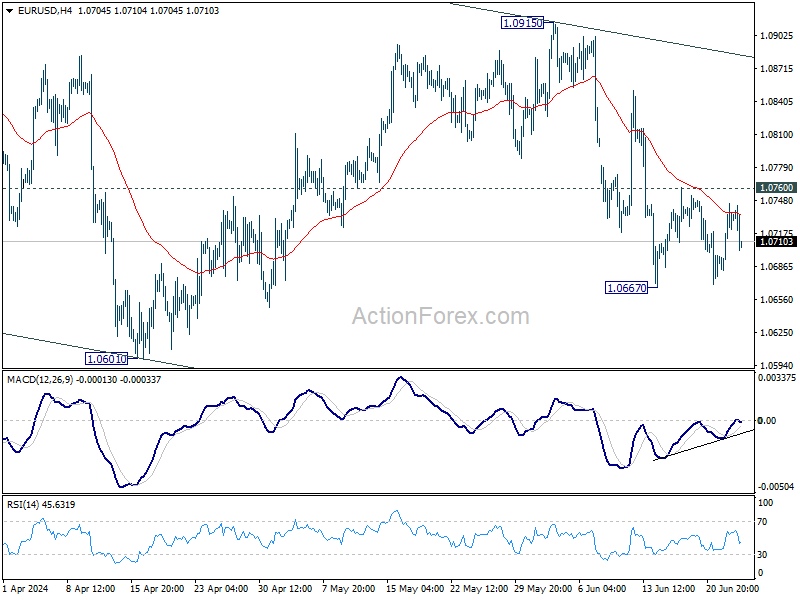

EUR/USD dips notably in early US session but stays in range above 1.0667. Intraday bias remains neutral at this point. Further fall is expected with 1.0760 resistance intact. Decline from 1.0915 is seen as another leg in the larger corrective pattern. Break of 1.0667 will target 1.0601 and below. However, firm break of 1.0760 will turn intraday bias back to the upside for stronger rebound.

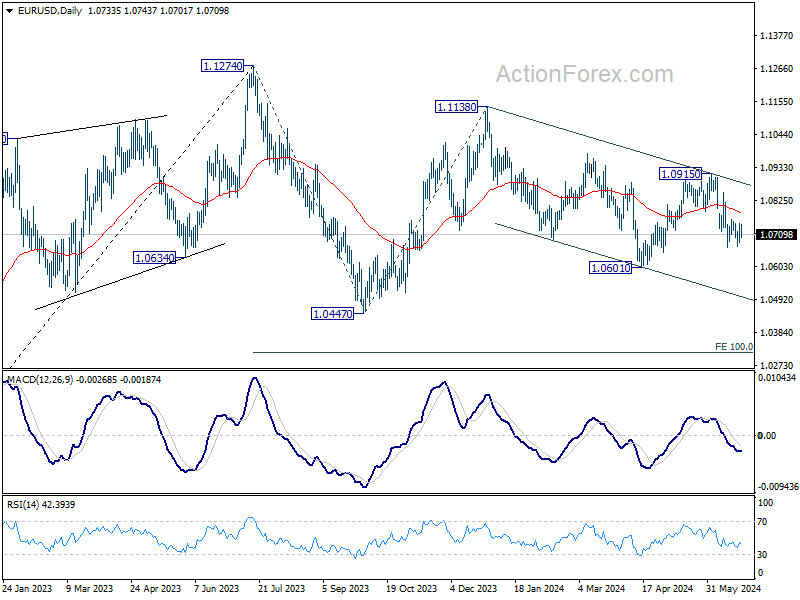

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that’s still in progress. Break of 1.0601 will target 1.0447 support and possibly further to 100% projection of 1.1274 to 1.0447 from 1.1138 at 1.0311. For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y May | 2.50% | 2.80% | 2.70% | |

| 00:30 | AUD | Westpac Consumer Confidence Jun | 1.70% | -0.30% | ||

| 12:30 | CAD | CPI M/M May | 0.60% | 0.30% | 0.50% | |

| 12:30 | CAD | CPI Y/Y May | 2.90% | 2.60% | 2.70% | |

| 12:30 | CAD | CPI Core M/M May | 0.60% | 0.20% | 0.20% | |

| 12:30 | CAD | CPI Median Y/Y May | 2.80% | 2.60% | 2.60% | |

| 12:30 | CAD | CPI Trimmed Y/Y May | 2.90% | 2.80% | 2.90% | |

| 12:30 | CAD | CPI Common Y/Y May | 2.40% | 2.60% | 2.60% | |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Apr | 7.00% | 7.40% | ||

| 13:00 | USD | Housing Price Index M/M Apr | 0.50% | 0.10% | ||

| 14:00 | USD | Consumer Confidence Jun | 100.2 | 102 |