{kind=link}

Yen is under intense scrutiny today as it continues a six-day losing streak, approaching the key psychological level of 160 against Dollar. This move comes despite Japan’s core inflation reaccelerating in May, but failed to meet market expected pace. Additionally, core-core CPI, which excludes both food and energy, and services inflation both continued to decline. These mixed signals undermine the case for BoJ to consider raising interest rates again in July. Furthermore, BoJ has yet to clarify its stance on the tapering of bond purchases, adding to the market’s uncertainty.

As the Yen edges closer to 160 per Dollar, a level often associated with intervention by Japanese authorities, comments from Japanese officials suggest a more hands-off approach. Masato Kanda, Japan’s top currency diplomat, reiterated that the authorities are prepared to counter speculative and highly volatile moves in the currency markets. But more importantly, he emphasized that intervention is “not intended to change the market’s trend.” He added that as long as currency rates move stably in line with economic fundamentals, there is no need for intervention.

Kanda’s comments could be interpreted by some that the authorities might tolerate further Yen depreciation, provided the movement is orderly and reflective of underlying economic conditions. So, Japan’s reaction to USD/JPY at 160 in the next few days would be crucial to decide whether the intervention threshold has already moved up, say to 165 or 170.

In the broader currency markets, Australian Dollar is currently the strongest performer of the week, supported by RBA’s indication that a rate hike remains on the table. Canadian Dollar is the second strongest, followed by Euro. Conversely, New Zealand Dollar is the second weakest, next to Yen. Sterling is the third worst, following BoE’s suggestion that an August rate cut is back on the table. Swiss Franc, despite the pullback after SNB’s rate cut, is positioned in the middle, maintaining most of the gains due to political instability in the EU. Dollar is also trading in the middle of the performance chart.

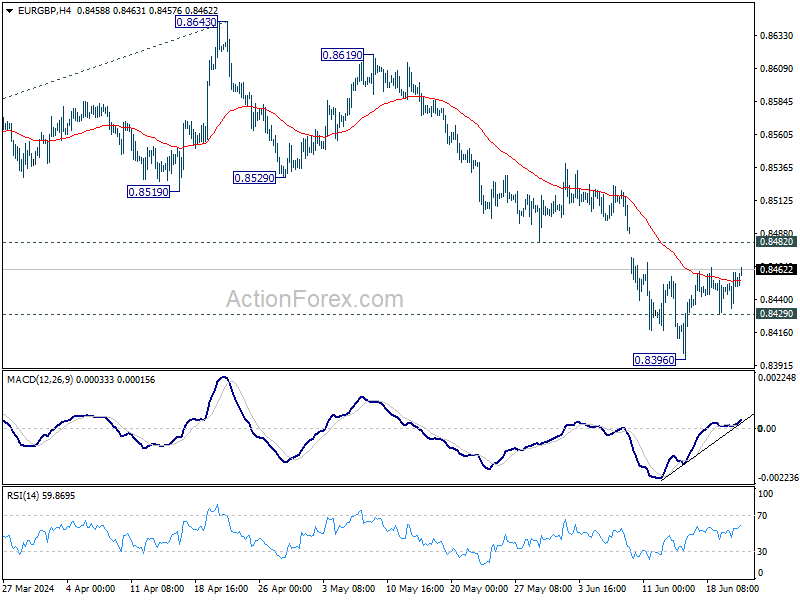

Technically, EUR/GBP is worth some attention today. While recovery from 0.8396 might extend higher, upside could be capped by 0.8482 support turned resistance. Break of 0.8429 minor support will argue that larger down trend is ready to resume through 0.8396. Nevertheless, decisive break of 0.8482 will confirm short term bottoming and bring stronger rebound. Reactions to today’s UK retail sales and PMIs, as well as Eurozone PMIs could decide the next move.

In Asia, at the time of writing, Nikkei is down -0.02%. Hong Kong HSI is down -1.71%. China Shanghai SSE is down -0.36%. Singapore Strait Times is up 0.30%. Japan 10-year JGB yield is up 0.0303 at 0.986. Overnight, DOW rose 0.77%. S&P 500 fell -0.25%. NASDSAQ fell -0.79%. 10-year yield rose 0.037 to 4.254.

Japan’s CPI core accelerates to 2.5%, but core-core slows to 2.1%

Japan’s CPI core (ex-food) accelerated from 2.2% yoy to 2.5% yoy in May, slightly below the expected 2.6%. This marks the 26th consecutive month that core inflation has remained above BoJ’s 2% target. However, the increase was primarily driven by a significant 14.7% yoy rise in electricity prices.

In contrast, CPI core-core (ex-food and energy) slowed from 2.4% yoy to 2.1% yoy. Additionally, services inflation eased from 2.5% yoy to 2.2% yoy. Headline CPI also rose from 2.5% to 2.8% yoy, marking its ninth consecutive month of deceleration and the lowest reading since September 2022.

BoJ Governor Kazuo Ueda has repeatedly suggested that a July rate hike is a possibility. However, today’s report indicates that the inflation uptick is mainly due to cost-push factors, such as higher electricity prices, rather than increased demand. This might not provide a strong enough basis yet for BoJ to proceed with a rate hike at this time.

Japan’s PMI composite falls to 50, mixed economic signals with rising costs

Japan’s latest PMI data for June presents a mixed economic outlook. Manufacturing PMI slipped slightly from 50.4 to 50.1, falling short of expectations of 50.6. However, manufacturing output showed a positive shift, rising from 49.9 to 50.5, marking the first expansion in over a year. Conversely, Services PMI dropped sharply from 53.8 to 49.8, indicating fractional contraction for the first time since August 2022. As a result, Composite PMI fell from 52.6 to 50.0.

Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, commented that the private sector expansion has stalled midway through the year. The return of manufacturing output growth was overshadowed by a decline in services activity, partially due to labor constraints.

A notable concern is the “pressure on margins,” with average input costs rising at the fastest pace in over a year while output price inflation softened, particularly in the service sector. Anecdotal evidence pointed to the weak yen and increasing labor costs as significant factors driving up cost inflation.

Australia’s PMI composite falls to 50.6, slowing business expansion, manufacturing weakness

Australia’s PMI data for June indicates a slowdown in business expansion, with Manufacturing PMI falling from 49.7 to 47.5, Services PMI dropping from 52.5 to 51.0, and Composite PMI decreasing from 52.1 to 50.6, hitting a five-month low.

Warren Hogan, Chief Economic Advisor at Judo Bank, noted that while business activity continues to grow, the pace of expansion has slowed compared to the strong performance in the first half of 2024.

The manufacturing sector showed significant weakness, with PMI, output, and new orders declining towards the cyclical lows of 2023, all falling below the 50 threshold that separates expansion from contraction. In contrast, the services sector experienced a slight pullback but remained in expansionary territory.

The composite input price index dropped below 60 for the first time since January 2021, suggesting that business cost growth is easing. Final prices also decreased but still indicate above-target inflation. Service sector price indicators retreated in June, aligning with the view that inflation is gradually easing in 2024, yet they remain above RBA’s target range of 2-3%.

Looking ahead

UK will release retail sales and PMIs in European session. Eurozone PMIs will also be featured. Later in the day, Canada will publish retail sales, and IPPI and RMPI. US will release PMIs and existing home sales.

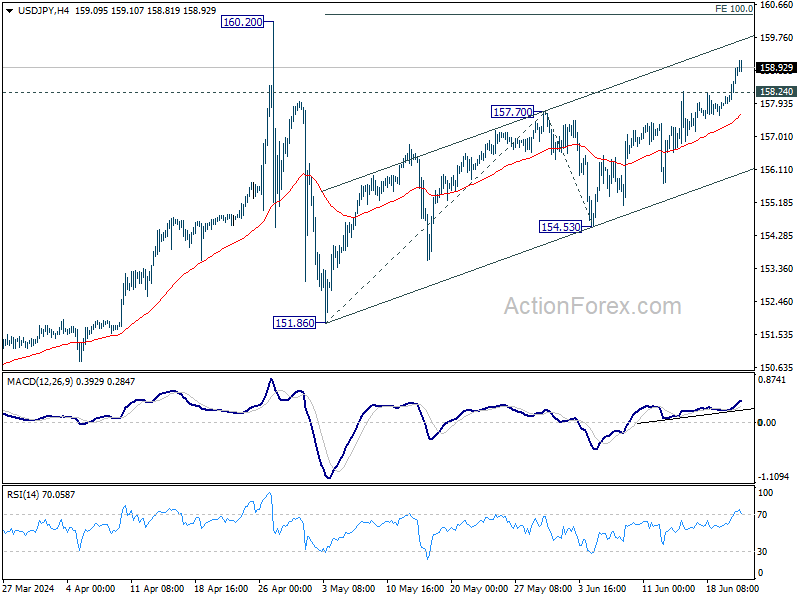

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.25; (P) 158.59; (R1) 159.28; More…

USD/JPY’s rise from 151.85 is still in progress and intraday bias stays on the upside. Further rally could be seen to 160.20 high, or possibly to 100% projection of 151.86 to 157.70 from 154.53 at 160.37. But upside should be limited there, at least on first attempt. On the downside, below 158.24 minor support will turn intraday bias neutral first.

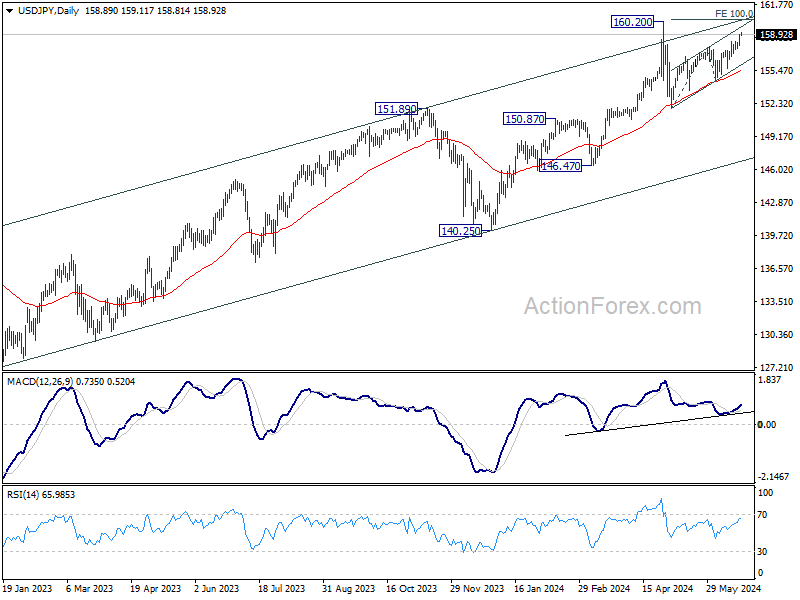

In the bigger picture, price actions from 160.20 medium term top are seen as a corrective pattern to rise from 150.25 only. Another rally is still expected at a later stage through 160.02 to resume the larger up trend. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Jun P | 47.5 | 49.7 | ||

| 23:00 | AUD | Services PMI Jun P | 51 | 52.5 | ||

| 23:01 | GBP | GfK Consumer Confidence Jun | -14 | -16 | -17 | |

| 23:30 | JPY | National CPI Y/Y May | 2.80% | 2.50% | ||

| 23:30 | JPY | National CPI ex Fresh Food Y/Y May | 2.50% | 2.60% | 2.20% | |

| 23:30 | JPY | National CPI ex Food Energy Y/Y May | 2.10% | 2.40% | ||

| 00:30 | JPY | Manufacturing PMI Jun P | 50.1 | 50.6 | 50.4 | |

| 00:30 | JPY | Services PMI Jun P | 49.8 | 53.8 | ||

| 06:00 | GBP | Retail Sales M/M May | 1.50% | -2.30% | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) May | 14.8B | 19.6B | ||

| 07:15 | EUR | France Manufacturing PMI Jun P | 46.8 | 46.4 | ||

| 07:15 | EUR | France Services PMI Jun P | 50 | 49.3 | ||

| 07:30 | EUR | Germany Manufacturing PMI Jun P | 46.4 | 45.4 | ||

| 07:30 | EUR | Germany Services PMI Jun P | 54.4 | 54.2 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jun P | 48 | 47.3 | ||

| 08:00 | EUR | Eurozone Services PMI Jun P | 53.5 | 53.2 | ||

| 08:30 | GBP | Manufacturing PMI Jun P | 51 | 51.2 | ||

| 08:30 | GBP | Services PMI Jun P | 53.2 | 52.9 | ||

| 12:30 | CAD | Industrial Product Price M/M May | 0.40% | 1.50% | ||

| 12:30 | CAD | Raw Material Price Index May | -0.60% | 5.50% | ||

| 12:30 | CAD | Retail Sales M/M Apr | 0.90% | -0.20% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Apr | 0.50% | -0.60% | ||

| 13:45 | USD | Manufacturing PMI Jun P | 51 | 51.3 | ||

| 13:45 | USD | Services PMI Jun P | 53.5 | 54.8 | ||

| 14:00 | USD | Existing Home Sales May | 4.10M | 4.14M | ||

| 14:30 | USD | Natural Gas Storage | 69B | 74B |