{kind=link}

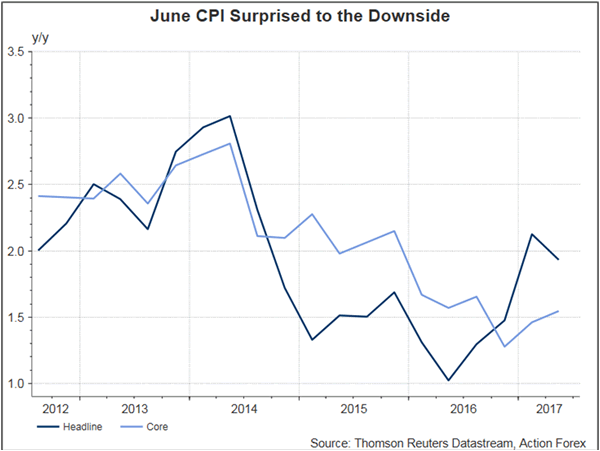

Aussie dropped after the weaker than expected inflation report, as traders took profit after the currency rallied to 2-year against USD and last week. Headline CPI moderated to +1.9% y/y in 2Q17 from +2.1% a quarter ago. The market had anticipated an increase to +2.2%. Key contributors to the weakness were lower automotive fuel prices as global oil prices plunged and the usual seasonal drop in domestic holiday, travel and accommodation prices. RBA’s trimmed mean slipped 0.1 percentage point to +1.8%, in line with expectation, while the weighted median CPI climbed +0.1 percentage point to +1.8% in the second quarter. Consumer price levels are an important gauge of central banks’ monetary outlook. The dilemma currently facing major central banks worldwide is the continuing economic growth and employment market improvement, alongside subdued inflation. At the July meeting minutes, RBA acknowledged that weak inflation is a global phenomenon with core inflation remaining low while headline inflation turning down..

RBA’s Neutral Rate Rhetoric Overstated

Indeed, Aussie’s rally last week was a result of market’s overreaction to ‘neutral rate’ rhetoric’s by the RBA and Fed Chair Janet Yellen. Recall that RBA suggested that the neutral nominal cash rate is around 3.5%, with medium-term inflation expectations well- anchored around 2.5%’. It also noted that ‘a reduction in risk aversion and/or an increase in the potential growth rate could see the neutral real interest rate rise again’. Fed’s Yellen noted at the testimony that ‘the neutral rate is currently quite low by historical standards, the federal funds rate would not have to rise all that much further to get to a neutral policy stance’.

Despite initial impression that RBA’s language was implying a tightening stance, RBA’s estimated nominal neutral rate, currently at 3.5%, was weaker than the previous projection of 5% (prior to global financial crisis). More importantly, what RBA noted was ‘nominal neutral rate’ which, if adjusted with medium term inflation expectations of around 2.5%, would bring a real rate of 1%. This is indeed coincident with the Fed’s long-run neutral rate in real terms. Meanwhile, Yellen’s comments on neutral rate were not more pessimistic than previously. Indeed, the Fed’s neutral rate stance over recent years has remained similar, suggesting that the neutral rate had fallen fell sharply after the financial crisis and has remained near zero; r-star would move high should the temporary factors dissipate over time and the long-term level of the neutral rate has permanently shifted downward due primarily to slower potential growth.

RBNZ Assistant Governor John McDermott also talked about the monetary policy outlook earlier today. His stance, while driven muted market reaction, was rather dovish. He suggested that current estimate of the neutral interest rate is around 3.5 % with potential output growth at 2.9% and core inflation at 1.4%. He added that the neutral rate has been slowly falling for some time, due to lower potential output growth. Dating back to early 2015, the central bank noted that the neutral interest rate is around 4.5%